Transaction Attributes and Customer Valuation

Michael Braun

Cox School of Business

Southern Methodist University

David A. Schweidel

Goizueta Business School

Emory University

dschweidel@emory.edu

Eli Stein

Harvard College

Harvard University

estein@post.harvard.edu

Forthcoming in December 2015 issue of Journal of Marketing Research

Abstract

Dynamic customer targeting is a common task for marketers actively managing customer

relationships. Such efforts can be guided by insight into the return on investment from marketing

interventions, which can be derived as the increase in the present value of a customer’s expected

future transactions. Using the popular latent attrition framework, one could estimate this value

by manipulating the levels of a set of nonstationary covariates. We propose such a model that

incorporates transaction-specific attributes and maintains standard assumptions of unobserved

heterogeneity. We demonstrate how firms can approximate an upper bound on the appropriate

amount to invest in retaining a customer and demonstrate that this amount depends on customers’

past purchase activity, namely the recency and frequency of past customer purchases. Using

data from a B2B ser vice provider as our empirical application, we apply our model to estimate

the revenue lost by the service provider when it fails to deliver a customer’s requested level of

service. We also show that the lost revenue is larger than the corresponding expected gain from

exceeding a customer’s requested level of service. We discuss the implications of our findings

for marketers in terms of managing customer relationships.

Keywords:

services marketing, customer retention, probability models, marketing ROI, customer

value

1

According to IBM’s recent survey of chief marketing officers, 63% of respondents said that

return on investment (ROI) would be the most important measure of success in the next three to five

years (IBM Corporation 2011). Braun and Schweidel (2011) argue that marketing ROI should be

measured in terms of an expected change in the residual value of the customer base that occurs from a

marketing intervention. Latent attrition models, such as the the Pareto/NBD (Schmittlein, Morrison,

and Colombo 1987) and the BG/NBD (Fader, Hardie, and Lee 2005a), are useful for estimating

residual value, but they do not lend themselves easily to incorporating covariates that change from

transaction to transaction. In the marketing ROI domain, possible examples of these covariates

include attributes of the marketing mix, exogenous conditions at the time of the transaction (e.g.,

weather effects), or an investment in improved customer experiences.

The quality of customer information to which a firm has access, which encompasses being

both broad and up-to-date, has been found to moderate the profitability of customer prioritization

(Homburg, Droll, and Totzek 2008). Similarly, Mithas, Krishnan, and Fornell (2005) posit that the

value of customer relationship management tools lies in their ability to facilitate learning about

customers over the course of multiple interactions, the insights from which can then be used to target

customers dynamically with tailored offerings. Though some researchers have proposed methods of

incorporating both time-invariant and time-variant predictors into customer base analyses (Abe 2009;

Schweidel and Knox 2013), these models stop short of establishing the link between the effects

of transaction-specific attributes and forecasts of residual value. Thus, how to use information

about transaction attributes to assess the increased customer value stemming from marketing efforts

remains an open and important area of research.

In this paper, we propose a latent attrition model that integrates transaction attributes into a

probability model of customer retention and lifetime value. One application of this model (and the

one we use in our empirical analysis) is to evaluate the impact of a customer’s service experience on

customer retention. Consider the following scenario. A local business (i.e., the customer) contracts

with a service provider to meet a recurring business need, such as copywriting services. Based on

examples of the provider’s work, the customer has some expectation of the caliber and timeliness of

2

the work. If the provider delivers a top-notch experience, the customer may engage the provider

the next time he needs similar services. By increasing the retention probability for that customer,

all else being equal, the service experience delivered by the provider’s team may have generated

additional revenue in subsequent time periods. In contrast, if the provider falls short and delivers

a sub-par experience, the customer may be more likely to search for another provider when the

need for similar services arises in the future. When this happens, the future revenue stream from

the customer falls to zero. In this example, the attributes of a single customer-firm interaction

could affect the future revenue stream. The “transaction attribute” in this case is an indicator of the

customer’s service experience. More generally, transaction attributes may refer to some aspect of

the marketing mix, the employee who processed a customer’s transaction, or any information about

a customer’s transaction that the firm has collected.

While there is an intuitive relationship between transaction attributes and retention probabilities,

and hence customer value, extant empir ical research often fails to differentiate among transactions

other than with regard to the times at which the events occur. Models like the Pareto/NBD and

the BG/NBD rely on summary statistics of past transactional activity, namely the total number

of transactions (frequency) and the time of the most recent transaction (recency). However, by

aggregating the data to this level, information about other characteristics of each transaction is

lost. Take the case of two customers with the same number of transactions dur ing the last year,

and with their most recent transaction occurring on the same day. Ignoring attr ibutes of those

transactions, these two customers’ transaction histories, and the resulting predictions of residual

value, are identical. If a firm had access to additional information about the last customer-firm touch

point, the firm could have different beliefs of what each customer would do in the future. Failing to

meet stated and established standards of service, for example, may lead the firm to believe that a

customer is now at a g reater risk for churn, while exceeding these standards may lead to perceptions

that this risk is lower (Ho, Park, and Zhou 2006).

Exploiting information about the attributes of each transaction gives firms additional guidance for

managing customer relationships, compared to the information provided by frequency and recency

3

alone. The value of transaction attribute data comes from how that information affects the firm’s

decisions. We assess the effect of a particular transaction attribute in terms of the projected change

in discounted expected residual transactions (DERT, Fader, Hardie, and Lee 2005b; Fader, Hardie,

and Shang 2010). DERT is the present value of expected future transactions, taking into account

the probability that a customer may have already chur ned, or will churn in the future. Differences

in the transaction attributes will produce variation in DERT beyond that which is captured by

the recency and frequency of transactions. Attribute data can affect firm decisions in two ways.

First, ignoring attributes can lead to different estimates of DERT, which in turn may lead to a

suboptimal decisions based on bad information. Second, the “incremental DERT” that comes from

manipulating the transaction attributes (say, by increasing investment in retaining a specific customer

immediately before a transaction) can serve as an upper limit for such a marketing investment (Braun

and Schweidel 2011). For example, if a firm could estimate the effect of a marketing mix variable

on churn, the incremental DERT would be the difference between the forecast of DERT under the

marketing treatment, and a baseline DERT without it. To the best of our knowledge, our research is

the first to examine the value of information about transaction attributes in terms of the change in

expected future customer transactions.

In the next section, we provide a brief discussion of relevant literature in the customer base

analysis and service quality areas, the latter of which relates to the context of our empirical example.

We show how our research adds to the associated body of knowledge. Then, we describe the

model, in terms of a likelihood function, as well as derive both prior and posterior DERT that can

be expressed in either closed-form or as a summation. The subsequent empirical analysis, which

employs a dataset from a noncontractual service provider, illustrates a case in which including

transaction attribute data adds predictive power to the model. Finally, we show that incremental

DERT has a nonlinear and non-monotonic relationship with customer recency and frequency. The

patterns suggest that falling short of the requested service level has a smaller effect on retaining

customers who are either likely to have already chur ned, or who are highly unlikely to have churned,

compared to the effect on customers for whom there is more uncertainty in their active status.

4

1 Related Literature

Latent attrition models such as the Pareto/NBD and the BG/NBD are workhorse models of customer

base analysis (Schmittlein, Morrison, and Colombo 1987; Fader, Hardie, and Lee 2005a; Fader,

Hardie, and Lee 2005b). A notable limitation of this class of models is the difficulty of incorporating

information about attributes that accompany each customer-fir m interaction, such as marketing

actions that vary across transactions. Recognizing this gap in the literature, Ho, Park, and Zhou

(2006) propose incorporating customer satisfaction into the latent attrition framework. Their model

assumes that customer satisfaction affects the rate at which customers conduct transactions, and they

demonstrate how satisfaction can be allowed to impact the attrition process. Although Ho, Park, and

Zhou do consider information that is specific to the customer-firm interaction (i.e., satisfaction),

their model is analytic, as opposed to empirical. Nevertheless, they illustrate the importance of

incorporating customer satisfaction and, more broadly, customer-firm interaction information, into

estimates of customer value.

Another notable difference between the Ho, Park, and Zhou (2006) model and empirical latent

attrition models is that Ho, Park, and Zhou assume homogeneous purchase and attrition processes.

In addition to capturing variation across customers, models that allow for unobserved heterogeneity

let firms update their expectations of customer behavior as new data become available. These

posterior inferences are necessary both for valuing customers (Fader, Hardie, and Lee 2005a; Braun

and Schweidel 2011) and for assessing the impact of marketing efforts. Schweidel and Knox (2013)

illustrate this idea with a joint model of individuals’ donation activity and the direct marketing efforts

of a non-profit organization, accounting for the potentially non-random nature of marketing efforts.

In their example, the authors allow for direct marketing activity to affect the likelihood of donation

each month, the amount of a donation conditional on the donation occurring, and the likelihood

with which a donor becomes inactive. To account for unobserved heterogeneity, Schweidel and

Knox apply a latent class structure. While their model allows for marketing actions to impact

each of the processes that may affect customer value, they do not consider how an individual’s

transaction history may affect expectations of future activity. Moreover, they do not consider how

5

their framework could be adapted to estimate measures such as expectations of future purchases,

customer lifetime value, or residual value.

Like Schweidel and Knox (2013), Knox and van Oest (2014) also employ a latent class structure

to account for heterogeneity across customers in their investigation of the impact of customer

complaints on customer churn. They assess the impact of customer complaints and recovery by

the firm for two types of customers: a new customer and an established customer. The authors

demonstrate that the residual value of customers following a complaint varies with both the customers’

past purchase activity and past complaints. The authors distinguish between the effects of marketing

interventions on new and established customers, consistent with research that has investigated the

profitability of behavior-based marketing actions (Villas-Boas 1999; Pazgal and Soberman 2008;

Shin and Sudhir 2010). While extant work has documented the benefits of differentiating between

new and established customers, such work often does not seek to provide insight into how marketing

interventions may affect established customers with different transaction histor ies. We contribute to

this stream of research by developing a modeling framework that allows us to conduct a systematic

investigation into how customers’ recency and frequency of past transactions (Fader, Hardie, and

Lee 2005b) affects the incremental impact of marketing efforts, which can enable marketers to target

customers with increased precision.

Although there are many different attributes a transaction could possess, our empirical analysis

in Section 3 is in the domain of service quality. Several researchers have studied service quality and

its relationship to customer expectations. Boulding et al. (1993) find that a customer’s evaluation of

a service encounter is affected by his prior expectations of what will and should occur, as well as the

quality of service delivered on recent service encounters. In essence, will and should expectations

for a service encounter are a weighted average of prior expectations and the recently experienced

service. Boulding, Kalra, and Staelin (1999) further investigate the process by which expectations

are updated. In addition to affecting a customer’s cumulative opinion, the authors find that prior

beliefs also affect how experiences are viewed. As a result, prior expectations deliver a “double

whammy” to evaluations of quality. This suggests that service encounters are not all equal in

6

the eyes of consumers, as the way in which service encounters are viewed are affected by past

experiences. For example, the exact same level of quality might exceed expectations in a mid-range

family restaurant, but miss expectations in a fancy bistro. Yet, extant customer valuation models in

both non-contractual and contractual settings often assume that the “touch points” associated with

customer-firm interactions are equivalent to each other.

Rust et al. (1999) further investigate the role of customer expectations in perceptions of quality.

Rather than focusing on the average expectation across customers, the authors highlight the

importance of the distribution of customer expectations. They tackle a number of myths that had

been held with regard to the level of service that providers should deliver to their customers. In

contrast to the popularly held belief that firms must exceed expectations, the authors find evidence

that simply meeting customers’ expectations can result in a positive shift in preferences. They

also find that service encounters that are slightly below expectations may not affect customers’

preferences at all. Though provoking, the authors recognize that because they conducted their

investigation in a laboratory setting, and relied on self reports, there is a need for additional research.

In addition to the work that has been conducted on service quality, our research is also related

to work on customer satisfaction. Bolton (1998) investigates the impact of customer satisfaction

on the duration for which customers continue to subscribe to a contractual service. She finds that

reported customer satisfaction with the service, solicited prior to the decision of whether to remain

a subscriber or cancel service, is positively related to the duration for which a customer will retain

service. She also finds evidence that recent experiences with the service provider are weighed

differently depending on whether the experience was evaluated as positive or negative. To the best

of our knowledge, research on customer valuation has not incorporated this differential weighting of

customer experiences into estimates of customers’ future behavior.

7

2 Model

In this section we propose a general form of a latent attr ition model that incorporates transaction

attributes. To keep terminology consistent with the empirical example in Section 3, we say that the

customer of the firm places orders for jobs, and the firm fills those orders by completing the jobs.

Thus, orders and jobs always occur in a pair, and are indexed by

k

. We assume that these jobs are

completed the instant the order is placed, so we index calendar time for orders and jobs by

t

. Without

loss of generality, we define a unit of calendar time as one week. The service was introduced to the

marketplace at time

t =

0 and

T

is the week of the end of the observation period. Let

t

1

be the week

of the customer’s first order, let

x

be the number of orders between times

t

1

and

T

, including that

first order at

t

1

, and let

t

k

be the time of order

k

. Therefore,

t

x

is order time of the final, observed

job. For clarity, we are suppressing the customer-specific indices on

t

and

x

in the model exposition.

Our baseline model is a variant of the BG/NBD model for non-contractual customer base analysis

(Fader, Hardie, and Lee 2005a). Immediately before the customer places an initial order at time

t

1

,

he is in an active state. While active, the customer places orders according to a Poisson process with

rate

. After each job (including the first one), a customer may churn, resulting in that order being

his last. With probability

p

k

, the customer churns after the

k

th

job and transitions from the active

state to the inactive state. Upon doing so, we assume that the customer is lost for good and will

not place any more orders, ever. If the customer does not churn, then the time until the next order,

t

k+1

t

k

, is a realization of an exponential random variable with rate

. We never observe directly

when, or if, a customer churns, although if a customer places

x

orders, he must have survived

x

1

possible churn opportunities.

For a customer who places

x

orders between times

t

1

and

T

, the joint density of the

x

1

inter-order times is the product of

x

1 exponential densities. For this customer, there could not

have been any orders between times

t

x

and

T

. This “hiatus” could occur in one of two ways. One

possibility is that the customer may have churned after job

x

, with probability

p

x

. Alternatively,

the customer may have “survived” with probability 1

p

x

, but the time of the next order would be

sometime after

T

. Thus, conditional on surviving

x

jobs, the probability of not observing any more

8

jobs before time T is e

(Tt

x

)

. Hence, the conditional data likelihood for a single customer is

f (x, t

2:x

|, p

1:x

) =

x1

e

(t

x

t

1

)

2

6

6

6

6

4

x1

Y

k=1

1 p

k

3

7

7

7

7

5

f

p

x

+

1 p

x

e

(Tt

x

)

g

(1)

If

p

k

were time-invariant (i.e., the same for all

k

), Equation 1 would be the individual-level likelihood

in the BG/NBD

1

. To incorporate transaction-specific information, we allow

p

k

to vary across orders

in our model. We define the probability of becoming inactive by transitioning to the inactive state

immediately after job

k

as

p

k

=

1

e

✓q

k

and define

B

k

=

P

k

j=1

q

k

, where

q

k

is a non-negative

scalar value that can influence the probability that a customer transitions to the inactive state after

job

k

. If we restrict

q

k

=

1 for all

k

, then

p =

1

e

✓

, or alternatively,

✓ = log(

1

p)

. The

expression

q

k

, and hence

B

k

, could be a function of further parameters and observed data, such as

the transaction attributes. For example, we might give

q

k

a log-linear str ucture, where

log q

k

=

0

z

k

,

is a vector of homogeneous coefficients, and

z

k

is a vector of covariates that represents attributes

of transaction k. Substituting these definitions into Equation 1,

f (x, t

2:x

|, ✓, q

1:x

) =

x1

e

(t

x

t

1

)✓ B

x1

f

1 e

✓q

x

⇣

1 e

(Tt

x

)

⌘g

(2)

The expression of the likelihood in Equation 2 assumes that all customers place orders at the same

rate, and that all customers have the same baseline propensity to churn after each job. To incorporate

heterogeneity of latent characteristics into the model, we let

and

✓

vary across the population

according to gamma distributions, where

⇠ G

(r, a)

and

✓ ⇠ G

✓

(s, b)

. Integrating over these

latent parameters, we get the marginal likelihood:

L =

(r + x 1)

(r)

a

r

(a + t

x

t

1

)

r+x1

b

b + B

x1

!

s

2

6

6

6

6

4

1

b + B

x1

b + B

x

!

s

*

,

1

a + t

x

t

1

a + T t

1

!

r+x1

+

-

3

7

7

7

7

5

(3)

A detailed derivation of the marginal likelihood is in Equation 10 in Appendix A. Transforming

1As with the BG/NBD, in our model a high transaction rate suggests additional attrition opportunities.

9

a gamma-distributed random variable to yield a value between zero and one was discussed by

Grassia (1977). If

p

k

were constant across time, and varied across the population according to a

beta distribution, then the marginal likelihood would be the same as the BG/NBD. Griffiths and

Schafer (1981) show that Grassia’s method and a beta distribution are “practically identical,” and

that choice between them could be based “entirely on mathematical convenience.” Our approach

lets us estimate model parameters using standard maximum likelihood techniques even when the

attrition probability depends on transaction-specific covariates.

Certain design decisions allow us to maintain some degree of computational efficiency. We allow

for unobserved heterogeneity in

and

✓

by carefully choosing a parametric family of independent

mixing distributions. The

B

x

term is heterogeneous across observable characteristics that vary

across both individuals and time. Also, we allow for unobserved nonstationarity in some of the

parameters in B

x

(see Equations 8 and 9).2

2.1 Conditional expectations and DERT

Once a manager has parameter estimates in hand, he might be interested in the number of orders

that we might receive from a newly acquired customer during a period of

t

weeks. In Appendix A

we show that the prior expected value of this order count is

E[X (t)] =

1

X

k=1

b

b + B

k

!

s

H

B

✓

t

a + t

; k, r

◆

(4)

Therefore, the manager can estimate the expected number of orders by truncating this infinite series.

The function

H

B(x

;

a, b)

is regularized beta function, which also happens to be the cdf of a beta

distribution, with parameters a and b, evaluated at x.3.

One way to interpret the summation in Equation 4 is as the sum of the probabilities of ordering

2

Among the alternative specifications considered was one in which we allow for heterogeneity in

via a latent

class structure. The estimated probability of being in the first latent class was

p =

1, suggesting that the additional

model complexity is not warranted. We also estimated a model that allows

to vary with

z

k

. The Hessian in the

resulting model was singular, so the parameters could not be identified when covariates are assumed to impact both the

transaction rate and the attrition process simultaneously.

3A glossary of many of the functions we use in this paper is in Table 3 in Appendix A

10

k

jobs before time

t

, for all possible values of

k

. These jobs are hypothetical, so we need a model

for each

q

k

that comprises

B

k

, which is the cumulative sum of

q

1

, q

2

,...,q

k

. In general, one could

simulate multiple sequences of

q

k

from that model, truncated at a sufficiently large value of

k

, and

then average

E

[

X (t)

] across sequences. An alternative heuristic is to replace each

B

k

with its mean.

This approximation will be most accurate when the variance in

B

k

is very small, which, as we will

show later, is the case in our empirical application. This approximation is not needed to estimate the

model itself, but only to calculate the expected number of transaction without resorting to the use of

simulations.

A conceptually useful expression is the probability that a customer is still active at time T.

P (A) =

2

6

6

6

6

4

1

a + T t

1

a + t

x

t

1

!

r+x1

1

b + B

x

b + B

x1

!

s

!

3

7

7

7

7

5

1

(5)

The derivation for Equation 5 is in Appendix A.

A manager might also want to know how many orders he can expect from an existing customer,

during the next

t

⇤

periods, given an observed transaction history. In Appendix A, we show that this

posterior expected number of future transactions is

E

⇤

[X (t

⇤

)| x, t

x

] = P (A) ⇥

1

X

k=1

B

x

+ b

B

x

+ B

k

+ b

!

s

H

B

t

⇤

t

⇤

+ a + T t

1

; k, r + x 1

!

(6)

In Equation 6, the index of the summation

k

refers to the potential orders that are made after

time

T

. As discussed previously, we can either model

B

k

so that we may simulate future values of

B

k

explicitly, or substitute

E(B

k

)

as an approximation. The prior and posterior probability mass

functions for the number of orders (i.e., to express the probability of placing a particular number of

orders during some future number of weeks) are included in Appendix B, which is available as part

of the online supplement.

While it is useful to know the expected number of future orders, orders are placed at different

times. One order may be placed at time

T +

1, the next order may not be placed until a point in

time that is well into the future. Given the time value of money, orders that occur soon are more

11

valuable than orders that are placed later. Therefore, an appropriate metric for the expected number

of a customer’s future transactions should discount those transactions back to the present. The

value for discounted expected residual transactions (DERT) is proportional to a customer’s residual

lifetime value when the margin is constant (Fader, Hardie, and Shang 2010). Let

be a discount

factor that captures the time value of money, so a dollar earned

t

weeks from now is worth

t

today

(for notational simplicity, we reset the counter of

t

so

t =

0 at

T

, and we assume that payments are

made at the end of the week). The posterior estimate for the DERT of this customer is the sum of

discounted incremental expected orders.

DERT =

1

X

t=1

✓

E

⇤

[X (t)|x, t

x

, B

x

, T] E

⇤

[X (t 1)| x, t

x

, B

x

, T]

◆

t

= P (A)

1

X

k=1

B

x

+ b

B

x

+ B

k

+ b

!

s

⇥

1

X

t=1

t

"

H

B

t

a + T t

1

+ t

; k, r + x 1

!

H

B

t 1

a + T t

1

+ t 1

; k, r + x 1

!#

= (1 )P (A)

1

X

k=1

B

x

+ b

B

x

+ B

k

+ b

!

s

1

X

t=1

t

H

B

t

a + T t

1

+ t

; k, r + x 1

!

(7)

These future transactions depend on a number of different elements. The parameters

r

,

a

,

s

and

b

capture the distribution of order rates and baseline churn likelihoods across the population (e.g.,

for any randomly chosen member of the population,

E() = r/a

and

E(✓) = s/b

). Through

P (A)

,

customers with low

t

x

and high

x

might be more likely to have already become inactive, so there is

a low probability of these individuals conducting transactions in the future. Customers with high

x

and high t

x

are more likely to be alive, and to order often, so their DERT should be high.

Like all statistical models, this model is intended as a schematic of the actual data-generating

process. To give the model some useful parametric structure, we treat the latent attrition process as a

manifestation of a random variable. Though one can always propose more complicated versions of

a model, such as allowing for duration dependence in purchase times or contagion across customers

in their propensities to churn, we favor parsimony so as to avoid overparameterizing the model given

certain limitations in a typical transactional dataset.

12

3 Empirical Analysis

The context in which we study the role of quality on customers’ future transactions is that of an

online market for freelance writing services. The firm in question operates a website on which

customers can post orders for “jobs,” and from which writers can claim jobs to complete. The types

of jobs vary greatly. One example would be a 100-word description of a product that the customer,

an online retailer, is selling on her website. Another is a 500-word summary of what participants at

a conference might do for fun when exploring the host city. Orders include all of the information a

writer would need to complete the job: the topic area (e.g., sports, health), intended audience, word

count, and so forth. Customers are encouraged to be as specific as possible in their requirements,

as that makes it more likely the customer will be satisfied with the results. In our taxonomy, we

consider an order to be equivalent to the posting of a job.

Customers also choose a minimum rating, or grade, for the writers who are eligible to claim the

order. The firm maintains a bank of reviewers who screen and rate the writers who register with

the website. These reviewers are employed directly by the firm, and are considered to be experts

in evaluating prose (many have Masters of Arts degrees, or similar qualifications). Upon initial

application, a writer submits a writing sample, and a reviewer rates the writer as A, B, C or D. The

firm’s website provides examples of work from the different rating categories, so customers have a

general idea about the differences to expect across the different ratings. Ratings differ according to

objective criteria such as accuracy, grammar, style and vocabulary. A D-rated wr iter might produce

work with errors and simple sentence structure with no creative insight, while work from an A-level

writer will be of professional quality.

Customers pay, and writers earn, on a per-word basis, where the charge for each word depends

on the rating in the order. The firm claims a fixed percentage of this fee, plus a small (less than a

dollar) charge per order. Writers claim jobs from a list on a first-claim basis, so there is no bidding

involved. Wr iters may claim jobs that are rated below their own ratings (e.g., an A-rated writer

can choose a project from any level, but a B-rated writer cannot choose an A-rated order). In such

cases, writers are paid the lower per-word fee. The company has told us that it has not experienced

13

shortages of writers, with most job specifications being claimed within a day. Writers have another

day to complete the job, and nearly all jobs are completed within 24 hours of posting.

Sometime after the writer returns the completed job to the customer, the firm’s bank of reviewers

assigns each job a grade. Customers are not involved in this grading process, and neither customers

nor writers ever see the grade for a particular job. However, a writer’s rating can be adjusted

according to his grade history. This gives the writer an incentive to complete the job well; the grades

determine if the writer’s rating is adjusted up or down. The reviewers try to rate jobs as accurately

and objectively as possible, as a way to ensure that customers receive the quality they pay for, and to

reclassify writers as necessary. Writers can only be elevated to the A level manually, so the firm

classifies all A-rated and B-rated jobs together in an A/B class. Reviewers may also assign a grade

of E for completed jobs that do not meet even minimum standards.

3.1 Data summary

Our master dataset includes all completed jobs from the launch of the company in June 2008 to the

end of our observation period at the end of July 2011. We are restricting our analysis to customers

in either the United States or Canada whose first order takes place before the end of 2010, and to

jobs for which the language is English. This dataset contains information on 24,059 completed jobs

that were ordered by 3,048 distinct customers. For each job, we have identifiers for the customer

and writer, the day that the order was placed, some other details of the job specification. We also

have the requested rating of the job, as well as the grade the job received from the bank of reviewers.

Table 1 shows the number of jobs requested at each quality rating, and the quality grade of the work

that the writer delivered to the customer. By exploiting variation in the ratings, we can examine the

impact of quality level delivered (assessed objectively by the reviewer), relative to the level that was

requested by the customer, on customers’ future transactional activity.

All observed transactions for a particular customer occur from the day of a customer’s first order

(

t

1

), until the end of our observation period (

T

). Treating the time of initial trial as the beginning of

the customer relationship is consistent with prior research in customer base analysis (Schmittlein,

14

Post-hoc quality grade

A/B C D E Total

A 773 9 0 0 782

Requested B 8784 614 6 1 9405

Rating C 2050 5714 257 16 8037

D 1668 3270 814 83 5835

Total 13275 9607 1077 100 24059

Table 1: Number of jobs requested at each quality rating, and the quality grade of the work that the writer

delivered to the customer.

Morrison, and Colombo 1987; Fader and Hardie 2001; Fader, Hardie, and Lee 2005a). If a customer

places

x

orders during that observation period, his observed “frequency” is equal to

x/(T t

1

)

.A

customer’s “recency” is

t

x

, the week of the most recently observed order. Each day is represented as

1/7 of a week.

To control for the possibility that some of the firm’s earlier adopters might behave differently

than those customers whose first order came later, we divide the customer base into four cohorts

based on the week of the first order. The 588 customers who placed their first order during the first

33 weeks of our data are considered to be in the first cohort. The 568 customers who placed their

first order between weeks 33 and 66 are assigned to the second cohort. The 911 customers placing

their first orders between weeks 66 and 99 are assigned to the third cohort, and the 981 customers

placing their first orders between weeks 99 and 130 are assigned to the fourth cohort.

3.2 Model estimation

In this example, the transaction attr ibutes represent the requested and delivered quality of the jobs.

Although there are many functional forms that we could choose, we consider models of the form

log q

k

=

0

z

k

, where

z

k

is a vector of job-specific covariates and

is a vector of coefficients. Effects

that increase q

k

increase the probability of churn.

The elements of z

k

include the following:

- z

first

: a indicator of the customer’s first job;

- z

coh2

, z

coh3

, z

coh4

: indicators for time-invariant cohort effects;

15

- z

Ak

, z

Ck

, z

Dk

: indicators for the requested quality level of job k;

- z

Lk

,

z

Hk

: indicators for whether job

k

was lower (L) or higher (H) than the requested service

level; and

- z

LD

, z

HD

, z

LC

: interactions among requested and delivered quality ratings;

All coefficients, except those on

z

Lk

and

z

Hk

, are stationary. The coefficients

Lk

and

Hk

represent the effect on the churn probability from missing or exceeding the specifications of job

k

.

These effects can change from job to job, according to the customer’s recent experience. To capture

how these sensitivities change, we define a set of six

⌘

parameters that affect

Lk

and

Hk

in the

following ways:

L,k+1

=

Lk

+ ⌘

L

+ ⌘

LL

z

Lk

+ ⌘

HL

z

Hk

(8)

H,k+1

=

Hk

+ ⌘

H

+ ⌘

LH

z

Lk

+ ⌘

HH

z

Hk

(9)

The coefficient

Lk

changes by

⌘

L

regardless of the rating given to job

k

, capturing a drift in

customers’ sensitivity to receiving a lower-than-requested service level. The terms

⌘

LL

and

⌘

HL

capture the extent to which customers’ sensitivity to receiving a lower-than-requested service level

on job

k +

1 is affected by receiving a lower (

⌘

LL

) or higher (

⌘

HL

) level of service than was requested

for job

k

. The coefficient

Hk

evolves in a similar manner. By allowing

to be dynamic in this

way, we allow for customers’ responses to service quality to be affected by a customer’s experience

(Bolton 1998). For example, if

⌘

LL

were positive, then after having a bad experience with the firm,

a customer would be even more sensitive to subsequent bad experiences.

To assess the role of ser vice quality on churn propensities, we tested three variants of the model.

Model 3 is the full model as described. Model 1 is a “baseline” model that ignores all service quality

effects. Model 2 is similar to Model 3, with all of the insignificant ⌘ parameters removed.

Table 2 contains descriptions of the model parameters, along with maximum likelihood estimates

and standard errors. The subscripts for the elements of

in the table correspond to those of

z

. The

most interesting estimates are those on

L1

and

⌘

LL

, which are both positive. This result suggests

16

Model 1 Model 2 Model 3 Description

est se est se est se

r 0.90 0.04 0.90 0.04 0.90 0.04 shape parameter on

a 0.77 0.04 0.77 0.04 0.77 0.04 scale parameter on

s 1.09 0.07 1.08 0.07 1.10 0.07 shape parameter on ✓

b 1.13 0.19 1.14 0.19 1.17 0.20 scale parameter on ✓

first

-0.22 0.07 -0.22 0.07 -0.21 0.07 effect of customer’s first job

coh2

-1.15 0.11 -1.16 0.11 -1.15 0.11 fixed effect for cohort 2

coh3

-1.00 0.10 -1.01 0.11 -1.00 0.11 fixed effect for cohort 3

coh4

-0.81 0.11 -0.81 0.11 -0.80 0.11 fixed effect for cohort 4

A

0.88 0.11 0.89 0.11 0.89 0.11 effect for requested quality level A

C

-0.30 0.06 -0.27 0.07 -0.27 0.07 effect for requested quality level C

D

-0.51 0.08 -0.36 0.15 -0.37 0.15 effect for requested quality level D

L1

0.19 0.13 0.21 0.14 effect for rating being “lower” than requested

H 1

0.01 0.09 0.01 0.10 effect for rating being “higher” than requested

LD

0.21 0.36 0.24 0.38 interaction effect between “lower” and requested level D

HD

-0.18 0.17 -0.15 0.17 interaction effect between “higher” and requested level D

LC

-0.53 0.26 -0.52 0.26 interaction effect between “higher” and requested level C

⌘

L

-0.01 0.01 evolution parameter on

L

⌘

H

0.00 0.01 evolution parameter on

H

⌘

LL

0.18 0.12 0.29 0.21 evolution parameter on

L

after a “lower” rating

⌘

LH

0.05 0.13 evolution parameter on

H

after a “lower” rating

⌘

HL

0.01 0.04 evolution parameter on

L

after a “higher” rating

⌘

HH

-0.01 0.02 evolution parameter on

H

after a “higher” rating

Table 2: Parameter estimates

that, as expected, missing the requested level of service for the first job increases the probability of

churn. It also suggests that the magnitude of that effect will be larger for the next job with a missed

service level. Thus, the churn probabilities increase across jobs when customers repeatedly receive

lower-than-requested service.

We also see that

H1

, and the associated

⌘

parameters, are not significantly different from zero.

This asymmetry in the effect of service quality on customers’ tendency to churn is consistent with

losses looming larger than gains (Kahneman and Tversky 1979; Hardie, Johnson, and Fader 1993).

Our findings are also in line with prior research by Bolton (1998), who found that perceived losses

adversely impact the duration of a customer’s relationship in a contractual setting while perceived

gains did not have a significant impact on the duration of the relationship.

17

3.3 Model assessment

We compare the performance of the three model specifications using a series of assessments. A

likelihood ratio test suggests a weak preference for Model 2 over Model 1 (

2

6

=

11

.

0

, p = .

088);

we cannot infer a preference for Model 3 over Model 2 (

2

5

=

1

.

29

, p = .

936), or for Model 3

over Model 1 (

2

9

=

10

.

1

, p = .

342). One shortcoming of relying only on the likelihood ratio test,

however, is that it does not consider the extent to which the incorporation of transaction attributes

improves forecasting performance. Thus, in addition to the likelihood ratio test, we compare model

performance using two additional measures of fit.

We calculated the mean absolute percentage error (MAPE) associated with the models’ prediction

of the weekly number of repeat orders made by customers in our sample and the root mean squared

error (RMSE) for the models’ predictions of the distribution of the number of orders made by the

sample. We find that the MAPE is similar across model specifications, with Models 2 and 3 having

slightly lower errors compared to Model 1. In terms of the RMSE, we again find evidence to suggest

that the transaction attributes contribute to model fit. Models 2 and 3 have lower RMSEs compared

to Model 1 for the data used to estimate the model during the calibration and forecasting periods.

Using a holdout sample for cross-validation reveals that, while Model 2 has a lower RMSE than

Model 1, Model 3 has a higher RMSE during the forecasting period which would suggest that the

model is overparameter ized.

Details of these posterior predictive tests are in Appendix C, which as available as part of the

online supplement. Taken together with the likelihood ratio test, we believe that the posterior

predictive tests provide evidence that transaction attributes improve model performance and

contribute to forecasting accuracy. Based on these analyses, we focus on the results using Model 2

for the remainder of our discussion.

To provide a better sense for how well the proposed model captures customers’ observed behavior,

the panels in Figure 1 illustrate model fit at the aggregate level. Figure 1a plots the cumulative and

incremental number of weekly orders, for both in-sample and holdout populations. The vertical

lines at Week 130 divide the calibration and forecast time periods. We used only data to the left of

18

the lines for estimating the model parameters, and we included only those customers whose initial

order was before Week 130. Model 2 does well in tracking the number of orders from week to week.

In Figure 1b, we compare the histogram of pre-customer order counts with the distribution of counts

from Model 2 predicts. Again, Model 2 appears to fit rather well.

At the level of an individual customer, one managerially relevant test statistic is the probability

that a customer will place an order sometime in the future. While the probability of being active,

P (A)

, is a commonly used construct in customer base analysis, we cannot use it as a model checking

tool because we cannot observe the customer’s activity state directly. Instead, the appropriate metr ic

is

P

⇤

(

0

) = P(X

⇤

(t

⇤

) =

0

|x, t

x

, ·)

, the posterior probability that a customer will place no orders

during a forecast period. We test how well Model 2 predicts which customers will order during the

forecast period using a calibration plot. First, we assign each customer to one of 15 “bins”, according

to the customer’s posterior

P

⇤

(

0

)

. A customer is assigned to bin

i

if

(i

1

)/

15

< P

⇤

(

0

) i/

15

for

i =

1

...

15. Next, we compute the observed proportion of customers in each bin who do

not place an order during the forecast period. We consider the model to be well-calibrated if

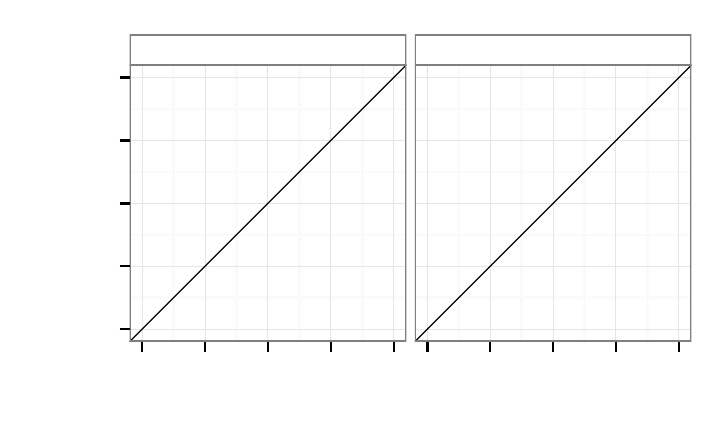

the predicted probabilities and observed proportions are aligned. Figure 2 confirms that they are.

Each dot represents the membership of the bin. The

x

-coordinate is the midpoint of the bin, and

the

y

-coordinate is the observed incidence of “no orders” for the members of that bin. “Perfect”

calibration would have occurred if all of the dots fell exactly on the 45° line. Of course, we expect

some random variation around this line, so we can still be confident that Model 2 forecasts the

incidence of future orders, at the customer level, quite well.

3.4 Forecasting quality data

In Section 2.1 we discussed the need to model the sequences of covariates for the purpose of

estimating conditional expectations and DERT rather than simply plugging in a fixed value. The

specifics of such a model depend on the context. For this dataset, there are two sources of variation

in the covariates: the ser vice level that a customer requested and the level that was delivered. For the

“requested” model, we assume that each customer has a latent, stationary probability of placing A, B,

19

Calibration Sample

Holdout Sample

0

5000

10000

15000

0.0

0.1

0.2

0.3

0.4

0.5

Cum. Repeat Orders

Incremental Orders / Trier

0 50 100 150 0 50 100 150

Week Since Launch (Forecast period begins Week 130)

Orders

model

Observed

Model 2

(a) Weekly incremental repeat orders per previously acquired customer. The vertical line is at Week 130, the

end of the calibration period and the start of the forecast period.

Calibration Sample

Holdout Sample

0

200

400

600

0

500

1000

1500

2000

Calibration Period

Forecast Period

0 1 2 3 4 5 6 7 8 9 10111213+ 0 1 2 3 4 5 6 7 8 9 10111213+

Number of Orders

Number of Clients

model

Observed

Model 2

(b) Observed and predicted histograms of orders.

Figure 1: Fit and forecast assessment for Model 2.

20

Calibration Sample

Holdout Sample

●

●

●

●

●

●

●

●

●

●

●

●

●

●

●

●

●

●

●

●

●

●

●

●

●

●

●

●

●

●

0.00

0.25

0.50

0.75

1.00

0.00 0.25 0.50 0.75 1.000.00 0.25 0.50 0.75 1.00

Probability of no orders during forecast period

Observed proportion of clients with

no orders during forecast period

Figure 2: Predicted vs observed probability of a particular customer making no orders during the forecast

period.

C or D-rated orders. This probability vector is heterogeneous and varies across customers according

to a Dirichlet distribution, allowing some customers to always choose the same rating, while other

customers vary more in their choices. Under the further assumption of a zero-order choice process,

we can infer the likelihood of a particular order pattern by using the maximum likelihood estimates

of a Dirichlet-multinomial mixture model.

The Dirichlet-multinomial parameters for this dataset are .04, .26, .22 and .12 for ordered

ratings A, B, C and D, respectively. These low values (all less than one) suggest high polarization

in the Dirichlet mixing distribution; even though there may be variation across customers, a

single customer is likely to place orders for the same level of quality across the jobs he orders.

To simulate hypothetical orders, we sample a probability vector from each customer’s posterior

Dirichlet distr ibution. Since most customers order at the same rating level every time, these posterior

probabilities are even more concentrated on a single quality level compared to the choice probabilities

of the prior distribution. We then use the empirical distribution of the job grades for each rating

level to get the service level delivered for each simulated job. In general, we find that there is little

variation in B

k

across simulated sequences of z

k

.

21

4 How Transactional Patterns Affect DERT and Incremental

DERT

Using the parameter estimates of Model 2, we can examine how infor mation from transaction

attributes affects expectations of the future transactional activity of heterogeneous customers.

Specifically, we examine how falling short of the expected level of service affects DERT, for

customers with different frequency (

x

) and recency (

t

x

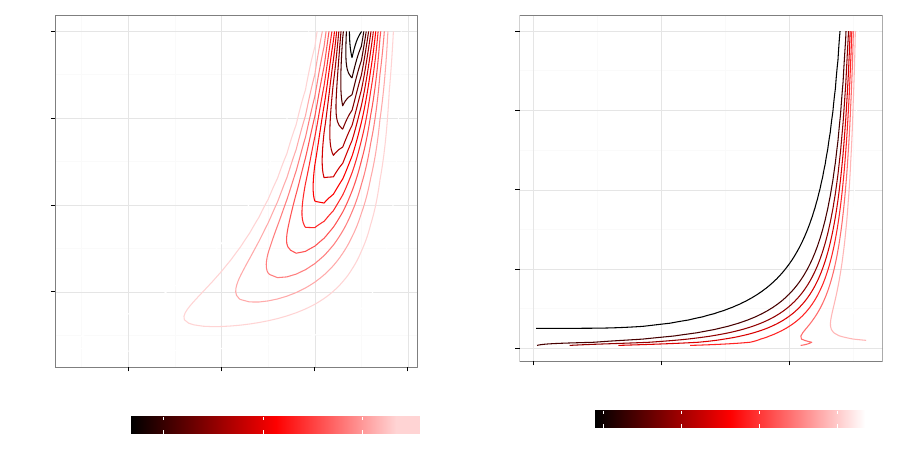

) data. Figure 3 plots the contours that connect

the same levels of DERT at

T =

130 for hypothetical customers who placed the first order at time

t

1

=

1, and who requested quality grades B, C or D for the most recent order. For each of requested

service levels, we consider delivered service levels that are lower than, or the same as, what was

requested for that most recent order. We assume that the level of service delivered was the same as

what was requested for all other orders placed by the customer. These iso-value cur ves are similar

in spirit to those introduced by Fader, Hardie, and Lee (2005b) for the Pareto/NBD model. Since

DERT is a posterior expectation based affected by the likelihood that a customer remains active,

as anticipated, we see “backward-bending” contours (Fader, Hardie, and Lee 2005b). When the

number of orders is large and the most recent order was in the distant past, it is more likely that the

customer has already become inactive than if the x

th

order was made more recently.

The iso-DERT curves in Figure 3 reveal the relationship between customers’ transaction histories

and expected future activity, but they do not show the incremental effect of missing the requested

service level. To assess the incremental impact of deviations in the level of service on expected

future transactions, we calculate the difference in DERT between what we would expect when the

most recent job is rated at the same level of service the customer ordered and what we would expect

if the level of service delivered was lower. We refer to this difference as “incremental DERT.” This

metric offers a long-term assessment of the marketing investment’s impact, and forms an upper

bound on the amount the fir m should invest. In transactions for which incremental DERT is small, it

may not be worth the firm’s effort to monitor and evaluate the service encounters. Those transactions

for which the incremental DERT is large, however, may warrant additional resources to ensure the

22

Rating Lower

Rating as Ordered

10

20

30

10

20

30

10

20

30

Job Ordered D

Job Ordered C

Job Ordered B

90 100 110 120 130 90 100 110 120 130

Week of last order

Number of orders during calibration period

1

2

3

4

5

level

Figure 3: DERT iso-value curves for hypothetical customers whose first order came at

t

1

=

1. The panels

condition on the ordered job quality, and whether the last job was rated lower or the same than what was

ordered. The

x

axis of each panel is the week number of the most recent order (

T =

130), and the

y

axis is the

number of observed orders.

23

appropriate level of service is delivered. In our empir ical context, incremental DERT can be viewed

as the penalty associated with delivering a level of service lower than what a customer requested.

The expected cost of missing a requested service level for a brand new customer is the incremental

DERT when

x =

1 and

t

1

= t

x

= T

. That is, immediately after the first job is ordered and a

new customer comes under observation, incremental DERT is the number of discounted future

transactions that we expect to be lost if the delivered service level were below what was requested.

For this par ticular dataset, the percentage change is 2.9% for new customers who ordered a B-level

job, 2.5% for a C-level job, and 2.2% for a D-level job. For existing customers, incremental DERT

depends crucially on how many orders the customer has placed and how long ago his last order

was made. Figure 4 shows this relationship in the form of “iso-incremental DERT” curves for a

customer who has requested a service level of B, in both absolute and percentage terms, for

t

1

=

1

and

T =

130. The levels of these curves represent the incremental DERT, evaluated at varying levels

of frequency and recency. The darker contours represent differences that are more negative, for

which the mismatch in service levels has more of an effect.4

In absolute terms, at a given level of frequency, falling short of the requested service level

appears to have the greatest effect when recency is neither too high nor too low. Take the case of a

customer who has conducted a given number of transactions. If the last transaction was conducted

recently, it is likely that the customer is still active. Regardless of whether the service delivered was

at or below the level requested, the recency of the transaction leads us to estimate a high DERT

for that customer. Alternatively, if the order were placed at a time in the distant past, the customer

is more likely to have already defected, regardless of the service quality level, so we estimate a

low DERT. In both of these cases, the difference in DERT between the case in which the service

delivered matches what was requested and the case in which it is below that which was requested

will be small compared to the incremental DERT for a customer with moderate recency. For those

customers, there is more uncertainty about whether the customer is still active. Small differences in

attrition probabilities will yield more substantial decreases in DERT when the requested service

4

We observe a similar pattern as depicted in Figure 4 for jobs that exceed the order specifications, except with

positive differences in DERT. However, for this dataset, the magnitude of the effect is very small.

24

25

50

75

100

100 110 120 130

Week of last order

Number of orders during calibration period

−0.06 −0.04 −0.02

Incremental

DERT

(a) Absolute difference

0

25

50

75

100

0 50 100

Week of last order

Number of orders during calibration period

−8% −6% −4% −2%

Percent

Incremental

DERT

(b) Percent difference

Figure 4: Iso-incremental DERT curves when missing the requested ser vice level. Observed recency is on the

x-axis and frequency is on the y-axis. Each curve connects points for which the incremental DERT is the

same.

level is missed. We see that the range of incremental DERT is the widest at low or moderate order

frequencies.

Figure 4b illustrates the DERT contours in percentage terms. As shown in Figure 4a, for a given

number of orders

x

, there are two values

t

x

that correspond to the same absolute difference in DERT.

As DERT increases with recency for a given value of

x

(as shown in Figure 3), incremental DERT

on a percentage basis will be smaller at higher values of recency.

Figure 4 demonstrates that the expected difference in a customer’s remaining value between

meeting and falling short of the requested service level depends on both the recency and frequency

of the customer’s transactions. When the goal of CRM is to identify those customers for whom

targeted marketing actions generate the greatest financial impact, our findings should caution against

scoring customers solely on popular measures like P(Alive) or CLV. While the most recent and

frequently transacting customers are likely to be the most valuable, the effect of transaction attributes

is not much different from customers who last purchased a long time ago.

To provide another perspective on customers’ remaining value, Figure 5 shows incremental

25

DERT (absolute in Figure 5a, and percent in Figure 5b) as a function of frequency, for select

values of recency. That is, each curve corresponds to a vertical slice of either Figure 4a or 4b.

For transaction histories with lower recency (e.g.,

t

x

=

85 and

t

x

=

100), we observe an initial

increase in the magnitude of the incremental DERT (in absolute terms) as the number of orders

increases. But, with a very large number of orders, the magnitude of incremental DERT decreases

and approaches zero. This patter n reveals the interplay of two factors. First, the large number of

orders is indicative of a high transaction rate (

). For these customers, missing the requested service

level puts a lucrative revenue stream at risk. But, with a large number of orders, the low recency of

the last order suggests that the customer may have already become inactive. Given that the increased

likelihood that the customer has already lapsed, the increased cost associated with missing the

requested service level is lower, resulting in the reduced magnitude of incremental DERT. At the

highest level of recency (

t

x

=

130), the customer is known to be still active, and DERT increases

with the number of orders. We thus observe that the magnitude of incremental DERT increases with

frequency, but at a much slower rate.

Figure 5b presents a similar analysis in percentage terms. At the highest level of recency

(

t

x

=

130), when the customer has just conducted a transaction and is known to still be active, DERT

increases with frequency. Therefore, incremental DERT, while relatively flat in absolute terms,

falls when expressed as a percentage of DERT. For the remaining three levels of recency, higher

transaction frequency ultimately results in a higher magnitude of incremental DERT as a percentage.

As the number of transactions increases along these three curves, so too does the likelihood that these

customers have already become inactive, thereby driving down DERT. With incremental DERT (in

absolute terms) being compared to a smaller base, the incremental DERT increases as a percentage.

Prior research has suggested that the value of CRM tools lies in their ability to facilitate learning

about customers (Mithas, Krishnan, and Fornell 2005), and that this value is limited based on the

quality of infor mation the firm has available about its customers (Homburg, Droll, and Totzek 2008).

Our findings reveal that differences in customer value that are associated with variation in transaction

attributes (e.g., the level of service delivered on a transaction) depend on customers’ past transaction

26

−0.020

−0.015

−0.010

−0.005

0.000

0 25 50 75 100

Number of Orders

Incremental DERT

Week of

last order

85 100

115 130

(a) Absolute difference

−8%

−6%

−4%

−2%

0%

0 25 50 75 100

Number of Orders

Percentage Incremental DERT

Week of

last order

85 100

115 130

(b) Percent difference

Figure 5: Absolute and percent incremental DERT as a function of frequency, for different levels of recency.

activity. If a customer is more obviously active or inactive deviations from the requested service

level provide little information on the customer’s DERT. It is when there is increased uncertainty as

to whether a customer is active or inactive that the level of service delivered relative to that which

was requested allows us to learn more about a customer’s DERT. To the best of our knowledge, our

research is the first to explore the value of transaction attributes using the latent attrition models

frequently employed in customer base analysis and customer valuation, and how past activity affects

the differences in customer value associated with transaction attributes.

5 Discussion

We present a flexible latent attrition model that incorporates transaction attributes in customer base

analysis, and descr ibe an empirical application that defines those attributes as indicators for relative

service quality. The model allows us to derive “incremental DERT,” a metric of the discounted

expected return on changes in those attributes. For transactions that are about to happen immediately,

incremental DERT can serve as an upper bound on the amount a firm should invest to change one

27

of those attributes. We also describe patterns in the relationship between incremental DERT and

the recency/frequency profile of the customer. Understanding these patterns and quantifying the

effects allow a manager to more accurately estimate DERT for all members of the customer base.

Model parameters can be estimated using standard maximum likelihood methods and DERT can be

computed as a truncated summation.

As firms use customer base analysis and customer valuation models to score and rank customers

according to the value they hold for a firm (Wuebben and von Wangenheim 2008), managers should

be interested in tracking and compiling transaction attributes that may be informative of customers’

future value. Acquiring such information, however, often entails a cost. For example, firms may

incur costs to monitor their salesforce to ensure compliance with required activities (John and

Weitz 1989). A simple heuristic to identify those transactions in which firms should be willing to

invest more in monitoring could be customers’ purchase frequency. After all, such customers are

likely to be among the most valuable customers to a firm. Our results, however, suggest that for such

customers, the difference in discounted long-term value to the firm between meeting and falling

short of the requested service level (reflected by incremental DERT) is low for those customers. For

customers who have not conducted as many transactions, our estimates of their value to the firm

are more sensitive to information on the level of service delivered. It is these customers for whom

estimates of long-term value are most subject to change if the level of service in a transaction comes

up short of specifications.

In our empirical context, we see that the magnitude of the effect of missing specified levels of

service is larger than exceeding specified levels. This is consistent with the idea of losses looming

larger than gains. While extant research has questioned the wisdom of trying to delight customers

by exceeding their expectations, due to the possibility of raising customers’ future expectations

(Rust and Oliver 2000), our analysis suggests that coming up short of the service customers have

requested poses a greater risk to a customer’s continued relationship with the firm and the firm’s

ability to capture the corresponding revenue stream.

Using our framework as a foundation, there are a number of promising directions with which

28

research could continue. While we focus our attention on customer retention and the value of

existing customers, a similar modeling approach could be employed to jointly investigate customer

acquisition and retention (Schweidel, Fader, and Bradlow 2008; Musalem and Joshi 2009). Doing

so could provide firms with guidance for how to balance marketing expenditures across the two

activities (Reinartz, Thomas, and Kumar 2005). Another area to explore is the effect of strategic

investments in service quality, a practice that the firm that supplied our data did not employ. While it

may be costly for a firm to invest in improving service encounters and monitoring these encounters

for all customers, the firm may have resources to focus on select customers. The firm could use

incremental DERT as a criterion for selecting those target customers. If the costs of delivering better

than expected service experiences are the same across customers, such an allocation rule would be

equivalent to putting your money where it will deliver the most “bang for the buck.” These actions

would be consistent with the management principle of “return on quality.” (Rust, Zahorik, and

Keiningham 1995). In many cases, we would need to account for the firm’s actions when estimating

the effect on retention probabilities (Manchanda, Rossi, and Chintagunta 2004; Schweidel and

Knox 2013). To alleviate such concerns, one might choose to proceed in this research area with a

carefully designed field experiment.

Another area for future research would be to develop further means of accounting for variation in

the effect of customer-firm touch points on future customer behavior. While we rely on observable

transaction attributes (i.e., the requested and evaluated service levels) as a means of evaluating

the level of service, future work may explore if such a measure could be inferred with additional

information about the transaction. For example, in our empirical context, if the transaction data

indicated the writer who completed each job, the firm may be able to evaluate the “quality” of each

writer based on the effect they have on customer churn. Another example of a firm that offers a

marketplace is eBay, which connects buyers and sellers. Evaluating sellers based on the churn of

buyers who have recently interacted with them may provide an indication of which sellers should be

rewarded versus which sellers are potentially costing the firm business.

A cost of conducting such an analysis is the detail in the data that must be collected. While

29

the early latent attrition models that appeared in the marketing literature relied on recency and

frequency as sufficient statistics, as in our analysis, recognizing the variation in customer tendencies

that exist across transactions require data be tracked at the transaction level. It is an empirical

question as to extent to which incorporating such sources of variation into the analysis will affect

managerial decisions. As the answer to this question may vary from context to context, additional

research across a range of empirical applications is warranted, recognizing the costs associated with

acquiring and analyzing data on customer-fir m interactions.

Appendices

A Derivations

In this section, we use the definitions and symbols that are defined in Table 3.

(k) =

R

1

0

t

k1

e

t

dt

Gamma function

(k,) =

R

0

t

k1

e

t

dt

Lower incomplete gamma function

G

z

(r, a) = (r, az)/(r)

cdf of a gamma distribution with shape r and rate a

dG

z

(r, a) =

a

r

(r)

z

r 1

e

az

Density of a gamma distribution with shape r and rate a

B (k, r) =

R

1

0

u

k1

(1 u)

r 1

du

Beta function

B (z; k , r ) =

R

z

0

u

k1

(1 u)

r 1

du

Incomplete beta function

H

B (z; k , r ) = B (z; k, r) /B (k, r)

Regularized incomplete beta function (equivalent to cdf of beta

distribution with parameters k and r, evaluated at z)

2

F

1

(a, b, c; z)

Gaussian hypergeometric function

P (A|, ✓), P (A)

Conditional and marginal probabilities that a customer has not yet

churned by time T.

Table 3: Definitions of symbols and functions used in the paper.

To derive the marginal likelihood in Equation 3, we integrate the individual-level data likelihood

in Equation 1 over two gamma densities, one for and one for ✓.

30

L =

Z

1

0

Z

1

0

f (x, t

2:x

|, ✓, q

1:x

)dG

(r, a)dG

✓

(s, b)

=

Z

1

0

Z

1

0

x1

e

(t

x

t

1

)✓ B

x1

f

1 e

✓q

x

⇣

1 e

(Tt

x

)

⌘g

a

r

(r)

r1

e

a

b

s

(s)

✓

s1

e

b✓

dd✓

=

a

r

(r)

b

s

(s)

Z

1

0

r+x2

e

(a+t

x

t

1

)

d

Z

1

0

✓

s1

e

✓(b+B

x1

)

d✓

a

r

(r)

b

s

(s)

Z

1

0

r+x2

e

(a+t

x

t

1

)

d

Z

1

0

✓

s1

e

✓(b+B

x

)

d✓

+

a

r

(r)

b

s

(s)

Z

1

0

r+x2

e

(a+Tt

1

)

d

Z

1

0

✓

s1

e

✓(b+B

x

)

d✓

=

(r + x 1)

(r)

a

r

(a + t

x

t

1

)

r+x1

b

b + B

x1

!

s

2

6

6

6

6

4

1

b + B

x1

b + B

x

!

s

*

,

1

a + t

x

t

1

a + T t

1

!

r+x1

+

-

3

7

7

7

7

5

(10)

By rearranging terms, we can write the marginal likelihood equivalently as

L =

(r + x 1)

(r)

a

r

(a + T t

1

)

r+x1

b

b + B

x

!

s

2

6

6

6

6

4

1

a + T t

1

a + t

x

t

1

!

r+x1

1

b + B

x

b + B

x1

!

s

!

3

7

7

7

7

5

(11)

We can also compute the expected number of orders for any randomly chosen customer in the

population. Our approach draws inspiration from Section 4.3 in Fader, Hardie, and Lee (2005a).

Let

⌧

be the time of job immediately after which the customer churns. Therefore, conditional on

k

,

the probability that

⌧

is sometime after

t

is equal to the probability of surviving all

k

transactions

that occur red before

t

. This survival probability is

e

✓ B

k

. The probability of making

k

transactions

is a shifted Poisson (since k starts at 1). By summing over all possible values of k,

P(⌧>t) =

1

X

k=1

(t)

k1

e

t

(k 1)!

e

✓ B

k

(12)

31

By differentiating Equation 12 with respect to t, we get the pdf of ⌧.

g(⌧) =

1

X

k=1

e

✓ B

k

k1

(k 1)!

d

dt

f

t

k1

e

t