The authors of this chapter are Fabio Cortes, Mohamed Diaby, Caio Ferreira (co-lead), Nila Khanolkar, Harrison Samuel Kraus, Benjamin

Mosk, Natalia Novikova, Nobuyasu Sugimoto (co-lead), and Dmitry Yakovlev, under the oversight of Charles Cohen.

Chapter 2 at a Glance

• The chapter assesses vulnerabilities and potential risks to financial stability in corporate private credit, a rapidly

growing asset class—traditionally focused on providing loans to midsize firms outside the realms of either

commercial banks or public debt markets—that now rivals other major credit markets in size.

• Private credit creates significant economic benefits by providing long-term financing to firms too large

or risky for banks and too small for public markets. However, credit migrating from regulated banks and

relatively transparent public markets to the more opaque world of private credit creates potential risks.

• Firms borrowing private credit tend to be smaller and riskier than their public market counterparts,

and the sector has never experienced a severe economic downturn at its current size and scope. Such an

adverse scenario could see a delayed realization of losses followed by a spike in defaults and large valuation

markdowns.

• The chapter identifies vulnerabilities arising from relatively fragile borrowers, increased exposure of

pensions and insurers to the asset class, a growing share of semiliquid investment vehicles, multiple layers

of leverage, stale valuations, and unclear interconnections between participants.

• Assessing overall financial stability risks of this asset class is challenging because the data needed to fully

analyze these risks are unavailable. Despite these limitations, such risks appear contained at present.

• However, given private credit’s size and role in credit creation—now large enough to compete directly

with public markets—it may become macro-critical and amplify negative shocks to the economy.

• The rapid growth of private credit, coupled with increasing competition from banks on large deals and

pressure to deploy capital, may lead to a deterioration in pricing and nonpricing terms, including lower

underwriting standards and weakened covenants, raising the risk of credit losses in the future.

• If the asset class remains opaque and continues to grow exponentially under limited prudential oversight,

the vulnerabilities of the private credit industry could become systemic.

Policy Recommendations

• Encourage authorities to consider a more intrusive supervisory and regulatory approach to private credit

funds, their institutional investors, and leverage providers.

• Close data gaps so that supervisors and regulators may more comprehensively assess risks, including

leverage, interconnectedness, and the buildup of investor concentration. Enhance reporting requirements

for private credit funds and their investors, and leverage providers to allow for improved monitoring and

risk management.

• Closely monitor and address liquidity and conduct risks in funds—especially retail—that may be

faced with higher redemption risks. Implement relevant product design and liquidity management

recommendations from the Financial Stability Board and the International Organization of Securities

Commissions.

• Strengthen cross-sectoral and cross-border regulatory cooperation and make asset risk assessments more

consistent across financial sectors.

CHAPTER

THE RISE AND RISKS OF PRIVATE CREDIT

2

International Monetary Fund | April 2024 53

GLOBAL FINANCIAL STABILITY REPORT: THE LAST MILE: FINANCIAL VULNERABILITIES AND RISKS

54 International Monetary Fund | April 2024

How Private Credit Started and Has Grown

This chapter evaluates how financial stability is

affected by the recent evolution of private credit into

a major asset class. Private credit (see Table 2.1 for

definitions) has grown exponentially and is becoming

an increasingly important and interconnected part of

the financial system. The sector predominantly involves

alternative asset managers who raise capital from institu-

tional investors using closed-end funds and lend directly

to predominantly middle-market firms (Figure 2.1). This

chapter focuses on performing corporate credit rather

than distressed assets, infrastructure, and real estate.

Private credit has provided significant economic

benefits during its approximately 30-year existence.

It developed as a lending solution for middle-market

companies deemed too risky or large for commercial

banks and too small for public markets. Loans are

typically negotiated directly between borrowers and

one or more alternative asset managers. Although

usually more expensive than bank loans, private credit

offers borrowers a value proposition through strong

relationships and customized lending terms designed to

provide flexibility in times of stress.

1

In contrast with

most broadly syndicated loans, private credit offers

terms that include enhanced covenants providing lend-

ers with downside protection.

2

Private credit managers

also claim to have much greater resources to deal with

problem loans than either banks or public markets,

thereby enabling fewer sudden defaults, smoother

restructurings, and lower costs of financial distress.

Because private credit deals are idiosyncratic and

difficult for outside parties to value or trade, lenders

typically rely on long-term pools of locked-up capital

for financing.

Private credit has grown rapidly since the global

financial crisis, taking market share from bank lending

1

Customized lending terms can include, for example, the option

to capitalize interest payments (that is, pay in kind) in times of

poor liquidity.

2

Covenants can vary depending on the transaction and can

include, for example, limits for leverage and interest coverage ratios,

restrictions on capital expenditures and dividend distributions,

restrictions on additional debt, and limitations on asset sales.

Private credit funds are intermediaries between end investors and

corporate borrowers that offer floating rate loans to middle-mar

ket firms.

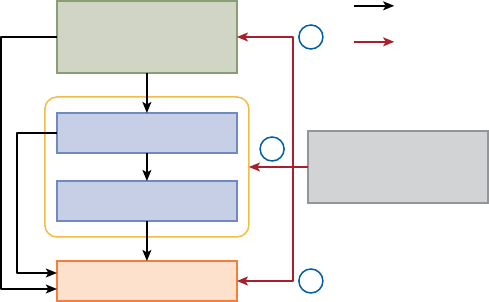

Figure 2.1. Private Credit Structure

Private Credit, End Investors, and Borrowers

Source: IMF staff.

Note: GP = general partners; LP = limited partners.

Borrowers

•

Middle-market

firms

•

Close to

syndicated loan

universe

Intermediaries

•

Limited maturity

transformation

•

Leverage

provided by

banks

PFs

Pension

funds

ICs

Insurance

corporations

SWFs

Sovereign

wealth

funds

Retail

Funds

Closed-ended

GP/LP

structure

Floating rate loans

Covenant heavy/heavier

Degree of control; customized terms; few lenders

Corporates

Small and medium-sized firms; some highly leveraged

Funds

Open-ended

BDCs

Business

development

companies

CLOs

Collateralized

loan

obligations

Banks

End investors

•

Long-term

investment

horizon

•

Institutional

investors

•

High-wealth

individuals

Leverage

Table 2.1. Key Concepts and Definitions

Key Concept Definition

Private credit Nonbank corporate credit provided through

bilateral agreements or small “club deals”

outside the realm of public securities or

commercial banks. This definition excludes

bank loans, broadly syndicated loans, and

funding provided through publicly traded

assets such as corporate bonds.

Broadly syndicated loan A form of financing provided by a group of

lenders, often banks and other financial

institutions, to a single borrower. Loans are

syndicated when too large or risky for a

single lender. Such loans are structured and

arranged by one or more lending agents—

typically investment banks—that underwrite

and facilitate the transaction. Given the broad

investor base, larger syndicated loans typically

have a relatively deep secondary trading

market.

Leveraged loan A broadly syndicated loan with a high level of

corporate leverage. Such a loan is usually

rated below investment grade and has a high

credit spread.

Middle-market firm A firm that is typically too small to issue public

debt and requires financing amounts too

large for a single bank because of its size

and risk profile. The size of middle-market

firms varies widely. In the United States, they

are sometimes defined as businesses with

between $100million and $1billion in annual

revenue. In contrast to syndicated loans, loans

to middle-market firms are typically unrated,

even when multiple lenders are involved.

CHAPTER 2 THE RISE AND RISKS OF PRIVATE CREDIT

55International Monetary Fund | April 2024

and public markets. Private credit benefitted from

the long period of low interest rates that saw a huge

expansion of attention to alternative investment strategies.

In this context, private credit has appeared attractive,

with some of the highest historical returns across debt

markets and appears to be relatively low volatility

(Figure 2.2, panel 1). At the same time, postcrisis

regulatory reforms raised capital requirements for banks

and made regulation more risk sensitive, incentivizing

banks to hold safer assets. Some end investors (notably

insurance companies) were also incentivized to move

into private credit because the capital charges are lower

and less risk-sensitive than the charges applicable to

commercial banks (Cortes, Diaby, and Windsor 2023).

There is a concern that tighter bank regulation will

continue to encourage the migration of credit from banks

to private credit lenders (Cai and Haque 2024).

As banks appear to have become less willing to lend

to middle-market firms with riskier profiles in the

United States and Europe, private credit has emerged

as a key lender. Private credit assets grew to approxi-

mately $2.1 trillion globally in combined assets and

undeployed capital commitments in 2023, with a focus

on North America and Europe (Figure 2.2, panel 2).

3

3

This estimate of the growth in private credit assets includes the

assets of private credit funds ($1.7 trillion globally, as of 2023),

business development companies, and private collateralized loan

obligations, and therefore underestimates the overall size of private

credit globally. This is because some end investors also lend directly

to middle-market firms.

Private equity

Natural resources

S&P 500

Venture capital

Private credit

Real estate

MSCI World TR

Rest of the world

Europe

North America

Dry powder (undeployed capital)

North America managers

Asia managers Other managers

Europe managers

High-yield bonds

Private credit Leveraged loans

US private credit/bank credit (right scale)

Figure 2.2. Overview of Private Credit and Other Traditional Markets and Assets

Private credit funds have delivered comparatively higher gross

returns ...

1. Returns of Private Equity, Private Credit, and Other Asset Classes

(Indices rebased to 100 as of December 2000)

0

1,000

200

400

600

800

2000 02 04 06 08 10 12 14 16 18 20 22

... and grown exponentially over the past two decades.

2. The Growth of Private Credit Markets

(Trillions of US dollars)

0

2.4

0.4

0.8

1.2

1.6

2.0

2000 02 04 06 08 10 12 14 16 18 20 22

Private credit fund managers based in North America manage a

material part of the market in other regions.

3. Geographical Focus of Private Credit Funds’ Managers

(Percent, as of June 2023)

0

100

20

40

60

80

North America

focus ($1.1 trillion)

Europe focus

($460 billion)

Asia focus

($114 billion)

Other focus

($59 billion)

In the United States, private credit size is comparable to leveraged

loans and high-yield bond markets.

4. US Private Credit, Leveraged Loans, and High-Yield Bonds

(Trillions of US dollars, left scale; percent, right scale)

0

2.0

0.5

1.0

1.5

0

10

2

4

6

8

2001

03

05 07 09 11 13 15 17 19 21 23

Sources: Bank of America Global Research; Bloomberg Finance L.P.; PitchBook LCD; Preqin; S&P Capital IQ; and IMF staff calculat

ions.

Note: In panel 1, the private capital indices are rebased to 100 as of December 31, 2000, and are available until June 2023. In

panel 2, the measure of assets under

management includes those from private credit funds, business development companies, and middle-market collateralized debt obli

gations, with the last two being

mostly US focused, from 2000 to June 2023. In panel 4, bank credit includes both securities, and loans and leases for US commer

cial banks.

GLOBAL FINANCIAL STABILITY REPORT: THE LAST MILE: FINANCIAL VULNERABILITIES AND RISKS

56 International Monetary Fund | April 2024

For context, such assets are comparable to about

three-quarters of the global high-yield market, a more

mature but similarly risky market.

Although still focused on middle-market lending,

private credit has expanded its remit significantly over

the last 20 years, particularly over the last 5. As a result,

private credit firms in the United States and Europe can

now provide loans to much larger corporate borrowers

that would previously fund themselves through broadly

syndicated loans or even corporate bonds. Such

borrowers may now prefer the customized arrangement

of private credit that avoids the disclosures and costs

associated with public markets.

Private credit remains focused on North America,

but other regions, including Europe and Asia, are

experiencing similar growth dynamics. As of June 2023,

assets under the management (deployed and committed)

of private credit managers located in the United States

reached $1.6 trillion, growing at an average annual rate

of 20 percent over the last five years. Private credit now

accounts for 7 percent of the credit to nonfinancial

corporations in North America, comparable with

the shares of broadly syndicated loans and high-yield

corporate bonds (Figure 2.2, panel 4). In Europe,

private credit also increased rapidly at an average rate

of 17 percent per year over the same period, although

it has a smaller footprint of 1.6 percent of corporate

credit. There is evidence of cross-regional investments,

with North American managers financing a significant

portion of the private credit funds focused on Europe

and Asia (Figure 2.2, panel 3). Asian private credit

accounts for about 0.2 percent of credit to nonfinancial

corporations, although it has grown at 20 percent

annually over the last five years. Private credit in Asia

finances mostly smaller deals, targeting high-yield and

distressed segments that have limited financing options

in emerging market economies (Box 2.1).

Given the low liquidity, higher credit risk, and lack

of transparency of private credit, the space is dominated

by institutional investors. The most common private

credit investment vehicle, accounting for approximately

81 percent of the total market, is a closed-end fund

with a capital call structure and limited life cycle, similar

to funds used for private equity. An additional 5 per-

cent of the market consists of specialized collateralized

loan obligations (CLOs) that invest in middle-market

private credit.

4

Typical investors in these two vehicles are

pension funds, insurance companies, sovereign wealth

4

Sources: Preqin, S&P Capital IQ, and PitchBook LCD.

funds, and family offices. A rapidly growing segment

in the United States is known as business development

companies (BDCs), which account for 14 percent of

the market. BDCs (covered in greater detail later in the

chapter) are often public and open to retail investors.

In Europe, some funds have adopted more frequent

redemption periods (for instance, monthly or even more

often) to appeal to a wider investment base.

The growth in private credit has followed the rise in

private equity, with which it is closely linked. Manag-

ers whose umbrella firm is also active in private equity

hold more than three-quarters of private credit assets.

For about 70 percent of private credit deals, the bor-

rowing company is sponsored by a private equity firm.

How Private Credit Could Threaten

Financial Stability

This chapter assesses private credit vulnerabilities

and risks to financial stability and focuses on macrofi-

nancial imbalances that might amplify negative shocks

to the real economy (Adrian and others 2019). Specif-

ically, this chapter analyzes the risks from borrowers,

liquidity mismatches, leverage, asset valuations, and

interconnectedness.

The migration of credit provision from regulated

banks and relatively transparent public markets to

more opaque private credit firms raises several poten-

tial vulnerabilities. Whereas bank loans are subject to

strong prudential regulation and supervisory oversight,

and bond markets and broadly syndicated loans to

comprehensive disclosure requirements that foster

market discipline and price discovery, private markets

are comparatively lightly regulated and more opaque.

Private credit loans, furthermore, are unrated, rarely

traded, typically “marked to model” by third-party

pricing services, and without standardized terms for

contracts. Rising risks and their potential implications

may therefore be difficult to detect in advance.

Severe data gaps prevent a comprehensive assessment

of how private credit affects financial stability. The

interconnections and potential contagion risks many

large financial institutions face from exposures to the

asset class are poorly understood and highly opaque.

Because the private credit sector has rapidly grown, it

has never experienced a severe downturn at its current

size and scope, and many features designed to mitigate

risks have not yet been tested.

At present, the financial stability risks posed by

private credit appear contained. Private credit loans

CHAPTER 2 THE RISE AND RISKS OF PRIVATE CREDIT

57International Monetary Fund | April 2024

are funded largely with long-term capital, mitigating

maturity transformation risks. The use of leverage

appears modest, as do liquidity and interconnect-

edness risks.

The rapid growth of the asset class requires careful

monitoring. As private credit assets under management

grow rapidly, and competition with investment banks

on larger deals intensifies, supply-and-demand

dynamics may shift, thereby lowering underwriting

standards, raising the chance of credit losses in the

asset class, and rendering risk management models

obsolete. The private credit sector may also eventually

experience falling risk premiums and weakening

covenants as assets under management rise rapidly and

the pressure to deploy capital increases.

Immediate risks may seem contained, but the

sector has meaningful vulnerabilities, is opaque to

stakeholders, and is growing rapidly under limited

prudential oversight. If these trends continue, private

credit vulnerabilities may become systemic:

• Borrowers’ vulnerabilities could generate large,

unexpected losses in a downturn. Private credit is

typically floating rate and caters to relatively small

borrowers with high leverage. Such borrowers could

face rising financing costs and perform poorly in

a downturn, particularly in a stagflation scenario,

which could generate a surge in defaults and a

corresponding spike in financing costs.

• These credit losses could create significant capital losses

for some end investors. Some insurance and pension

companies have significantly expanded their invest-

ments in private credit and other illiquid invest-

ments. Without better insight into the performance

of underlying credits, these firms and their regula-

tors could be caught unaware by a dramatic rerating

of credit risks across the asset class.

• Although currently low, liquidity risks could rise with

the growth of retail funds. The great majority of

private credit funds poses little maturity transforma-

tion risk, yet the growth of semiliquid funds could

increase first-mover advantages and run risks.

• Multiple layers of leverage create interconnectedness

concerns. Leverage deployed by private credit funds

is typically limited, but the private credit value chain

is a complex network that includes leveraged players

ranging from borrowers to funds to end investors.

Funds that use only modest amounts of leverage

may still face significant capital calls in a downside

scenario, with potential transmission to their lever-

age providers. Such a scenario could also force the

entire network to simultaneously reduce exposures,

triggering spillovers to other markets and the broad

economy.

• Uncertainty about valuations could lead to a loss of

confidence in the asset class. The private credit sector

has neither price discovery nor supervisory oversight

to facilitate asset performance monitoring, and the

opacity of borrowing firms makes prompt assess-

ment of potential losses challenging for outsiders.

Fund managers may be incentivized to delay the

realization of losses as they raise new funds and

collect performance fees based on their existing track

records. In a downside scenario, the lack of trans-

parency of the asset class could lead to a deferred

realization of losses followed by a spike in defaults.

Resulting changes to the modeling assumptions

that drive valuations could also cause dramatic

markdowns.

• Risks to financial stability may also stem from inter-

connections with other segments of the financial

sector. Prime candidates for risk are entities with

particularly high exposure to private credit markets,

such as insurers influenced by private equity firms

and certain groups of pension funds. The assets

of private-equity-influenced insurers have grown

significantly in recent years, with these entities

owning significantly more exposure to less-liquid

investments than other insurers. Data constraints

make it challenging for supervisors to evaluate

exposures across segments of the financial sector and

assess potential spillovers.

• Increasing retail participation in private credit

markets raises conduct concerns. Given the specialized

nature of the asset class, the risks involved may

be misrepresented. Retail investors may not fully

understand the investment risks or the restrictions

on redemptions from an illiquid asset class.

Characteristics of Private Credit Borrowers

Private credit borrowers tend to be riskier than

their traded counterparts, such as high-yield bond and

leveraged-loan issuers. Borrowers in private credit are

also relatively vulnerable to interest rates, as loans have

floating rates. However, the support of private equity

sponsors and the relatively close and flexible relation-

ship between lender and borrower partially mitigate

liquidity and solvency risks. Collateralization and the

greater use of covenants provide additional protection

for investors.

GLOBAL FINANCIAL STABILITY REPORT: THE LAST MILE: FINANCIAL VULNERABILITIES AND RISKS

58 International Monetary Fund | April 2024

Reasons Firms Finance in Private Credit Markets

A key reason driving firms to private credit mar-

kets is challenges in accessing traditional funding

sources. Evidence suggests that weaker firms with low

or negative earnings and high leverage are less likely

to secure bank loans and are more inclined to borrow

from nonbank sources (Chernenko, Erel, and Prilmeier

2022). Private debt fund managers also believe that

they finance companies and leverage levels that banks

would not fund (Block and others 2023). In addition,

borrowers in the private credit market may be excluded

from the syndicated loan market because of their size

or their lack of high-quality collateral for bank lenders.

Private credit can also offer benefits in flexibility,

speed of execution, and confidentiality. Aspects of

each transaction, such as the repayment schedule and

collateral requirements, can be tailored to the par-

ties involved. Compared with traditional bank loans

and public debt offerings, private credit transactions

are often executed more quickly and provide

confidentiality. More recently, these characteristics

have attracted larger borrowers that have traditionally

accessed other sources of funding. This alternative and

flexible funding source for riskier borrowers involves

a higher cost; as a result, interest rates on private

credit loans tend to exceed yields for market-based

alternatives (Figure 2.3, panel 1).

Characteristics and Vulnerabilities of Private

Credit Borrowers

Tracking the financial characteristics of private

credit borrowers is challenging because of their

private nature, resulting in limited availability of

their financial statements. To address this challenge,

a sample of private credit borrowers was constructed

by cross-referencing data from Preqin with corporate

fundamentals sourced from S&P Capital IQ.

Private credit borrowers are typically highly lev-

eraged middle-market companies. These firms are

Private credit

Median firm size: $0.5 billion

Leveraged loans

Median firm size: $4.6 billion

High-yield bonds

Median firm size: $4.5 billion

Investment-grade bonds

Median firm size: $16 billion

Information

technology,

41%

Healthcare,

14.5%

Consumer

discretionary,

11.5%

Industrials,

8.5%

Raw materials

and natural

resources,

8.2%

Telecoms

and media,

6.1%

Financial and

insurance services,

5.8%

Other,

4.5%

Figure 2.3. Private Credit Firms Are Medium Sized, Technology Sector Heavy, and Relatively Highly Leveraged Compared to

Earnings

1. US Corporate Debt Yields and

Median Private Credit Loan Rates

(Percent)

The interest rates on private credit loans are

typically higher than the yields on

market-based debt instruments.

Corporate bonds Leveraged

loans

private

credit

IG HY BDCs

0

2

4

6

8

10

12

14

Debt-to-assets ratio, percent

2. Size and Leverage Statistics, by Issuer Type

(North America)

(Median debt-to-asset ratio in percent; median

debt-to-EBITDA ratio; bubble size reflects median

firm size by total assets)

Private credit borrowers are smaller than the typical

leveraged loan or bond issuer, and they are more

highly leveraged as compared to their earnings.

2.0

2.5

3.0

3.5

4.0

4.5

5.0

30 40 50

Debt-to-EBITDA ratio

A breakdown of private credit borrowers

by sector shows a greater weight of

technology and health care sectors.

3. Private Credit Sector Allocation, by

Last Three-Year Deal Volume

(Percent share by global deal volume)

Sources: Bloomberg Finance L.P.; Preqin; S&P Capital IQ; and IM

F staff calculations.

Note: In panel 1, bond yields are based on the aggregate Barcla

ys Bloomberg US corporate bond indices. Leveraged loan yields originate from the LSTA US

Leveraged Loan Index. Private credit loan interest rates are ba

sed on BDC filings and reflect the median among a sample of loans. The bond and leveraged loan

yields reflect the marginal cost of funding, whereas private cre

dit loan interest rates reflect the BDC portfolio. The reference

date is year-end 2023. In panel 2, private

credit firm fundamentals are based on a sample of private credit

transactions from Preqin that have matching data in Capital IQ Pro. This matched sample may

therefore be subject to a selection bias given that most privat

e firms do not publicly release financial statements. BDCs = business development companies;

EBITDA = earnings

before interest, tax, depreciation, and amortization; HY = high yield; IG = investment grade.

CHAPTER 2 THE RISE AND RISKS OF PRIVATE CREDIT

59International Monetary Fund | April 2024

significantly smaller than broadly syndicated loan or

high-yield bond-issuing firms. Private credit borrowers

have higher debt-to-earnings ratios but better asset

coverage than their syndicated loan counterparts.

(Figure 2.3, panel 2) For all these asset classes, high

debt levels are often driven by private equity sponsors

that enhance returns for their investors by increasing

debt on the balance sheets of the firms they acquire

(Haque 2023). Private credit borrowers operate across

various economic sectors and are overrepresented in

the information technology and health care sectors

(Figure 2.3, panel 3).

5

Private credit borrowers are vulnerable to interest

rate shocks. Private credit borrowers almost exclu-

5

For comparison, the weights of the technology and health

care sectors in the S&P 500 Index are 30 percent and 12 percent,

respectively, whereas these shares are 24 percent and 11 percent for

the Bloomberg World Large and Mid Cap Index.

sively use floating rate loans. By contrast, only about

29 percent of high-yield corporate bond issuers’ total

debt is variable rate.

6

Panel 1 of Figure 2.4 highlights

the swifter transmission of interest rates to the

cost of debt for firms with a higher share of vari-

able rate debt.

Rising interest rates could ultimately lead

to a deterioration in credit quality. The rise in

benchmark rates has increased the interest burden

for private credit borrowers, prompting some

firms to resort to payment-in-kind interest. This

flexibility may help borrowers withstand temporary

stress, but it can lead to compounding losses if

a firm’s underperformance cannot be reversed.

6

For a sample of 518 North American and 157 European

high-yield corporate bond issuers, the average share of variable rate

debt is 29.4 percent, at the end of 2022. Sources: S&P Capital IQ;

and IMF staff calculations.

Private credit

Variable rate debt

75%–100% of total debt

Variable rate debt

50%–75% of total debt

Variable rate debt

25%–50% of total debt

Variable rate debt

0%–25% of total debt

PIK share

2018 interest income = 1

Non-PIK (right scale)

PIK (right scale)

Interest coverage ratio (left scale)

Share of firms with ICR < 1 (right scale)

3

12

6

9

2018

0

40

5

10

15

20

25

30

35

0

3.5

0.5

1

1.5

2

2.5

3

1. Cost of Debt by Firm Reliance on

Variable Rate Instruments

(Percent of total debt)

2. BDC Interest Income and PIK Share

(Percent, left scale; total interest income

indexed to 2018 = 1, right scale)

3. ICR and Share of Firms with ICR < 1

(Percent, left scale; percent, right scale)

The transmission of higher rates into firms’

cost of debt has been more swift for firms

with variable rate debt.

Payment-in-kind interest payments have

surged for BDC portfolios.

Public firms with size and leverage characteristics

similar to private credit firm have shown a

deterioration in their ability to pay interest.

Sources: BDC 10-K and 10-Q filings; S&P Capital IQ; and IMF staf

f calculations.

Note: Panel 1 shows the cost of debt, calculated as interest ex

pense divided by total debt. Medians are taken for each bucket of variable rate debt reliance, whereby

this reliance is expressed as the ratio of variable rate debt o

ver total debt. The cost of debt within each bucket varies based on credit fundamentals. Private credit

rates are based on a sample of BDC portfolios. In panel 2, when

interest is paid in kind, no cash flow occurs. Instead, the interest coupon is added—usually at an

extra cost—to the loan’s principal. Statistics in panel 3 are b

ased on a sample of public firms located in North America with size and leverage characteristics similar

to

those of borrowers in the private credit universe. It should be noted that interest coverage and debt/EBITDA ratios are usually not reflected in firm-level databases

when

earnings are negative. This means that the true number of firms with unsustainable interest expense level is (even) higher than indicated by the ICR = 1

threshold. BDC = business development company; EBITDA = earning

s before interest, taxes, depreciation, and amortization; ICR = interest coverage ratio;

PIK = payment in kind.

0

14

2

4

6

8

10

12

0

14

2

4

6

8

10

12

2019 20 21 22 23

19 20 21 22 23

Figure 2.4. Private Credit Firms Face a Steep Increase in the Cost of Their Variable Rate Debt

2019:Q4

20:Q1

20:Q2

20:Q3

20:Q4

21:Q1

21:Q2

21:Q3

21:Q4

22:Q1

22:Q2

22:Q3

22:Q4

23:Q1

23:Q2

23:Q3

GLOBAL FINANCIAL STABILITY REPORT: THE LAST MILE: FINANCIAL VULNERABILITIES AND RISKS

60 International Monetary Fund | April 2024

The share of payment-in-kind interest in BDC

interest income has doubled since 2019 (Figure 2.4,

panel 2). In addition, the proportion of firms with

unsustainable interest coverage ratios has increased

to over one-third among firms with size and leverage

characteristics similar to those of private credit

borrowers (Figure 2.4, panel 3).

Mitigating Factors of Credit Risk

Despite the risky profile of private credit borrowers,

their credit losses have not historically exceeded losses

in high-yield bonds and are comparable to leveraged

loans (Figure 2.5, panel 1). Headline default rates for

private credit indices tend to be relatively high, but

these include covenant defaults, which often lead to

renegotiated terms rather than a true payment default.

Sponsorship by private equity firms also mitigates

private credit risks. Private equity sponsors want to

preserve the long-term value of their investments and

may inject additional capital in their portfolio firms

if they believe that stress will be transient. Evidence

from the leveraged-loan market illustrates that firms

sponsored by private equity have lower default rates

during periods of stress than other firms (Figure 2.5,

panel 2). This strategy may lessen defaults in a

short-lived downturn. To help boost recovery rates

in case of liquidation, most private credit loans are

secured, which mitigates credit losses. Collateralization

can be lower in some sectors, such as the software

industry, where unitranche and mezzanine loans are

more common (Figure 2.5, panel 3).

Private Credit Cyclicality

Evidence is mixed regarding the cyclicality of

private credit lending. Private credit managers argue

that private credit remains accessible during economic

downturns, whereas traditional funding sources often

contract. There is evidence suggesting that private

credit’s relationship with private equity sponsors facil-

itated lending during the COVID-19 pandemic (Jang

2024). In March 2020, private credit lending did not

“dry up,” while high-yield bond and leveraged-loan

issuance contracted strongly (Figure 2.6, panel 1).

Private credit lending subsequently proved more stable

than similarly floating rate leveraged loans. A structural

analysis shows private credit market activity is less

Sponsored

leveraged loans

Nonsponsored

leveraged loans

Software

IT infrastructure

Health care

Industrial machinery

All

Figure 2.5. Private-Equity-Sponsored Firms Show Lower Default Rates during Times of Stress, and Overall Credit Losses in

Private Credit Have Historically Not Been Outsized because of Risk Mitigants

1. Average Annual Credit Losses

(Percent)

Private debt credit losses fall below high-yield

bond and bank loan credit losses.

0

1.6

0.2

0.4

0.6

0.8

1.0

1.2

1.4

High-yield

bonds

Leveraged

loans

Private

credit

Bank

loans

Private-equity-sponsored leveraged loans

have shown significantly lower default rates

during periods of stress compared with

nonsponsored firms.

2. Annual Loan Default Rates

(Percent)

0

16

2

4

6

8

10

12

14

Other years

(baseline)

2009 2020 2023

In some sectors and industries, secured loans

are less common. This is likely related to the

amount of available collateral.

3. Loan Types in Private Credit, by Sector

(Percent of deals)

0

70

10

20

30

40

50

60

Secured Mezzanine Unitranche Other

Sources: Cliffwater; Federal Reserve; Fitch Ratings; Preqin; and IMF staff calculations.

Note: In panel 1, “bank loans” refers to US banks’ commercial and industrial business loans. Average annual credit losses are c

omputed for a 10-year window

between 2013 and 2022. In panel 2, “other years” refers to the 2007–22 period, with the exception of 2009 and 2020. IT = inform

ation technology.

CHAPTER 2 THE RISE AND RISKS OF PRIVATE CREDIT

61International Monetary Fund | April 2024

responsive to a sudden credit shock than the high-yield

bond and leveraged-loan markets (Figure 2.6, panel 2).

Yet there is also evidence of procyclical behavior.

The Bank for International Settlements found that

capital deployment in private equity and private credit

is positively correlated with stock market returns

(Aramonte and Avalos 2021). In addition, data from

the BDC markets indicate that new private credit loans

contract when banks tighten their lending standards

(Figure 2.6, panel 3). New lending by private credit

funds seems to be less procyclical than BDC lending.

Liquidity Risks of Private Credit Funds

Although private credit funds hold highly illiquid

underlying assets, their structure is designed to

minimize liquidity and maturity transformation risk

through long-term lockups and other constraints

for investors to redeem their capital. Most private

credit fund investors, such as insurance companies

and pension funds, lock in a certain portion of their

investments for a period compatible with the life cycle

of closed-end funds. However, liquidity stress could

arise from the credit facilities offered by private credit

funds to borrowers. In addition, the recent shift toward

semiliquid evergreen structures could increase liquidity

risks over time.

Limited Redemptions

Private credit funds invest primarily in private

corporate loans, assets characterized by their

illiquidity, and an incipient secondary market. Asset

managers mitigate the risk of holding these assets by

setting structures with low maturity transformation.

Private credit CLOs and closed-end funds do not

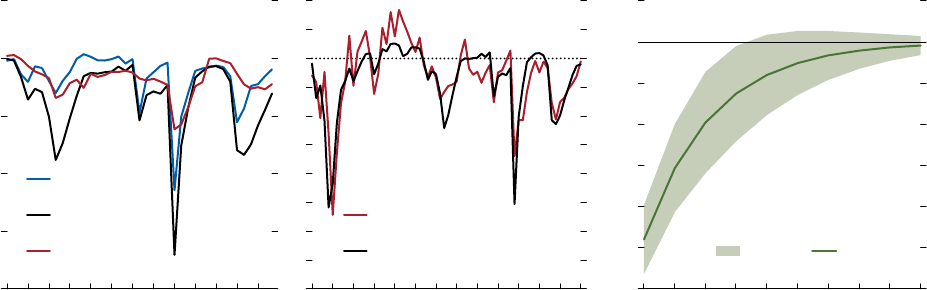

High-yield bonds

Leveraged loans

Private credit

95% CI

Point estimate

COVID-19

BDC lending Private credit

fund lending

Private credit

fund

fundraising

1. Case Study: Gross US Issuance

during the Pandemic

(Percent; cumulative deviation from

long term average)

New private credit lending did not show

the same drop as high-yield bond and

leveraged-loan issuance in March 2020,

and also remained more stable in

subsequent months.

2. Response of US Issuance to a Credit Risk

Shock

(Percent; deviation from baseline gross quarterly

issuance volume)

New BDC lending seems to be more correlated

with bank lending conditions than private

credit, where fundraising in particular shows a

weaker relationship to bank lending conditions.

The response of new private credit deals and

fundraising to a credit shock is not as consistently

negative as the response of leveraged-loan and

high-yield bond issuance.

3. US Private Credit: New Lending,

Fundraising, and Bank Lending Conditions

(Percent; median new lending and fundraising

as share of outstanding)

Sources: Bloomberg Finance L.P.; Federal Reserve; PitchBook LCD; Preqin; S&P Capital IQ; and IMF staff calculations.

Note: In panel 1, issuance is benchmarked versus the average cu

mulative issuance over the same months in the five preceding years. In panel 2, the response of

issuance volumes is based on Structural Vector Autoregression models containing quarterly high-yield corporate bond spreads and

issuance volumes, whereby the

identification is based on the Cholesky ordering spreads (first)

and issuance (second). The number of lags included is based on the Akaike information criterion. One

lag is included for leveraged loan, high-yield bond issuance and private credit deal volume, two for fundraising. In panels 3 a

nd 4, bank lending conditions are based

on the Net Percent of Domestic Respondents Tightening Standards

for Commercial & Industrial Loans for Large/Medium Firms, as r

eported in the Senior Loan Officer

Opinion Survey on Bank Lending Practices. BDC = business develo

pment company; CI = confidence interval.

Private credit Leveraged

loans

High-yield

bonds

Deals Fundraising

–100

–80

–60

–40

–20

0

20

40

60

80

100

–30

–20

–10

0

10

0

1 2

3

4

5 6

7

8 9 10

0

5

10

15

20

<0 0–40 40–80 <0 0–40 40–80 <0 0–40 40–80

Figure 2.6. Private Credit and Procyclicality

Months since coronavirus outbreak

(1 = March 2020)

Net % of domestic respondents

tightening standards

GLOBAL FINANCIAL STABILITY REPORT: THE LAST MILE: FINANCIAL VULNERABILITIES AND RISKS

62 International Monetary Fund | April 2024

typically allow redemptions during their life span.

This significantly reduces the liquidity risks arising

from such funds.

Redemptions are more common for semiliquid

structures that aim to provide liquidity to investors

while investing in illiquid assets. Unlike traditional

closed-end funds, semiliquid funds provide investors

with limited windows during which they can redeem

their shares. BDCs, for instance, often use semiliquid

structures to appeal to a wider investor base, especially

individual investors. Even in semiliquid structures,

however, redemptions are often constrained by gates,

fixed redemption periods, and suspension clauses.

Although these liquidity management tools may seem

adequate in principle, they have not been tested in a

severe runoff scenario, and redemption pressures have

sometimes forced certain large private credit fund

managers to allow redemptions above the established

limits. In addition, certain funds, particularly in

Europe, have adopted more frequent redemption

periods (for instance, monthly or even more often),

which may exacerbate liquidity risks.

Potential liquidity pressures could also arise from

credit and liquidity facilities offered to portfolio

companies. Private credit funds often combine loans

with revolving facilities. There is a risk that, like the

“dash for cash” in 2020, firms simultaneously and

unexpectedly withdraw their credit balances, sud-

denly increasing private credit funds’ need for cash.

Private credit funds might also transfer the liquid-

ity stress to end investors through their committed

capital (see the “Interconnectedness” section later in

this chapter).

Risks from the Increasing Share of Retail Investors and

Semiliquid Funds

The recent trend toward the use of semiliquid

structures has the potential to increase maturity

transformation within the private credit industry.

This trend is exemplified by the active creation of

semiliquid funds, such as perpetual nontraded BDCs

(Figure 2.7). One primary motivation behind this

trend is to access a broader investor pool, particularly

individual investors. As institutional investors

reach their limits on investment in private capital,

funds seek to broaden their capital sources. Recent

legislation in Europe on the European long-term

investment funds (ELTIFs) and in the United

Kingdom on the long-term asset funds (LTAFs) may

further support this trend.

Although designed to enable access for individual

investors, the operational efficiencies and liquidity

potential of semiliquid structures may also appeal

to institutional investors. Insurance companies and

pension funds have transformed their business models

over the years, prompted by the prolonged low

interest rate environment. They have shifted from

traditional, capital-intensive, long-term guaranteed

products to unit-linked insurance products

7

and

from defined-benefit to defined-contribution pension

plans. By transferring the performance and loss of

investments to end investors (that is, clients), insurers

and pension funds enable clients to switch between

available investment plans. This flexibility reduces

the effective duration of the liabilities of insurers and

pension funds, potentially increasing their demand

for liquidity in underlying investments and further

7

Unit-linked insurance products provide both insurance coverage

and investment exposures—typically through investment funds—and

the insurance benefits are linked to the investment returns. Policy-

holders are often subject to a minimum lock-in period, additional

fees, and taxes for early surrender, which discourage the policyhold-

ers from early surrender and redemption. Despite these constraints,

insurers often allow policyholders to change their investment alloca-

tions among the selected investment funds.

Private BDC

Traded BDC

Perpetual BDC

Figure 2.7. Private Credit Liquidity

An increase in semiliquid products, such as perpetual business

development companies, can increase liquidity risk.

BDCs Assets under Management

(Billions of US dollars)

0

300

50

100

150

200

250

2000 02 04 06 08

10 12 14 16 18 20 22

Sources: S&P Capital IQ; and IMF staff calculations.

Note: The data comes from the aggregation of 143 business development

companies, 50 of them being traded. BDCs = business development companies.

CHAPTER 2 THE RISE AND RISKS OF PRIVATE CREDIT

63International Monetary Fund | April 2024

pushing the trend toward semiliquid structures in

private credit.

Leverage in Private Credit

Leverage deployed by private credit funds appears

to be low compared with other lenders such as banks,

but the presence of multiple layers of hidden lever-

age within the broader private credit system raises

concerns. Leverage may not always be at the fund

level, and the entire private credit system can form a

complex network involving several potentially lever-

aged participants, including borrowers. Assessing the

financial stability implications of these multiple layers

of leverage is challenging because of data limitations.

Multiple Layers of Leverage

Private credit investors, funds, and borrowers deploy

leverage extensively, forming a complex multilayered

structure. Investors such as insurance firms and pension

funds may use leverage (Figure 2.8, channel 1), making

them vulnerable to the deterioration of the credit out-

look and an increase in credit downgrades and defaults.

These investors are also subject to margin and collateral

calls during periods of high market volatility, which,

given their large footprint, may exacerbate stress in

financial markets (see the “Interconnectedness” section).

Private credit investment vehicles may employ lever-

age directly within a fund, through special-purpose

vehicles or holding companies (Figure 2.8, channel 2).

Leverage can also be increased through more complex

strategies such as collateralized fund obligations, in

which the interests of the fund’s limited partners are

transferred to a special-purpose vehicle to loosen cash

flows and access a wider investor base (IOSCO 2023).

These opaque structures can also include cross-border

entities, which are often used for regulatory and

tax purposes.

In addition, private credit borrowers extensively

deploy leverage (Figure 2.8, channel 3). As discussed

earlier in the “Mitigating Factors of Credit Risk”

section, most firms borrowing from private credit

funds are backed by private equity sponsors, leading

to higher debt for the firms or leverage ratios deemed

excessive by banks.

These multiple layers of leverage throughout the value

chain, often hidden by gaps in reporting, could magnify

losses and trigger spillovers to other markets during

a downside scenario of forced deleveraging. In such

scenarios, vulnerabilities among borrowers may lead to

large, unexpected losses for funds and end investors.

Even funds that deploy modest amounts of leverage may

still face significant capital calls, potentially affecting

their leverage providers. This situation could compel

the entire network to simultaneously reduce exposures,

spilling over to other markets and the broader economy.

Evaluation of leverage in private credit markets from a

network perspective by prudential authorities is therefore

critical but is currently impeded by data constraints.

Leverage of Private Credit Funds

Private credit funds deploy leverage to enhance

returns for equity investors. The specific debt structure

varies by type of investment vehicle (Table 2.2). As for

most nontraded private credit products, information

on the deployment of leverage by closed-end funds is

scarce. One of the few in-depth studies of closed-end

funds was recently conducted by the US Federal

Reserve using confidential regulatory data.

According to this study, most closed-end private

credit funds are unleveraged but some use financial

and synthetic leverage (Federal Reserve 2023). Those

funds at the 95th percentile have borrowing-to-assets

ratios of about 1.27 and derivatives-to-assets ratios

of about 0.66.

Equity or credit

investment

Leverage

1

3

2

Figure 2.8. Leverage in Private Credit

Investors, funds, and borrowers extensively deploy leverage, forming a

complex multilayers structure.

Multiple Layers of Leverage

Sources: IOSCO 2023; and IMF staff.

Note: SPV = special purpose vehicle.

Investors

(pension funds, insurance

companies…)

Leverage Providers

(banks, syndicates, hedge

funds…)

Private Credit Fund

Fund-Owned SPV

Portfolio Companies

GLOBAL FINANCIAL STABILITY REPORT: THE LAST MILE: FINANCIAL VULNERABILITIES AND RISKS

64 International Monetary Fund | April 2024

Sources of debt for BDCs seem more diversified,

as they issue unsecured bonds and notes (Figure 2.9,

panel 1). BDCs are subject to a regulatory limit on

leverage and often establish internal limits that are

more conservative than the regulatory ones.

8

Neverthe-

less, BDCs’ leverage has steadily increased over the past

20 years (Figure 2.9, panel 2). Anecdotal evidence sug-

gests that closed-end funds exhibit the same behavior.

Private credit CLOs use securitization structures that

enable investors to acquire different tranches based

on their risk appetite.

9

Insurance companies, pension

funds, hedge funds, and banks are the main investors

in CLO securities. The ratio of CLO non-equity

tranches over the equity tranches varies but is often

about 6 to 1.

Although leverage at the fund level appears limited,

private credit funds may still be subject to rollover

risks, particularly in a sharp downturn. Leverage

provided by commercial banks often has loan-to-value

triggers, and thus, private credit funds may face large

collateral calls on leveraged portfolios during times of

stress. Leverage providers may decide to mark assets

down significantly, given the riskiness of borrowers and

the lack of comparable public pricing data. In addi-

tion, private credit funds often provide their borrowing

firms with revolvers or other credit lines. Sudden and

significant correlated drawdowns of these credit lines

8

The regulation of BDCs caps their debt-to-equity ratio at 2,

which was increased from 1 in 2018. Under the framework for loan

origination funds in the European Union, leverage caps may apply to

private credit fund managers irrespective of whether the underlying

investors are retail.

9

Private credit CLOs are structured finance vehicles that pool a

portfolio of privately originated loans and securitize them into debt

securities. They differ from traditional middle-market CLOs that

include underlying loans not originated in private markets.

could create considerable funding needs for the private

credit funds. Anecdotal evidence suggests that private

credit funds maintain significant cushions to mitigate

this risk, yet industry commentary suggests that such

pressures were seen during the height of COVID-19

stress in 2020. Unlike banks, private credit providers

did not have access to central bank lending facilities,

nor were central banks able to buy private credit assets

to support asset prices (see the April 2023 Global

Financial Stability Report). Evaluating the potential

extent of these risks is challenging given the lack of

publicly available information on maturity profiles and

often even on the composition and amount of debt.

Private Credit Valuations

Private credit loans tend to suffer from stale

valuations because of the absence of secondary

markets, limited comparable transactions, and irregular

appraisals. In a downside scenario, stale valuations

could create a first-mover advantage and increase

the risk of runs for private credit funds. This risk,

however, can be significantly mitigated by restrictions

on investors redeeming their investments (see the

“Limited Redemptions” section earlier in the chapter).

The lack of information about vulnerable borrowers,

as discussed in the previous section, combined with

stale valuations, nevertheless makes it challenging for

outsiders to assess potential losses promptly and could

fuel a loss of confidence in the segment.

Valuation Practices and Requirements

Valuing private credit assets is inherently challenging

because of their illiquid nature. Private credit loans

Table 2.2. Characteristics of Leverage in Private Credit Vehicles

Private credit investment vehicles deploy leverage in different forms.

Closed-End Funds BDCs Middle-Market CLOs

Debt-to-equity ratios ~0 to 1.3× ~0.8 to 1.2× All debt-to-equity: ~6×

AAA to other classes: ~1×

Leverage sources Portfolio financing, NAV loans,

subscription lines, derivatives

Secured bank lines of credit and

secured/unsecured bonds

Term leverage through structured

notes

Rollover risk Yes Yes No

Collateral call frequency Varies (typically quarterly) Varies (typically quarterly) None (cash-flow structure)

Main lenders Banks, insurers, pension funds Banks, insurers, pension funds Insurers, pension funds, hedge

funds, banks

Total AUM (United States) ~$1.2 trillion ~$300 billion ~$100 billion

Sources: IOSCO 2023; and IMF staff.

Note: AUM = assets under management; BDCs = business development companies; CLOs = collateralized loan obligations; NAV = net asset value.

CHAPTER 2 THE RISE AND RISKS OF PRIVATE CREDIT

65International Monetary Fund | April 2024

can be tailored to the financing needs of borrowers

and lenders, making it difficult to identify comparable

transactions. In the absence of observable price inputs,

the firms must resort to mark-to-model approaches to

estimate market prices that are inherently subjective

and can increase the potential for managerial manip-

ulation (Ball 2006; Dudycz and Praźników 2020). To

address these concerns and mitigate risks, asset manag-

ers frequently seek third-party pricing services.

10

Private credit fund managers must adhere to

accounting principles outlined in relevant standards,

such as generally accepted accounting principles in

North America or the International Financial Report-

ing Standards. These accounting standards offer guid-

ance but do not mandate any specific technique for

asset valuation, granting managers significant discre-

tion. The current regulatory framework, similarly, does

not specify asset valuation methodologies, focusing on

policy documentation, governance frameworks, and

investor disclosures. Evidence from disclosure forms of

traded private credit funds suggests that markdowns

often result from impairments of a borrower’s finan-

cial position.

10

Third-party valuation may not fully address the risks, as

evidence suggests that profit-driven service providers, appointed

and compensated by clients, may prioritize client retention over

impartiality (Efing and Hau 2015; Short and Toffel 2016).

Private Credit Stale Valuations

To assess private credit valuation practices, the

analysis conducted for this chapter benchmarked them

against the prices of similar publicly traded assets,

focusing on BDCs. BDCs are specific investment

funds created in the United States to encourage

the flow of capital to smaller companies. BDCs’

granular reporting of their investment portfolios—

consisting of loans, common and preferred equity

investments, various tranches of CLOs, and

asset-backed securities—along with the quarterly

position-by-position accounting fair-value marks,

provides a valuable window into the normally opaque

world of private credit.

11

11

Most BDCs have portfolios concentrated in first- and

second-lien senior secured loans, which typically represent

70 to 90 percent of their investment portfolios. These loans

are distributed across multiple industries and borrowers, often

ranging from 100 to 200. In addition to private credit loans, BDC

portfolios often contain equities and bonds of varying liquidity.

To focus on credit valuations, the analysis excludes price changes

arising from other types of assets. The US Securities and Exchange

Commission requires all BDCs to disclose Forms 10-Q and 10-K.

Public BDCs provide additional transparency, as they cater to a

broad range of equity and bond investors. The disclosure reports of

BDCs are prepared in accordance with the US generally accepted

accounting principles, following accounting and reporting guidance

ASC 946, and fair value of level 3 assets is determined in line

with ASC 820–10.

MedianInterquartile range

Unsecured bonds and notes

Revolving credit (secured bank credit)

Secured bonds and notes

Other

11

10

9

13

13

9

7

47

50

51

39

41

49

33

39

37

30

43

38

34

5

5

4

5

5

12

11

51

Figure 2.9. Leverage of Business Development Companies

BDCs have a relatively diversified source of financial leverage t

hat

includes secured and unsecured bonds and notes.

1. BDCs’ Source of Leverage

(Percent)

0

100

10

20

30

40

50

60

70

80

90

2004:Q4

23:Q4

22:Q4

21:Q4

20:Q4

19:Q4

19:Q1

17:Q4

16:Q4

15:Q4

14:Q4

13:Q4

13:Q1

11:Q4

10:Q4

09:Q4

08:Q4

07:Q4

06:Q4

05:Q4

The debt-to-equity ratio of BDCs has increased steadily, although still

substantially below the regulatory cap of 2.

2. Median BDC Leverage

(Debt-to-equity ratio)

0

1.6

0.2

0.4

0.6

0.8

1.0

1.2

1.4

2322212019182017

Sources: S&P Capital IQ; and IMF staff calculations.

Note: BDCs = business development companies.

GLOBAL FINANCIAL STABILITY REPORT: THE LAST MILE: FINANCIAL VULNERABILITIES AND RISKS

66 International Monetary Fund | April 2024

The analysis shows that private credit prices move

less than in high-yield and leveraged-loan markets,

even though private credit borrowers are riskier. In

Figure 2.10, panel 1 shows that the reaction of BDC

loans to credit shocks is much smaller than that of

B-rated leveraged loans, despite the lower credit qual-

ity of BDCs’ loan portfolios. The smaller valuation

adjustment is offset by an additional discount applied

to market prices of BDC shares (Figure 2.10, panel 2).

The discount widens during stress periods, and the

widening is proxied by the general market repricing of

credit risk (proxied by the LSTA US Leveraged Loan

100 Index).

Evidence suggests that adjustments to the values of

private credit loans are smaller and slower than those

observed in public markets. Panel 3 of Figure 2.10

shows that such deviations tend to persist for several

quarters, after which share prices and net asset value

per share converge. Markets differentiate BDCs on the

basis of their qualitative and quantitative characteris-

tics, such as the sector to which each BDC is exposed,

its ability to grow organically, and its transparency.

For other nontraded private credit investment funds,

evidence suggests that the discounts are even larger

because of the lack of transparency.

Potential Risks and Benefits from Infrequent Valuations

Stale valuations could offer a first-mover advantage

and increase runoff risks for private credit funds, but

this risk appears significantly mitigated at present. In

a downside scenario, stale valuations might overvalue

a fund’s assets, potentially prompting investors

to exit before asset values are marked down. As

outlined in the “Vulnerabilities to Liquidity Stress

and Spillovers to Public Markets” section, however,

private credit funds impose substantial obstacles for

investors seeking to redeem their investments, thus

mitigating this risk.

Industry commentary suggests that in illiquid asset

classes such as private credit, valuations are inherently

uncertain and subjective, potentially diminishing

the advantages of more frequent mark-to-market

practices. Beyond the associated costs and risk of

mispricing, frequent mark-to-market assessments

could exacerbate procyclical tendencies and increase

LL market price:

BB rated

LL market price:

B rated

BDC: accounting

price of loans

BDCs: weighted-average

price-to-NAV

Explained by the index of market

prices of leveraged loans

Price/NAV95% Cl

Figure 2.10. Valuation of Private Credit Assets

Adjustment of the valuation of private credit

loans is insufficient during market shocks ...

1. Accounting Fair Value of BDCs’

First-Lien Loans

(Percent)

80

105

85

90

95

100

2014:Q1

14:Q4

15:Q3

16:Q2

17:Q1

17:Q4

17:Q3

19:Q2

20:Q1

20:Q4

21:Q3

22:Q2

23:Q1

... which is offset by the additional discount

of market price to NAV.

2. Public BDCs: Price/NAV

(Ratio)

0.2

1.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1.1

Dec. 2007

Mar. 09

Jun. 10

Sep. 11

Dec. 12

Mar. 14

Jun. 15

Sep. 16

Dec. 17

Mar. 19

Jun. 20

Sep. 21

Dec. 22

Mar. 24

Price and NAV take at least four quarters to

converge after an unexpected shock.

3. Convergence after an Unexpected

Downward Shock to the Price-to-NAV Ratio

(Percent)

–12

2

–10

–8

–6

–4

–2

0

1 2 3 4 5 6 7 8 9 10

Sources: 10-Q/10-K disclosures of BDCs; Bloomberg Finance L.P

.; S&P Capital IQ; and IMF staff calculations.

Note: Panel 3 shows the impulse response function to a sudden d

eviation of the price-to-NAV ratio. The impulse response function is based on an AR(1) model using

quarterly data. The panel shows that—based on the historical pr

ice-to-NAV ratio patterns—it takes at least four quarters for the price and the NAV to converge after

a shock. The shock is sized to one standard deviation. BDC = bu

siness development company; CI = confidence interval; LL = leveraged loan; NAV = net asset value.

CHAPTER 2 THE RISE AND RISKS OF PRIVATE CREDIT

67International Monetary Fund | April 2024

market volatility. Moreover, the emphasis on frequent

valuations might incentivize investors and managers

to prioritize short-term performance, undermining

the long-term advantage offered by the buy-and-hold

nature of private credit. Institutional investors are

also incentivized to avoid balance sheet volatility and

demand more frequent and rigorous valuations from

investment managers.

However, stale valuations could also distort

capital allocation, exacerbate conflicts of interest,

and undermine confidence in private credit markets.

Inaccurate or infrequent mark-to-market practices

hinder investors from making informed decisions

and managing risks effectively. Stale valuations could

also affect market integrity when incentives are not

aligned. For example, managers may have incentives

to maintain high valuations during fundraising

periods to reference historically higher returns.

Conflicts of interest also arise from managers’ fees

based on valuation. Stale valuations make it difficult

for stakeholders to assess potential losses in a timely

manner and, in a downturn scenario, could fuel a loss

of confidence in the segment.

Interconnectedness

Private credit funds have ties with various financial

institutions. These institutions include private equity

firms, which sponsor most private credit deals; banks,

which are the primary providers of leverage; and insti-

tutional investors, which invest capital in the form of

equity and debt investments in private credit funds.

Interconnections between Private Credit and Private

Equity Firms

The private credit and private equity industries are

closely intertwined through two primary channels.

First, many managers of private credit funds are

also managers of private equity funds (Figure 2.11,

panel 1). This interconnectedness becomes even more

pronounced when considering the size of private

credit funds, given that managers of the largest

private credit funds are more likely to be involved in

the private equity segment. Second, private credit is

a key funding source for firms sponsored by private

equity (Figure 2.11, panel 2), with a large share of

High-yield bonds

Institutional leveraged loans

Direct lending (estimate)

Sponsored Nonsponsored

81.2%

42.3%

13.8%

43.9%

42.3%

77%

72%

51%

23%

28%

49%

Figure 2.11. Links between Private Credit and Private Equity

Many firms that manage private credit funds

also manages private equity funds.

1. Share of Private Credit Funds Managed

by Firms that Also Manage Private

Equity Funds

(Percent)

0

10

20

30

40

50

60

70

80

90

100

Weighted by private

credit assets under

management

Weighted by number

of private credit funds

under management

Private-equity-backed firms borrow on the

leveraged-loan, high-yield bond, and private

credit markets.

2. New Issue Volume for US Private-Equity-

Backed Borrowers, 2023

(Percent)

About 70 percent of private credit deals are

sponsored by private equity firms.

3. Share of Sponsored and Nonsponsored

Private Credit Deals, 2021–23

(Percent)

Europe North

America

Other

regions

0

10

20

30

40

50

60

70

80

90

100

Sources: PitchBook LCD; Preqin; and IMF staff calculations.

GLOBAL FINANCIAL STABILITY REPORT: THE LAST MILE: FINANCIAL VULNERABILITIES AND RISKS

68 International Monetary Fund | April 2024

the borrowing firms in private credit deals having a

private equity sponsor (Figure 2.11, panel 3). This is

an important connection because, as discussed in the

“Characteristics of Private Credit Borrowers” section,

private equity sponsors greatly mitigate credit risk.

Overall, these connections suggest that vulnerabilities

in one segment of the private financing industry

could spill over to the other. Close ties between the

two industries also raise questions about possible

conflicts of interest, given that managers may have

multiple connections through portfolio firms and

investors (that is, limited partners).

Exposure of Traditional Financial Institutions to

Private Credit

Potential risks to financial stability arising from direct

exposures of banks to private credit currently appear to

be contained. Banks are one of the primary providers

of leverage to private credit firms, yet their aggregate

exposure remains low. In aggregate, private credit funds

in the United States borrowed about $200 billion from

US banks at the end of 2021, representing less than

1 percent of the banks’ assets (Federal Reserve 2023).

Credit risks to banks are also mitigated by the secured

nature of the loans. However, the lack of data does not

allow ruling out the possibility that some banks exhibit

concentrated exposure to the sector.

In their search for yield, pension funds and insur-

ance companies have emerged as important end

investors in private credit, with significant investment

growth in recent years (Figure 2.12, panels 1 and 2).

Although private credit exposures are expanding

rapidly, they remain relatively small for most institu-

tions, accounting for only a low single-digit percent-

age of total assets under management (Figure 2.12,

panel 2). Certain segments exhibit substantially higher

exposure. Specifically, some large pension funds and

selected private-equity-influenced insurers in advanced

economies have increased their exposures significantly

in recent years, as investors in not only private credit

funds but also structured credit, participation in direct

lending, and the leverage providers to private credit

investment vehicles.

12

12

For example, such segments have increased their exposure by

investing in collateralized loan obligations and buying bonds and

notes issued by BDCs and other private credit investment vehicles.

19

%

4

%

12

%

30

%

35

%

Unknown

Insurance company

Public pension fund

Other

Private sector pension fund Allocation to private credit funds

(left scale)

Share of assets under management

(right scale)

Figure 2.12. Exposures of Traditional Financial Institutions to Private Credit Funds

Pension funds and insurers are the main investors in private credit

funds globally ...

1. Share of Private Credit Fund Investment

(Percent)

... and they are rapidly increasing their exposure.

2. Investment in Private Credit Funds by Pension Funds and Insurance Firms

(Billions of US dollars, left scale; percent, right scale)

0

4.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

0

700

100

200

300

400

500

600

2016 Current

Sources: Preqin; and IMF staff calculations.

Note: In panel 1, “Unknown” is related to those investors not disclosing the amount of their allocation to private credit funds publicly. This includes pension funds and

insurers that are known to have an allocation to private credit

but do not disclose the exact amount. It also includes other investors, family offices, and sovereign

wealth funds, in particular, that do not disclose data on their holdings. In addition to private credit funds, insurers have substantial exposures to private credit through

their investments in structured credit and their participation in direct lending. The share labeled “Other” includes asset mana

gers investment banks, private equity

firms, endowment plans, and more.

CHAPTER 2 THE RISE AND RISKS OF PRIVATE CREDIT

69International Monetary Fund | April 2024

Vulnerabilities to Liquidity Stress and Spillovers to

Public Markets

Private credit is increasing the share of illiquid

assets held by pension funds and insurers, giving

rise to concerns about potential market disruptions.

Some of the world’s largest pension funds, with assets

exceeding $7 trillion, have significantly increased

their allocation to illiquid investments while actively

using derivatives and other forms of leverage

(Figure 2.13, panels 1 and 2).

13

Rising allocations

to private credit are estimated to account for almost

half of the increase in level 3 assets, reflecting

13

The sample consists of 26 large pension funds—ranked among

the largest 150 pension funds in assets globally—that disclose data

on the gross notional exposure of derivatives in their annual reports.