Cymru

Cymorth

Brynu -

Help

Buy -

Wales

i

to

Help to Buy – Wales

Buyer’s Guide

Phase 3 Extension

www.gov.wales/helptobuy

Your guide to a Help to Buy – Wales: Equity Loan 4

What is a Help to Buy – Wales: Equity Loan? 4

Who provides the loan? 4

Key things you should know before taking out a Help to Buy – Wales: Equity Loan 5

How does it work? 6

Am I eligible? 7

Quality standards 8

Lease restrictions on Help to Buy – Wales homes 9

Estate Management Fees 9

How to apply 10

Buying your new home with an equity loan: 11

– Stage 1: Applying 11

– Stage 2: Authority to Proceed 12

– Stage 3: Mortgage offer and exchange of contracts 13

– Stage 4: Completing the purchase 14

How long does it take to buy a new home with an equity loan? 15

Repaying your equity loan 16

– You may pay back more than you borrow 16

– Work out what you need to repay 16

Understanding your interest payments 17

Contents

Help to Buy – Wales Buyers’ Guide2

Differences in interest payments 18

What happens if the Consumer Price Index (CPI) is below 0%? 18

Equity loan fees and costs 19

Help to Buy – Wales: Equity Loan and mortgages 20

Add and remove homebuyers from the equity loan 20

Structural alterations 21

Other restrictions 21

Changes in the housing market could affect your property price 22

Glossary 24

Updated March 2023

3

Your guide to a Help to Buy – Wales:

Equity Loan

This guide provides useful information

about Help to Buy – Wales: Equity Loan

Phase 3 Extension (from April 2023),

a home ownership scheme. It will help

you to understand what is involved in

taking out an equity loan, how it works

and how to apply.

The principles of the Welsh Government’s

Equity Loan scheme are to provide

support to people who want to become

homeowners, who would not otherwise

have access to an affordable mortgage

or be able to get onto the property ladder.

What is Help to Buy – Wales?

Help to Buy – Wales is an equity loan from

the Welsh Government that you put towards

the cost of buying a newly built home.

Help to Buy – Wales aims to provide

support to people, who would not be able

to get onto the property ladder without the

support of the scheme.

If you’re eligible for an equity loan, you can

borrow up to 20% of the market value of a

new home. The market value is:

• the value of the home, as determined

by an independent organisation called

the Royal Institution of Chartered

Surveyors (RICS), or

• the price a home sells for, whichever

is higher.

When you take out an equity loan, you only

pay interest on the amount you borrowed.

You should be aware that the interest

payments you make do not go towards

repaying your equity loan.

You cannot make monthly repayments to

reduce your loan, but you can choose to

repay it all or in part at any time. If you sell

your home, you will need to repay all of

your equity loan.

You can only apply for Help to Buy – Wales

if you reserve your new home with a Help

to Buy – Wales registered homebuilder.

Who provides the loan?

Help to Buy – Wales: shared equity loan

is provided by Help to Buy – Wales Ltd,

the administering agents appointed by the

Welsh Government.

Help to Buy – Wales Buyers’ Guide

4

Key things you should know before taking

out a Help to Buy – Wales: Equity Loan

Help to Buy – Wales: Equity Loan is not

a discount scheme or a price reduction –

the purchase price of the new home will be

the same whether you buy with or without

an equity loan.

The equity loan is not “interest free” –

Wedonotchargeinterestfortherst

5 years of the equity loan, but you will

begin to pay interest from year 6.

The total equity loan amount you repay

is linked to the value of your home at the

point of repayment, and not the amount

you originally borrowed.

A mortgage is an amount of money you

borrow from a lender to put towards the

full asking price of a property. You normally

borrow it for a set amount of time and pay

back a set amount each month, for an

agreed time. There are 2 main types of

mortgage:

• Interest-only – you only pay interest

based on the amount you owe, and

these payments do not reduce how much

you owe. At the end of your mortgage

term, you will still owe the same amount

you borrowed. If you get a Help to Buy –

Wales: Equity Loan, you cannot have an

interest-only mortgage.

• Repayment – you repay the full amount

(capital) borrowed, plus interest.

The amount you owe will decrease

until you repay it all by the end of your

mortgage term. With Help to Buy –

Wales: Equity Loan, you must have a

repayment mortgage. A mortgage uses

your home as security for the debt, so it

is important you’re able to keep up with

mortgage repayments.

You cannot have an equity loan without a

repayment mortgage, which is valid for the

duration of the equity loan.

5

Updated March 2023

How does it work?

With an equity loan, we lend you a

minimum of 10% and up to 20% of the

market value of your newly built home.

The maximum purchase price for an eligible

property under the scheme is £300,000.

You cannot change or negotiate this price.

Yourhomebuilderwillbeabletoconrm

if the home you want to buy is within the

eligible price range.

You must:

• pay a minimum cash deposit of 5% of

the purchase price of your new home

at exchange of contracts

• arrange a repayment mortgage of at

least 25% of the purchase price of your

new home.

An equity loan is secured against your

property in the same way a repayment

mortgage is. The Help to Buy – Wales:

Equity Loan scheme is not regulated by

the Financial Conduct Authority (FCA).

Example of how much your deposit,

mortgage and equity loan may be if you

buy a new home worth £200,000:

Homebuyers

£10k 5% deposit

£40K 20% equity loan

£150k

75% mortgage from repayment

mortgage lender

For the rst 5 years:

• the equity loan is interest free;

• pay a £1 monthly management fee by

Direct Debit.

From year 6:

• pay the £1 monthly management fee;

• pay a monthly interest fee of 1.75% of

the equity loan;

• interest fees will rise each year in April

by the Consumer Price Index (CPI),

plus 2%;

• continue to pay interest until you repay

your loan in full.

You must repay the equity loan in full

when you pay off your repayment mortgage,

sell your home or reach the end of your

loan term, normally 25 years.

You can repay your equity loan in full

at any time.

Ifmakingapartialrepayment,yourrst

partial repayment will need to be at least

10% of the market value of your home,

at that time.

The remaining balance of the Help to Buy –

Wales shared equity loan, must be at least

5% of the market value.

For example, you could repay 10% if you

took out a 20% loan.

Help to Buy – Wales Buyers’ Guide

6

Am I eligible?

You must be able to fund up to 80% of your

selected property through a combination

of a conventional repayment mortgage,

and a minimum cash deposit of 5% of the

purchase price.

Youmusttakeoutarstchargerepayment

mortgage with a qualifying lender.

www.gov.wales/help-buy-wales-

participating-lenders

When you buy your new build home with

an equity loan, you must be able to afford

the monthly fee and interest payments.

The home you purchase must be your

only home.

You must tell us if you or anyone you

are buying with has a connection with

a homebuilder, as this could affect your

eligibility for the equity loan scheme.

The Help to Buy – Wales scheme was

established to provide support to people

who want to become home owners,

who would not otherwise have access

to an affordable mortgage or be able to

get onto the property ladder. Therefore,

if your nancial position shows you can

secure a 90% rst charge mortgage,

without the support of Help to Buy

Wales, then you will not be offered

Help to Buy – Wales assistance. Your

Independent Financial Advisor will be

able to provide you with further advice.

7

Updated March 2023

We aim to make sure that homes sold with

Help to Buy – Wales are of a high standard

and broadband ready.

All our home builders will clearly

communicate any quality marks they have

been awarded or any quality schemes of

which they are a member, for example

Trustmark, in all Help to Buy – Wales

communications and advertisements.

Members of the Home Builders Federation

(HBF) that participate in the star rating

scheme, must clearly communicate that

rating on all Help to Buy – Wales related

communications and advertisements.

Only developers/builders that have a rating

of 4 stars and above will be permitted to be

part of the Help to Buy – Wales scheme.

Members of the Federation of Master

Builders (FMB) must clearly communicate

their membership on all Help to Buy

– Wales related communications and

advertisements.

Home Builders must:

• have a system in place which ensures

homes offered for sale through Help to

Buy – Wales are checked for quality of

constructionandnishduringthebuild

and on completion;

• be clear in all communications with

customers about likely broadband

capability on developments;

• allow buyers to view the actual home

being purchased (with their own surveyor

if desired) before legal completion of

sale.

Our home builders agree to follow:

1. Consumer Code for Home

Builders

All Help to Buy – Wales registered home

builders follow a code of customer care

and standards set out within the Consumer

Code for Home Builders. Find out more

about the code visit

www.consumercode.co.uk

2. Planning permission and

building regulations

Home builders must ensure each eligible

home built during Phase 3 Extension of

Help to Buy – Wales complies with planning

permissions and the Building Regulations in

force in Wales.

Your conveyancer is responsible for making

sure these are evidenced.

3. New Home Warranty

Your home builders must give you a new

home warranty before you complete the

purchase.

You won’t be able to buy your home without

it. The warranty will:

• dealwithdefectsyoumayndwhenyou

move into your new home

• offer you, us and your mortgage lender

protection.

If you have any questions about the new

home warranty, your conveyancer or home

builders will be able to give you more

information.

Quality standards

Help to Buy – Wales Buyers’ Guide

8

Lease restrictions on Help to Buy – Wales

homes

The Welsh Government has set out rules

to protect you from unfair lease terms and

costs when you buy a home.

There are very few Help to Buy – Wales

homes you can buy that will include a lease.

Ifyouarebuyingaatwithalease,check

with your conveyancer that the terms of the

lease meet the requirements of Help to Buy

– Wales.

If you buy a leasehold property, you own

theleaseholdpropertyforaxedperiod.

A lease is a private legal agreement

between you and the freeholder and sets

out the rights and responsibilities of both

parties. There maybe charges and fees

included in a lease. There are only a limited

number of properties that can be purchased

with the support of Help to Buy – Wales.

Home builders can only charge a

peppercorn ground rent for leasehold

homes included in Phase 3 extension of the

Help to Buy – Wales Scheme.

What is Peppercorn Rent?

The new Leasehold Reform (Ground Rent)

Act 2022 limits the amount of ground rent

payable under most new long leases of

residential properties to a peppercorn.

Peppercorn is effectively a notional rent.

Estate Management Fees

Your builder must provide information,

in writing, about the existence, and likely

level of estate charges, before accepting

a deposit on your home.

Your conveyancer will ensure you have

been advised of any fees that may become

due and the likely action that could be taken

if you do not pay these fees.

9

Updated March 2023

How to apply

1. Find and reserve your home

Registered home builders advertise

Help to Buy – Wales homes for sale on their

developments. You must reserve your home

and pay a fee of no more than £500 before

you can apply for an equity loan. This fee

is fully refundable if you’re not eligible for

an equity loan or you do not exchange

contracts.

2. Get professional advice

Help to Buy – Wales Ltd will help you to

apply for an equity loan if you’re eligible

and can afford the equity loan on top of

your other outgoings. However they are

notnancialadvisorsandcannotprovide

you with specialist advice. Therefore before

applying to the scheme you must check that

the equity loan meets your needs and that

you can afford to repay it.

Consider seeking independent advice to

helpyouunderstandyournancialsituation.

You can contact Help to Buy – Wales Ltd –

www.gov.wales/help-buy-wales/contact-us

Help to Buy – Wales Buyers’ Guide10

Buying your new home with

an equity loan

Stage 1: Applying

Find your new home

Search online for new homes for sale

using a Help to Buy – Wales: Equity

Loan. Look for the Help to Buy – Wales,

supported by Welsh Government logo

on registered home builders new home

development sites.

Reserve your home

Reserve your home with the home builder

and pay a fee of no more than £500.

This fee is fully refundable if you’re not

approved for an equity loan. Make sure the

homebuilder gives you a signed copy of the

reservation form, you’ll need it when you

apply for the equity loan.

Get nancial advice

Buying a new home can be a daunting

process, but there are many organisations

that offer free advice. Consider seeking

independentnancialadvice.

Apply for your equity loan

You need to complete a Property

Information Form to apply for an equity

loan. You will need to provide personal and

nancialinformation,suchashousehold

income, the property details, your proposed

repayment mortgage and deposit details.

The information you provide when

you apply must be accurate and true.

False details will lead to delays and may

put you at risk of fraud, which is a criminal

offence.

Return your paperwork

Send your signed Property Information

Form and a copy of the home builder’s

signed reservation form to Help to Buy –

Wales Ltd.

11

Updated March 2023

Stage 2: Authority to Proceed

Know how your nances stack up

Help to Buy – Wales Ltd will check if you’re

eligible for the scheme.

Help to Buy – Wales Ltd will use an

eligibility calculator tool to check your

monthly income and outgoings, including

household bills and estimated mortgage

repayments in the calculations. To be

eligible for the scheme your debt or

outgoings must not exceed 45% of your

household income.

Your repayment mortgage should be less

than 4.5 times your gross annual income.

Help to Buy – Wales Ltd are committed

to responsible lending and ensuring

applicants are able to comfortably

afford the shared equity loan. Therefore:

* There is no exibility on Debt to

Household Income Ratios above 45%.

Apply for a repayment mortgage

You are responsible for arranging your

repayment mortgage. Only apply for your

repayment mortgage once you have the

Authority to Proceed from Help to Buy –

Wales Ltd. If you apply for a repayment

mortgagerstandarenoteligibleto

apply for Help to Buy – Wales equity loan,

you may lose money. Your credit rating may

also be affected if the mortgage lender has

carried out a credit check on you.

Get Authority to Proceed

If your application is approved, Help to

Buy – Wales Ltd will give you the Authority

to Proceed (ATP) to buy your new home.

This is valid for 6 months.

When you have the Authority to Proceed,

your conveyancer will receive legal

guidance and forms to complete. Return

these to Help to Buy – Wales Ltd so you

can buy your home.

Your conveyancer is responsible for

explaining the legal information to you.

A list of conveyancers that have undertaken

Help to Buy training can be found at

www.gov.wales/help-buy-wales/how-

apply

Get the conveyancer’s pack

When you have the Authority to

Proceed, your conveyancer will receive

legal guidance and forms to complete.

Your conveyancer is responsible for

explaining the legal information to you.

Help to Buy – Wales Buyers’ Guide

12

Stage 3: Mortgage offer and

exchange of contracts

Your conveyancer will:

• explain the Help to Buy – Wales:

Equity Loan contract and your legal

responsibilities. They will remind you

that your application must be accurate

and true. False or misleading information

could be fraud. This is a criminal offence

and you may have to repay the equity

loan in full;

• ask you to sign the property sale contract

and the Help to Buy – Wales: Equity

Loan contract;

• make sure your repayment mortgage

offer, property price and deposit are the

same amount as agreed in the Authority

to Proceed;

• ask Help to Buy – Wales Ltd for

permission to exchange contracts.

Help to Buy – Wales Ltd will:

Check all the paperwork is correct and

issue the Authority to Exchange (ATE)

to your conveyancer so they can exchange

contracts.

Exchange of contracts is the process where

you and the seller have all the paper work in

place and you legally agree to buy a home.

When contracts are exchanged, you will

need to pay an exchange deposit of 5% to

the seller. At this point, an agreement to buy

becomes legally binding.

You will:

• pay your deposit and be legally bound

to buy your new home by an agreed

date. You pay 5% cash deposit when

you exchange contracts, even if your

full deposit is more;

• make sure your repayment mortgage

offer does not expire before the

completion date.

Home visits

You can visit your new home once you have

exchanged contracts. Your homebuilder

will arrange this for you. This will give you

achancetoconrmanylast-minutedetails

or changes before you move in. Speak to

your conveyancer or your homebuilder for

more information about home visits.

13

Updated March 2023

Stage 4: Completing the purchase

Pay for your new home on completion:

• you pay the rest of your deposit

(if more than 5%);

• your mortgage lender provides its share

of the funds to buy your new home;

• Help to Buy – Wales Ltd will pay your

equity loan to your conveyancer;

• you legally own your new home, get the

keys and can move in.

Conrm the sale

Your conveyancer contacts Help to Buy –

Wales

Ltdtoconrmthesale.

Registration of interest

Your conveyancer will register a legal

charge on your home for Help to Buy

– Wales Ltd. They will also register a

separate legal charge for your mortgage

lender. This is recorded with HM Land

Registry and will be shown on your

property title deeds.

When you’re ready to sell your home,

you need to let us know. You must pay back

your equity loan and repayment mortgage

before we can remove our legal charge

on the property.

Your home

After you buy your home, Help to Buy –

Wales Ltd will:

• set up your Direct Debit to pay the

£1 monthly management fee;

• arrange for you to pay fees and interest

payments on your equity loan;

• help set up repayments when you’re

ready to repay some or all of your

equity loan.

Your home may be repossessed if you

do not keep up repayments on your

repayment mortgage, equity loan or

other loans secured against it. Consider

seeking independent nancial advice

before making any nancial decisions.

Help to Buy – Wales Buyers’ Guide

14

How long does it take to buy

a new home with an equity

loan?

You have 6 months to exchange contracts

when you get our Authority to Proceed.

You must complete buying your home

within 6 months of exchanging contracts.

When you exchange contracts, you make

a legal commitment to buy the property.

If you change your mind, you may have

to pay costs.

15

Updated March 2023

Repaying your equity loan

When you take out your equity loan,

you agree to repay it in full, plus interest

and management fees.

You must repay your equity loan in full:

• at the end of the equity loan term; or

• when you pay off your repayment

mortgage; or

• when you sell your home; or

• if you do not comply with the terms set

out in the equity loan contract and we

ask you to repay the loan in full.

There are no monthly equity loan

repayments to reduce the total amount

of equity loan you borrow. You can pay

off all or part of your equity loan any time

before then.

You may pay back more than you

borrow

The percentage you borrow is based on the

market value of your new home when you

buy it.

When you repay your loan in full or in part,

the amount you pay back is worked out as

a percentage of the market value at the

time you choose to repay.

If the market value of your home rises,

so does the amount you owe on your equity

loan. And if the value of your home falls,

the amount you owe on your equity loan

falls too.

Your home could be at risk if you do not

keep up with repayments on your mortgage,

so it’s important to consider how you will

manage if your home drops in value.

If your home is worth less than when you

bought it, it may affect your ability to pay

your repayment mortgage. Consider talking

toanancialadviseraboutwhatyoucould

do if this happens.

Work out what you need to repay

You can repay your equity loan in full

at any time.

Ifmakingapartialrepayment,yourrst

partial repayment will need to be at least

10% of the market value of your home,

at that time.

The remaining balance of the Help to

Buy – Wales shared equity loan, must be

at least 5% of the market value.

For example, you could repay 10% if you

took out a 20% loan.

To work out how much you pay back we

need to know the current market value

of your home.

You will need to get a Royal Institution

of Chartered Surveyors (RICS) valuation

report.Aqualiedsurveyorwillestimatethe

value of your home, based on its condition

and the current housing market.

If you are selling your home, we use

the current market value of your home

as determined by a Royal Institution of

Chartered Surveyors (RICS) valuer, or the

price it sells for, whichever is highest. In all

other circumstances the market value will

be determined by RICS valuer.

Please note that the valuation will only be

valid for a period of 3 months and the cost

of the valuation is to be paid for by yourself.

Help to Buy – Wales Buyers’ Guide

16

Understanding your interest payments

Interest is what we charge for lending you

the funds to help you buy your Help to Buy

– Wales home.

Interest payments do not go towards paying

off your equity loan.

• You start to pay interest from year 6,

onthefthanniversarythatyoutook

out your equity loan;

• Yourrstinterestpaymentwillbe1.75%

of the amount you borrowed;

• Your interest will go up each year in April

by the Consumer Price Index (CPI),

plus 2%.

The amount of monthly interest you pay

is worked out by multiplying:

1. the Help to Buy – Wales: Equity Loan

amount (purchase price x equity loan

percentage). The equity loan percentage

will reduce following any part repayment.

2. by the interest rate (in the rst year

this is 1.75%). The interest rate increases

every year by adding CPI plus 2%.

The interest rate from the previous year is

then used to work out the interest rate rise

for the following year.

Payments are worked out as an annual

gure and then divided by 12 equal

instalments to get a monthly interest

payment.

Based on the yearly interest rate rises,

it is possible to show the typical annual

and monthly payments, including interest

and management fees. You will receive

a personalised example which estimates

the fees you’ll pay on your equity loan.

Theguresinthisguideareexamplesonly.

Typical annual and monthly payments,

including interest and management fees,

based on an equity loan in a region of

£40,000 and ination (CPI) of 2.5%:

If the market value of your home at the

time of purchase was £200,000 and you

borrowed a Help to Buy – Wales: Equity

Loan amount of £40,000 (20%), in year 6,

onthefthanniversaryoftakingoutyour

equity loan, the interest rate used to work

out your monthly interest fee would be

1.75%. So the sum is: (£40,000 x 1.75%)

÷ 12 = £58.33 interest every month in

year 6.

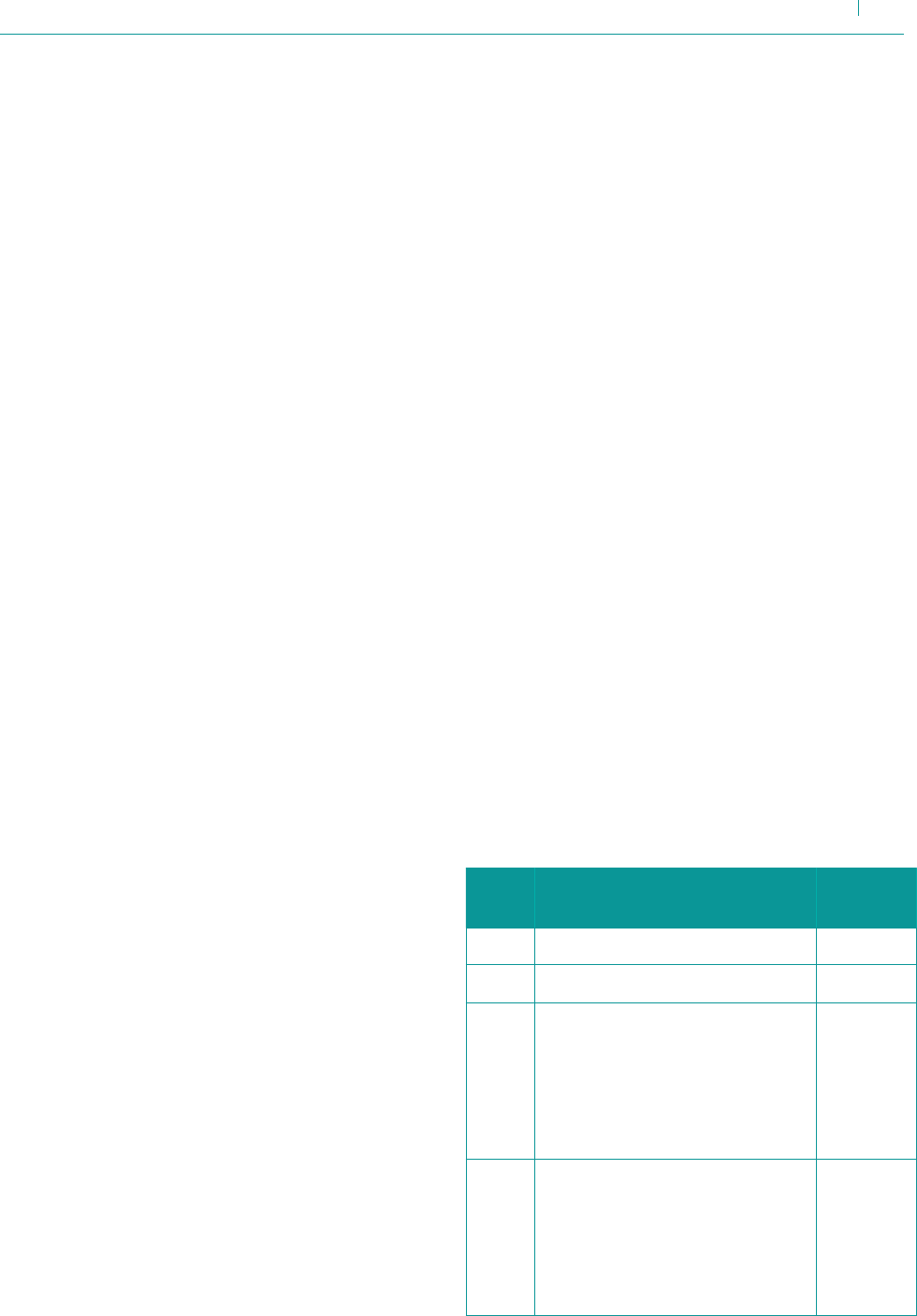

How we work out interest rate

increases

Interest rates go up each year in April by

the Consumer Price Index (CPI), plus 2%.

The table below shows how the interest

rate rise is worked out.

Year Interest rate increase

calculation

Interest

rate

1-5 No interest payments 0%

6 Not applicable 1.75%

7

1.75% (year 6 rate) + 0.08%

1.75% (previous interest

rate) x 4.5%

(2.5% CPI + 2%) = 0.08%

(interest increase)

1.83%

8

1.83% (year 7 rate) + 0.08%

1.83% (previous interest

rate) x 4.5% (2.5% CPI

+ 2%) = 0.08% (interest

increase)

1.91%

17

Updated March 2023

Differences in interest payments

You will pay slightly less interest if you take

out an equity loan at the start of the year,

and slightly more interest if you take it

out later.

Your interest payments start in year 6,

onthefthanniversarythatyoutook

out your equity loan if your equity loan

anniversary is between:

• 1 April and 31 December,yourrst

interest rate rise will be the coming April.

For example, if you take out your equity

loan on 1 June 2023, interest payments

will start on 1 June 2028 (year 6) and

the increase in interest will take place in

April 2029. This means your interest will

rise to the next rate sooner.

• 1 January to 31 March,yourrst

interest rate rise will be a year or more

later in the following April. For example,

if you take out your equity loan on

1 January 2024, interest payments will

start from 1 January 2029 (year 6) and

the increase in interest will take place

in April 2029. This means you will pay

a lower rate of interest for slightly

longer.

What happens if the Consumer Price

Index (CPI) is below 0%?

CPI can go up and down.

If when we work out your interest, CPI is

0%orless,agureof0%willbeusedfor

CPI to calculate your interest rate rise.

This means the interest rate increase will

be a minimum of 2%. CPI will never be less

than 0% when used to work out the interest

rate increase.

Example:

Where CPI is equal to or less than 0%,

we use 0% to work out the interest

rate rise:

0% + 2% = 2% interest rate rise.

Help to Buy – Wales Buyers’ Guide

18

Equity loan fees and costs

You agree to pay the fees and costs when

you take out the equity loan, and these

include:

Monthly management fee

When your equity loan starts you must

pay a £1 monthly fee. This is paid by

Direct Debit for the life of your equity loan.

For example, if you have the equity loan for

5 years (60 months) you will pay a total of

£60 in management fees.

Interest

You start to pay interest from year 6, on the

fthanniversaryofyourequityloanandthis

is calculated at a rate of 1.75% of the equity

loan amount. The interest rate will rise each

year thereafter in April by the Consumer

Price Index (CPI), plus 2%.

The interest you pay during the life of the

equity loan does not reduce the amount

you owe.

The amount of interest you pay will reduce

if you make part repayments. Interest will

be worked out on the amount of equity loan

left to pay.

Administration fees

You may be required to pay administration

fees, for example if you make changes to,

or redeem, your equity loan.

A full list of charges will be available from

Help to Buy – Wales.

In addition to administration fees, you are

responsible for paying other costs and fees,

such as a Royal Institution of Chartered

Surveyors (RICS) valuation report,

legal fees, mortgage arrangement fees.

Costs for late payment

You may be charged interest on overdue

money you owe us. Interest is worked out

based on the amount you owe. Interest is

applied every day until the money you owe

is paid in full. You may also be asked to

pay other reasonable costs that we have

incurred, if we need to take action against

you.

We collect interest and management fee

payments by Direct Debit. This helps to

keep your payment details up to date.

19

Updated March 2023

Help to Buy: Equity Loan

and mortgages

Help to Buy – Wales: Equity Loan normally

has a term of 25 years. If you choose to

switch lenders to get a better deal on your

repayment mortgage, either with your

current or a new lender, you will need to

getourpermissionrst.

Your lender must be a qualifying lender.

You can access the list of qualifying lenders

here www.gov.wales/help-buy-wales-

participating-lenders

If you want to borrow more on your

mortgage, you will need to meet certain

conditions.

You can only borrow more when you

remortgage if you use the money to pay:

• for repayment of all or part of your

equity loan;

• for structural alterations on medical

grounds, if we agree to it;

• to remove or add a homebuyer to the

equity loan agreement (Transfer of

Equity);

• for other personal circumstances that

you agree with us.

Add and remove homebuyers

from the equity loan

With our permission, you can add or

remove a homebuyer from the equity loan.

Homebuyers who are added must meet

our Help to Buy – Wales eligibility criteria.

One of the homebuyers named, must stay

the same as when the equity loan was

taken out.

Help to Buy – Wales Buyers’ Guide

20

Structural alterations

Help to Buy – Wales homes are for buyers,

now and in the future. We want to make

sure they are always affordable.

Making structural alterations to your home

can increase its market value.

You cannot make structural alterations to

your home without our permission, such as

adding an extension or converting a

bedroom into a bathroom.

We will only give permission to make

structural alterations on medical grounds.

The equity loan is linked to the value of your

home. So, if you make structural alterations

without our permission and it increases the

value of your home, the equity loan amount

you owe will increase.

If we give permission to make structural

alterations and the value of your home

increases, we will not consider the value of

that alteration when we work out how much

you owe on your equity loan.

Redecoratingorttinganewkitchenor

bathroom are not structural alterations,

and you do not need our permission to

do this.

You have the option to repay your equity

loan before you make structural alterations.

Other restrictions

You are not allowed to sublet your home

without our consent.

Like your repayment mortgage, you must

have building insurance for your home,

keep it in a good state of repair and comply

with other conditions.

21

Updated March 2023

Start of

year

Property

price

(%) increase

Property price Homebuyer

entitlement:

80%* of property

value

Help to Buy

entitlement:

20% of property

value

1 0% £200,000 £160,000 £40,000

2 2% £204,000 £163,200 £40,800

3 2% £208,080 £166,464 £41,616

4 2% £212,242 £169,793 £42,448

5 2% £216,486 £173,189 £43,297

6 2% £220,816 £176,653 £44,163

* This entitlement excludes any balance you owe on your repayment mortgage

Changes in the housing market could

affect your property price

Changes in the housing market means that house prices can go up and down.

These examples show what could happen if a property price increases.

Increase in a home

In this example, the homebuyer has:

Property value £200,000

Homebuyer’s deposit £10,000 (5%)

Equity loan % £40,000 (20%)

Repayment mortgage £150,000 (75%)

This assumes the property value increases

by 2% every year. If you sell your home at

the start of year 6, you would need to repay

£44,163.

Changes in the housing market could affect

your property price.

Changes in the housing market means that

house prices can go up and down.

Help to Buy – Wales Buyers’ Guide

22

This example shows what could happen

if a property price decreases.

Example 1: Decrease in a home

In this example, the homebuyer has:

Property value £200,000

Homebuyer’s deposit £10,000 (5%)

Equity loan % £40,000 (20%)

Repayment mortgage £150,000 (75%)

This assumes the property value decreases

by 5% every year. If you sell your home at

the start of year 6, you would need to repay

£30,951 (20% of the sale price) to settle

the equity loan. Since the sale price of your

home in this example is less than when you

bought it, it may affect your ability to pay

your repayment mortgage and the Help to

Buy – Wales: Equity Loan.

Start of

year

Property

price

(%) increase

Property price Homebuyer

entitlement:

80%* of property

value

Help to Buy

entitlement:

20% of property

value

1 0% £200,000 £160,000 £40,000

2 -5% £190,000 £152,000 £38,000

3 -5% £180,500 £144,400 £36,100

4 -5% £171,475 £137,180 £34,295

5 -5% £162,901 £130,321 £32,580

6 -5% £154,756 £123,805 £30,951

* This entitlement excludes any balance you owe on your repayment mortgage

23

Updated March 2023

Glossary

Capital repayments

Capital is the money you borrow; interest is

the charge made by the lender (in this case,

Help to Buy Wales Ltd) on the amount

you owe.

Completion

Thisisthenalstageinthesaleofa

property, and the point at which it legally

changes ownership to you, the homebuyer.

Consumer Prices Index (CPI)

CPI is a government annual measure of

ination.CPIismeasuredatdifferentpoints

in the year.

We use the September measurement and

apply it to our interest rate rise every April.

Deposit

A house deposit is usually an upfront

payment which is normally a percentage

of the house price and not included in the

mortgage. In the case of a Help to Buy

Wales home, the deposit at exchange of

contracts must be 5% of the price of the

home.

A deposit is your equity in the house you

buy.

Exchange of contracts

Where you and the seller have all the

paperwork in place, you legally agree to buy

a home. When contracts are exchanged,

you’ll need to pay an exchange deposit of

5% to the seller. At this point, an agreement

to buy becomes legally binding.

Interest

Interest is the cost of borrowing money.

You will usually pay interest for borrowing

money, such as an equity loan. Interest

is usually shown as a percentage of the

amount you borrow. This percentage is

called the interest rate. The higher the rate

of interest, the more interest you pay back.

For example, on £100 at a 5% interest rate

you’ll pay £5 in interest per annum.

Leasehold

You only own a leasehold property for

axedperiod.Aleaseisaprivatelegal

agreement between you and the freeholder

and sets out the rights and responsibilities

of both parties. There may be charges and

fees included in a lease.

There are only a limited number of

leasehold properties that can be purchased

with the support of Help to Buy – Wales.

Market value

The value of a Help to Buy – Wales

home as determined by an independent

organisation called the Royal Institution of

Chartered Surveyors (RICS) valuer, or the

price a home sells for, whichever is highest.

Help to Buy – Wales Buyers’ Guide

24

Mortgage

This is an amount of money you borrow

from a lender to put towards the full asking

price of a property. You normally borrow it

for a set amount of time and pay back a set

amount each month, for an agreed time.

There are 2 main types of mortgage:

• Interest-only – you only pay interest

based on the amount you owe, and these

payments do not reduce how much you

owe. At the end of your mortgage term,

you will still owe the same amount you

borrowed. If you get a Help to Buy –

Wales: Equity Loan, you cannot have

an interest-only mortgage.

• Repayment – you repay the full amount

(capital) borrowed, plus interest.

The amount you owe will decrease

until you repay it all by the end of your

mortgage term.

With Help to Buy – Wales: Equity Loan,

you must have a repayment mortgage.

A mortgage uses your home as security

for the debt, so it is important you’re able

to keep up with mortgage repayments.

Net disposable income

The amount of money left over from your

wages or salary that is available to invest,

save or spend as you please, after bills

and expenses.

New build or new home

A newly built home, including converted

commercial premises and conversions

which have not been used as residential

dwellings before conversion. Homes split

intoatsarenotincluded.Homeswhich

have been previously occupied either by an

owner occupier or a tenant before sale may

not be purchased with Help to Buy.

Part repayment

A minimum voluntary payment of 10%

of the current market value of the home,

paid on top of your regular monthly interest

payments. This will reduce the amount you

owe on the equity loan.

You can repay your equity loan in full

at any time.

Ifmakingapartialrepayment,yourrst

partial repayment will need to be at least

10% of the market value of your home,

at that time.

The remining balance of the Help to Buy –

Wales shared equity loan, must be at least

5% of the market value.

For example, you could repay 10% if you

took out a 20% loan.

Sublet

You are unable to rent out your entire

house to another person/tenant when you

buy a home with Help to Buy – Wales.

You can rent out rooms to lodgers with the

permission of Help to Buy – Wales Ltd,

but you must continue to live in your Help

to Buy – Wales home.

25

Updated March 2023

To apply for a Help to Buy – Wales:

Equity Loan, visit:

www.gov.wales/help-buy-wales/how-apply

This guide is for information only and must

not be considered advice. Consider seeking

independentnancialadvicebeforemaking

anynancialdecisionsonwhethertheHelp

to Buy – Wales: Equity Loan is right for you.

Please be aware that investments can go

down as well as up and you may get back

less than you invested.

Your home may be repossessed if you do

not keep up repayments on your mortgage,

equity loan and other loans secured

against it.

© Crown copyright 2023, Welsh Government, WG47147, Digital ISBN 978-1-80535-632-5

Mae’r ddogfen hon ar gael yn Gymraeg hefyd / This document is also available in Welsh

Rydym yn croesawu gohebiaeth a galwadau ffôn yn Gymraeg / We welcome correspondence and telephone calls in Welsh

Help to Buy – Wales Buyers’ Guide

26