Stephen F. Austin State University Stephen F. Austin State University

SFA ScholarWorks SFA ScholarWorks

Faculty Publications Gerald W. Schlief School of Accountancy

2017

Lumberjack Construction: Job-Order Costing & Manufacturing Lumberjack Construction: Job-Order Costing & Manufacturing

Simulation Simulation

Marie Kelly

Stephen F Austin State University

Nikki Shoemaker

Stephen F Austin State University

Follow this and additional works at: https://scholarworks.sfasu.edu/accounting_facultypubs

Part of the Accounting Commons, Educational Methods Commons, and the Finance and Financial

Management Commons

Tell us how this article helped you.

Repository Citation Repository Citation

Kelly, Marie and Shoemaker, Nikki, "Lumberjack Construction: Job-Order Costing & Manufacturing

Simulation" (2017).

Faculty Publications

. 36.

https://scholarworks.sfasu.edu/accounting_facultypubs/36

This Article is brought to you for free and open access by the Gerald W. Schlief School of Accountancy at SFA

ScholarWorks. It has been accepted for inclusion in Faculty Publications by an authorized administrator of SFA

ScholarWorks. For more information, please contact [email protected].

16 Journal of Accounting and Finance Vol. 17(5) 2017

Lumberjack Construction: Job-Order Costing & Manufacturing Simulation

Marie Kelly

Stephen F. Austin State University

Nikki Shoemaker

Stephen F. Austin State University

This paper describes a classroom Job-Order Costing and manufacturing simulation called Lumberjack

Construction. This simulation is used in introductory managerial accounting and cost accounting courses

to help students understand the various parts of the manufacturing process and the application of Job-

Order Costing principles. For this simulation, students are placed into manufacturing groups. Each

group is responsible for manufacturing a building and calculating the cost of that building using job-

order costing.

INTRODUCTION

Concepts in introductory managerial accounting and cost accounting courses can be challenging for

students and faculty because many of these concepts are rooted in manufacturing. However, few students

have been exposed to a manufacturing environment. In these courses, students are also introduced to

multiple ways of allocating costs to jobs and products. The combination of an unfamiliar work setting and

the introduction of multiple abstract allocation concepts make it difficult for faculty to help students grasp

these principles. Nevertheless, it is important for students to understand how costs are distributed among

different products, as this information is vital not only to accounting majors, but across numerous

business disciplines such as marketing, management, economics, and finance. This paper describes a Job-

Order Costing and manufacturing simulation that promotes understanding of the cost allocation process,

the manufacturing environment and the tracking of costs within this environment.

The remainder of this paper is organized as follows. First, the Job-Order Costing/Manufacturing

simulation is described. Second, learning objectives along with guidance on simulation implementation is

discussed. Third, evidence supporting the efficacy of the simulation is considered.

JOB-ORDER COSTING AND MANUFACTURING SIMULATION

Students often have difficulty understanding managerial accounting concepts that are based in a

manufacturing environment. Most introductory managerial accounting textbooks initially teach cost

terminology and then introduce job order costing to assign direct materials, direct labor, and to apply

manufacturing overhead costs to products. Students are often confused with these concepts as they have

never been exposed to a manufacturing environment. Consequently, terminology such as direct labor.

Journal of Accounting and Finance Vol. 17(5) 2017 17

direct materials, and materials requisitions is difficult to understand because they are not able to apply this

terminology to a real-life scenario. In order to improve comprehension of these concepts, this simulation

lets students complete a small scale building project within the classroom and calculate costs of their

building.

At the beginning of this project, students are divided into groups to model a manufacturing facility.

Once groups are assigned, each group is required to choose one student in their group to be the designated

student supervisor. The supervisors assemble at the front of the room to get their production assignments

from factory management. Each supervisor receives a packet that contains the following: Supervisor

Handout, Materials Requisition Form, Time Report Sheet, Overhead Application Sheet, Job Cost Sheet,

and blueprints for their construction project. Sample forms are provided in Appendices A - E.

Each group supervisor chooses a Materials Handler within their group, and assigns assembly jobs

based on the information in their Supervisor Handout. The Materials Handler fills out the Materials

Requisition Form for the number of items needed to manufacture their building and calculates the total

cost of these materials. The supervisor reviews this form and if the materials requisition form is filled out

correctly, the Materials Handler comes up to the front of the room to receive materials for construction

from the Materials Inventory warehouse manager, a.k.a. the instructor. Each group then works through

the blueprints to understand how the building will be manufactured. As Direct Labor employees begin

construction, group supervisors start monitoring their time, with one minute equivalent to 100 hours of

Direct Labor construction time. Once they have completed the manufacturing process, students in the

group work together to determine the cost of the building their group has manufactured. Student

supervisors are responsible for ensuring that each student participates and Job Cost calculations, including

Direct Materials, Direct Labor, and Applied Manufacturing Overhead, are agreed upon by all group

members before a project is deemed complete. Once the Materials Handlers job is complete and

construction has started, their position converts to Quality Control Inspector, where they must examine

and approve all finished products.

LEARNING OBJECTIVES AND SIMULATION IMPLEMENTATION

Learning Objectives

The Job-Order Costing/Manufacturing Costing simulation provides three specific learning objectives.

The first objective illustrates a simulated manufacturing environment using a building project. Requiring

students to work in groups to construct a building and complete source documents related to this project

reinforces concepts such as direct labor, direct materials and indirect costs.

The second learning objective is to enhance student comprehension of the application of job-order

costing. During the construction process, students are required to be aware of the costs of their job. They

must complete a materials requisition sheet for their building materials, keep a time sheet to record direct

labor hours, and complete a job cost sheet to calculate the final cost of their building. These steps

reinforce to students how source documents are used to determine the final cost of a job or product.

Finally, students gain awareness of the impact of various components of the manufacturing process

on total job cost. Through group and class discussion toward the end of the simulation, students realize

that assigning direct labor hours as a cost driver not only influences the direct labor cost associated with

the job, but also the overhead applied to the project. This allows the students to understand why efficient

use of labor time is important for cost control.

Implementation Guidance

Background

The current version of the project has been developed as a result of many other trials. This project

originally began as a key chain building project where students manufactured key chains during class.

This experience led us to realize that there was value in having different groups complete different types

of products. So, we developed a simulation where students manufactured small crafts (i.e., wooden

airplanes, pinwheels, sail boats, etc.). This version of the project was not ideal either because it cost a

18 Journal of Accounting and Finance Vol. 17(5) 2017

significant amount of money to purchase these items for use each semester. Consequently, we developed

the current version of the simulation discussed in this article. This version allows students to construct

multiple different types of products, but allows the instructor to reuse materials from semester to

semester.

Courses

This simulation was designed for an introductory managerial accounting course, which is normally

the second accounting class that a college business student will take, after introductory financial

accounting. It has been implemented in medium to large classes of up to 70 students. It is most effective

in medium-sized classes of around 50 students. Students attending these courses include accounting,

economics, finance, management, marketing, and general business majors. In addition, the project has

been used as a review tool for cost accounting classes.

This project simulation is normally presented in class following the Job-Order costing lecture. It is

important for the project to be placed at this point in the curriculum because students need a basic

background in job-order costing to understand the various components of the simulation. Project points

are included within the overall points awarded during the semester for the class, in order to persuade

students to attend and participate.

Materials

The simulation requires materials for two sets of each of the five different types of buildings. Two

100 piece sets of magnetic building tiles were purchased to provide the necessary materials. A sample of

the buildings and materials required are included in the appendices. Students should be instructed to

replace all materials back in their bag as soon as the project is over to ensure that building tiles are not

lost and can be used for future classes. Materials cost is approximately $200.00

In-class implementation

The project takes approximately one hour of class time to complete. In order to create variation

among students within the classroom and control project simulation outcomes, five different building

projects were created. Two student groups are assigned to each building, for a total of ten groups. This

allows for cost comparisons between the two groups who built the same building. A sample of the

Townhome project blueprints are included in Appendix F. Sample source documents are included in

Appendices A - E.

Evidence of Efficacy

This simulation was initially used in four different introductory managerial accounting classes taught

by two different accounting instructors over a period of two semesters. To determine effectiveness of the

project, the same exam administered in previous semesters testing Job Order Costing concepts without

this simulation project was administered during later semesters after the simulation project was

implemented.

The pre-simulation and post-simulation exams were identical, the classes used the same textbook, the

instructors were unchanged, and the exams were given at the same point during the semester calendar. In

all classes, the average increase in exam scores was approximately 8 to 10 points, between the pre and

post-simulation semesters. These results suggest significant improvement in student understanding of Job

Order Costing methods and applications as a result of this project simulation. In addition, student

approval measured by teaching evaluations indicated an increased appreciation for this experiential

learning activity.

Journal of Accounting and Finance Vol. 17(5) 2017 19

APPENDIX A

SUPERVISOR HANDOUT

It is your job to make sure that the manufacture of your product goes smoothly and that all costs are

recorded and accounted for. This means that you must:

1) Appropriately assign jobs to individuals in your group

1 supervisor

1 materials handler

1 quality control inspector

Remaining group members are construction workers

2) Make sure that you receive the materials requisition for your job.

a. This will be obtained from the materials handling personnel after they have received all

materials from the warehouse and distributed the materials to the employees using those

materials.

b. Materials will not be released without an accurate materials cost on your materials

requisition.

3) Make sure that you keep track of the amount of direct labor time spent working on your jobs

(Time starts when the first construction worker begins working and ends when the last

construction worker finishes working.)

a. This will be used to calculate the cost of direct labor (see the time report sheet)

b. NOTE: 1 minute = 100 direct labor hours

4) Make sure that operations are running smoothly and that all employees are actively

participating in the manufacturing process.

a. If there is an issue with operations, you should determine a solution to make operations

run more smoothly.

5) Help your group calculate the total cost of your job using the materials requisition, time

report, and overhead application sheets. Complete this cost calculation on the job cost sheet.

20 Journal of Accounting and Finance Vol. 17(5) 2017

APPENDIX B

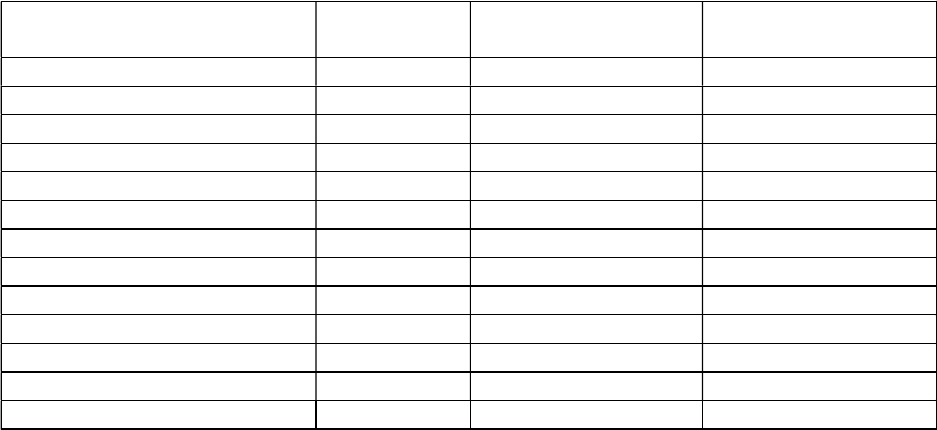

MATERIALS REQUISITION FORM

FIGURE 1

Materials Requisition

Townhome

Materials Requisition Number: _________ Date _____________

Job Number: ________

Description: __________________________________________________________

Material Description Quantity Unit Cost Total Cost of

Material

Equilateral Triangle-Green 6 $9,000.00

Equilateral Triangle-Red 2 $9,000.00

Equilateral Triangle-Orange 6 $9,000.00

Equilateral Triangle-Yellow 2 $9,000.00

Large Triangle-Yellow 2 $52,000.00

Small Square-Green 2 $12,000.00

Small Square-Yellow 6 $12,000.00

Small Square-Orange 3 $12,000.00

Small Square-Red 4 $12,000.00

Holey Square-Orange 2 $16,200.00

Rectangle-Purple 2 $4,500.00

Rectangle-Yellow 3 $4,500.00

Large Square-Red 2 $75,000.00

Total Cost of All Materials Used: _________________

Authorized Signature: _________________________________

Journal of Accounting and Finance Vol. 17(5) 2017 21

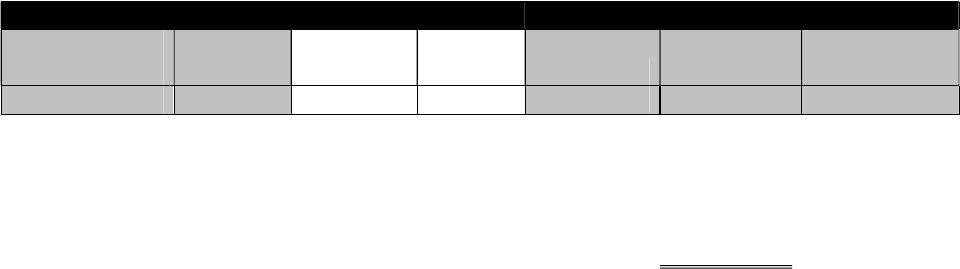

APPENDIX C

TIME REPORT

FIGURE 2

Time Report

Date: _____________

Job Number: ________

Description: __________________________________________________________

Time

Started Time Ended Total Time

Hourly

Rate

Number of DL

Employees

Total

Amount

$10.00

NOTE: 1 minute = 100 hours of direct labor

Authorized Signature: _________________________________

APPENDIX D

OVERHEAD APPLICATION SHEET

FIGURE 3

Overhead Application

Total Estimated Yearly Overhead

Glue $20,000.00

Nails $40,000.00

Paint $60,000.00

Hammers $10,000.00

Trucks (Depr., Repairs, Main., Gas) $170,000.00

Materials Handlers Salaries $240,000.00

Trash Cleanup Personnel Salaries $100,000.00

Inspection Costs $360,000.00

Supervisors Salaries $500,000.00

Total OH $1,500,000.00

Cost Driver: Direct Labor Hours

Total Estimated Yearly Direct Labor Hours = 50,000 DLH

Step 1: Calculate the OH Rate

Step 2: Apply OH to your products

22 Journal of Accounting and Finance Vol. 17(5) 2017

APPENDIX E

JOB COST SHEET

FIGURE 4

Job Cost Sheet

Job Number: ________

Time Started _____________

Time Completed _____________

Description: __________________________________________________________

Direct Materials Direct Labor Applied Manufacturing Overhead

Requisition

No. Amount Ticket No. Amount OH Rate

Actual Cost

Driver Amount

Cost Summary:

Direct Materials Cost ____________

Direct Labor Cost ____________

Applied Manufacturing Overhead Cost ____________

Total Cost of Job ____________

Authorized Signature: _________________________________

Journal of Accounting and Finance Vol. 17(5) 2017 23

APPENDIX F

SAMPLE BLUEPRINTS FOR TOWNHOME

24 Journal of Accounting and Finance Vol. 17(5) 2017

Journal of Accounting and Finance Vol. 17(5) 2017 25

26 Journal of Accounting and Finance Vol. 17(5) 2017

Journal of Accounting and Finance Vol. 17(5) 2017 27