REPORT ON EXAMINATION

OF

CAPITAL DISTRICT PHYSICIANS’ HEALTH PLAN, INC.

AS OF

DECEMBER 31, 2017

EXAMINER: GAIL A ROSS

DATE OF REPORT: OCTOBER 5, 2023

TABLE OF CONTENTS

ITEM

PAGE

NO. NO.

1.

Scope of the examination

2

2.

Description of the HMO

5

A.

Corporate governance

6

B.

Territory and plan of operation

12

C.

Reinsurance

14

D.

Holding company system

17

E.

Significant operating ratios

21

3.

Medical Loss Ratio (“MLR”)

21

A.

Market classification

21

B

MLR numerator

23

C

MLR denominator

26

D

Credibility Adjustment

27

E

Credibility - Adjusted MLR

28

F

Rebate disbursement and notice

28

G

Impact on risk-based capital

29

4.

Financial statements

30

A.

Balance sheet

31

B.

Statement of revenue, expenses, capital and surplus

32

5.

Claims unpaid

33

6.

Subsequent events

34

7.

Compliance with prior report on examination

35

8.

Summary of comments and recommendations

38

October 5, 2023

Honorable Adrienne A, Harris

Superintendent of Financial Services

Albany, New York 12257

Madam:

Pursuant to the requirements of the New York Insurance Law and the New York State

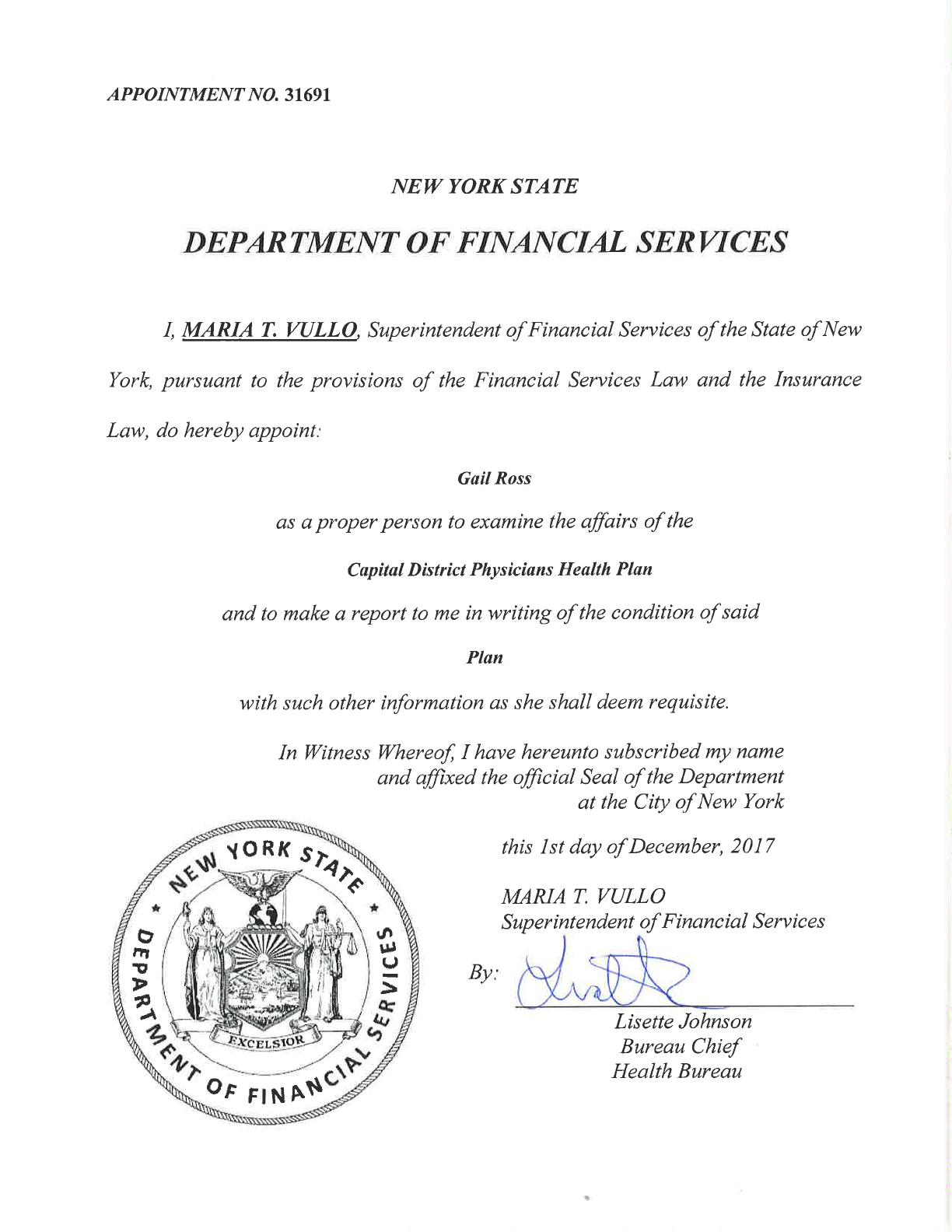

Public Health Law, and acting in accordance with the instructions contained in Appointment

Number 31691, dated December 1, 2017, attached hereto, I have made an examination into the

condition and affairs of Capital District Physicians’ Health Plan, Inc., a not-for-profit health

maintenance organization (“HMO”), issued a certificate of authority by the New York State

Department of Health (“NYSDOH”) under the provisions of Article 44 of the New York Public

Health Law, as of December 31, 2017. The following report is respectfully submitted thereon.

The examination was conducted at the administrative office of Capital District Physicians’

Health Plan, Inc. located at 500 Patroon Creek Boulevard, Albany New York.

Wherever the designations “CDPHP” or the “HMO” appear herein, without qualification,

they should be understood to indicate Capital District Physicians’ Health Plan, Inc. CDPHP is

also the ultimate parent within the holding company system.

2

Wherever the designation the “UBI” appears herein, without qualification, it should be

understood to indicate CDPHP Universal Benefits, Inc., a subsidiary corporation within CDPHP

holding company system.

Wherever the designation the “Department” appears herein, without qualification, it should

be understood to indicate the New York State Department of Financial Services.

Concurrent financial and Medical Loss Ratio (MLR) examinations were made of UBI, a

not-for-profit corporation licensed pursuant to the provisions of Article 43 of New York Insurance

Law. A separate report thereon has been submitted.

A separate Market Conduct examination reviewing the manner in which the HMO

conducted its business practices and fulfilled its contractual obligations to policyholders and

claimants was also conducted as of December 31, 2017. A separate report thereon has been

submitted.

1. SCOPE OF THE EXAMINATION

The prior examination of the HMO was conducted as of December 31, 2014. This

examination of the HMO was a financial examination as defined in the National Association of

Insurance Commissioners (“NAIC”) Financial Condition Examiners Handbook 2018 Edition (the

“Handbook”) and covered the three-year period January 1, 2015 through December 31, 2017. The

examination was conducted observing the guidelines and procedures in the Handbook. Where

deemed appropriate by the examiner, transactions occurring subsequent to December 31, 2017

were also reviewed.

3

The examination was conducted on a risk-focused basis in accordance with the provisions

of the Handbook, which provides guidance for the establishment of an examination plan based on

the examiner’s assessment of risk in the HMO’s operations and utilizes that evaluation in

formulating the nature and extent of the examination. The examiner planned and performed the

examination to evaluate the HMO’s current financial condition, as well as identify prospective

risks that may threaten the future solvency of CDPHP.

The examiner identified key processes, assessed the risks within those processes, and

assessed the internal control systems and procedures used to mitigate those risks. The examination

also included an assessment of the principles used and significant estimates made by management,

an evaluation of the overall financial statement presentation, and determined management’s

compliance with the Department’s statutes and guidelines, Statutory Accounting Principles, as

adopted by the Department, and annual statement instructions.

Information concerning the HMO’s organizational structure, business approach, and

control environment was utilized to develop the examination approach. The examination

evaluated the HMO’s risks and management activities in accordance with the NAIC’s nine branded

risk categories. These categories are as follows:

• Pricing

• Underwriting

• Reserving

• Operational

• Strategic

• Credit

• Market

• Liquidity

• Legal

• Reputational

4

The examination also evaluated CDPHP’s critical risk categories in accordance with the

NAIC’s ten critical risk categories. These categories are as follows:

• Valuation Impairment of Complex or Subjectively Valued Invested Assets

• Liquidity Considerations

• Appropriateness of Investment Portfolio and Strategy

• Appropriateness Adequacy of Reinsurance Program

• Reinsurance Reporting and Collectability

• Underwriting and Pricing Strategy Quality

• Reserve Data

• Reserve Adequacy

• Related Party Holding Company Considerations

• Capital Management

The HMO was audited annually during the years covered by this examination. by the

accounting firm Deloitte and Touche (“D&T”). The HMO received an unmodified opinion in each

of those years. Certain audit work papers of D&T were reviewed and relied upon in conjunction

with this examination. A review was also made of the HMO’s corporate governance structure,

which included its Internal Audit function and Enterprise Risk Management program.

A review was made of the HMO’s compliance with the provisions of Insurance Regulation

No. 118 (11 NYCRR 89), “Audited Financial Statements.” This regulation is based on the Model

Audit Rule (“MAR”), as established by the NAIC, and all references to MAR within this report

may be interpreted as reference to Insurance Regulation No. 118. Additionally, as part of this

examination, and in accordance with the provisions of the Handbook, a review was made of

CDPHP’s computer systems and operations that support the HMO on a risk-focused basis.

The examiner reviewed the corrective actions taken by the HMO with respect to the

recommendations concerning financial issues contained in the prior report on examination. The

results of the examiner’s review are contained in Item 7 of this report.

5

This report on examination is confined to financial statements and comments on those

matters which involve departure from laws, regulations or rules, or which require explanation or

description.

2. DESCRIPTION OF THE HMO

Capital District Physicians’ Health Plan, Inc. was formed as a membership corporation on

February 27, 1984, under Section 402 of the Not-for-Profit Corporation Law, and subsequently

incorporated within the State of New York on April 13, 1984. The members consist of physicians

licensed by the State of New York. CDPHP, a health maintenance organization (“HMO”),

certified pursuant to Article 44 of the New York Public Health Law, obtained its certificate of

authority to operate as an independent practice association (“IPA”) model HMO from the New

York State Department of Health (“DOH”), effective April 30, 1984. The HMO commenced

business on July 12, 1984.

As of December 31, 2017, membership in the HMO was opened to physicians licensed by

the State of New York, who applied for membership and met the criteria required by the HMO’s

by-laws and were accepted as member physicians.

The HMO is a not-for-profit health insurer which is exempt from income taxes under the

provisions of Section 501(c)(4) of the Internal Revenue Code.

On January 14, 2015 CDPHP requested approval for a $50 million secured revolving line

of credit from First Niagara Bank, NA (“FNB”). The proposed two-year secured $50 million line

of credit would replace the existing $35 million unsecured line of credit with FNB. On March 5,

2015 the Department approved the $50 million secured line of credit.

6

Under the provisions of Part 98-1.11(f) of the Administrative Rules and Regulations of

New York State Department of Health (10 NYCRR 98-1.11(f)), each health maintenance

organization initiating operations under the authority of Article 44 of the New York State Public

Health Law shall establish a deposit in the form of an escrow account for the protection of

enrollees, in an amount equal to the greater of five percent of the estimated expenditures for health

care services for the year or $100,000. On November 30, 2016, the Department approved the

withdrawal of $3,500,000 from the escrow deposit. Pursuant to the provisions of Part 98-1.11(f)

of the Administrative Rules and Regulations of the New York State Department of Health (10

NYCRR 98-1.11(f), the HMO established an escrow account in the amount of $66,521,593, as of

December 31, 2017.

The HMO made the following cash contributions to UBI:

• Effective December 10, 2015 and December 15, 2015, the New York State Department of

Financial Services and the New York State Department of Health, respectively, approved

CDPHP’s proposal to invest $50 million in UBI.

• Effective November 25, 2016 and December 2, 2016, the New York State Department of

Financial Services and the New York State Department of Health, respectively, approved

CDPHP’s proposal to invest $50 million as additional paid in capital to UBI.

As of December 31, 2017, the total value of all cash infusions from the HMO to UBI

equated to $124,846,345, the net worth of UBI.

A. Corporate Governance

The HMO is a physicians’ controlled corporation. The participating physicians, who are

members in good standing with the corporation, constitute a majority of the corporation’s board of

directors.

7

Pursuant to the HMO’s Certificate of Incorporation and by-laws, management of the HMO

is to be vested in a Board of Directors (“BOD”) consisting of fifteen (15) members. Eight (8) of

the fifteen (15) members of the BOD include CDPHP’s physicians members and the remaining

seven (7) directors comprise individuals who are non-physician members of the HMO.

Part 98-1.11(g)(1) of the Administrative Rules and Regulations of the Health Department

(10 NYCRR 98-1) requires that a minimum of twenty percent (20%) of the Board of Directors of

the HMO must be comprised of enrollee representatives, and at least one-third (1/3) shall be

persons who reside in New York State. As of the examination date, CDPHP Board was comprised

of fifteen (15) directors.

As of December 31, 2017, the Board and their principal business affiliation were as

follows:

Name and Residence

Principal Business Affiliation

Catherine Roberts Bartholomew, MD

Albany, New York

Medical Doctor,

Albany Medical Center

Holly Krick Cleney, MD

Latham, New York

Primary Care Physician,

Latham Medical Group

Bruce Evan Coplin, MD*

Delmar, New York

Medical Doctor,

Albany Associates in Cardiology

Gennaro Anthony Daniels, MD*

Troy, New York

Surgeon,

Capital District Colon & Rectal Surgery

Associates, PC

Joseph James Dudek, MD*

Delmar, New York

Medical Doctor,

NY Oncology Hematology, PC

Richard Edward Grant

Retired

Glenmont New York

8

Name and Residence

Gerald David Jennings

Albany, New York

Amy Michelle Johnson

Loudonville, New York

Anthony James Marinello, MD*

Guilderland, New York

Thomas John Marusak*

Loudonville., New York

Carmen Vito Mazzotta

Niskayuna, New York

Henry McDougall Neilley, MD*

Clifton Park, New York

William Patrick Phelan*

Loudonville, New York

Joseph Michael Polito, II, MD*

Albany, New York

Susan Crosby Scrimshaw, PhD*

Troy, New York

Principal Business Affiliation

Retired

President,

Capstone, Inc.

Medical Doctor,

Capital Care Family Practice

President,

Comfortex Corporation

President,

Health Capital Partners, LTD

Medical Doctor,

Shaker Pediatrics

Chief Executive Officer,

Bright Hub, Inc.

President,

Albany Gastroenterology Consultants,

PLLC.

President,

The Sage Colleges

* Enrollee representative per Part 98-1.11(g) of the Administrative Rules and Regulations of the Department of Health (10 NYCRR 98-

1.11). The composition of the Board meets the requirements of 10 NYCRR 98-1.11(g) as of December 31,2017.

The minutes of all meetings of the Board of Directors and sub-committees thereof held

during the examination period were reviewed. The BOD met at least six times during each

calendar year within the examination period, and the sub-committees also met at various times

annually on a regular basis throughout the examination period. A review of the minutes of the

HMO’s BOD and sub-committees’ meetings evidenced that the meetings were generally well

attended, with all BOD and sub-committee members attending at least one half of all the meetings

they were eligible to attend.

9

The principal officers of the HMO as of December 31, 2017 were as follows:

Name

Title

John Duncan Bennett, M.D.

President and Chief Executive Officer

Bethany Rea Smith CPA

EVP, Finance & Chief Financial Officer

The HMO Audit Committee Charter states in part:

“The Audit Committee shall be comprised of the Treasurer of the

Corporation and two or more other directors, …” and “The Treasurer shall

serve as the Chair of the Committee

.”

Pursuant to the HMO’s Audit Committee charter, the Chair of the Audit Committee shall

be the Treasurer of the corporation. However, the examiner noted that the HMO did not have a

Treasurer of Corporation, and the current Chair of the Audit Committee was the Treasurer of the

Board of Directors.

It is recommended that the HMO comply with its Audit Committee charter by having the

Treasurer of the Corporation serve as Chair of the committee.

On June 25, 2018, the Audit Committee updated the Charter from the Chair of the

committee being the “Treasurer of the Corporation” to the “Treasurer of the Board of Directors.”

Enterprise Risk Management

The HMO is required to be compliant with Insurance Regulation No. 203 (11 NYCRR 82)

as it relates to Enterprise Risk Management (“ERM”) and Own Risk Solvency Assessment

(“ORSA”). The HMO has a formal ERM framework with defined risk appetites and tolerances for

proactively addressing and mitigating risks, including prospective business risks. Exhibit M of

10

the Handbook (Understanding the Corporate Governance Structure) was utilized by the examiner

as guidance for assessing corporate governance. Overall, it was determined that CDPHP’s Board

and key executives maintain an effective control environment.

In addition, CDPHP has established a Government Affairs Department to address emerging

policy issues within the health insurance industry and those facing CDPHP and all of its affiliates.

As issues are identified, CDPHP establishes leadership teams to gain an understanding of the

impact on the CDPHP Companies. These leadership teams are developed to provide

recommendations to the members of the executive team, which is responsible for CDPHP’s

strategy on emerging issues.

Information Technology (“IT”)

The examination encompassed a review of the controls for financially significant

applications, systems and infrastructure. The IT portion of the examination was performed in

accordance with the Handbook and utilized applicable procedures found in Exhibit C – Evaluation

of Controls in Information Technology – of the Handbook.

Controls for financially significant applications, systems, and underlying infrastructure in

each of the NAIC Exhibit C Information Technology Work Program areas listed below represent

the framework for the scope of this examination. The following control areas were reviewed:

• Align, Plan and Organize;

• Build, Acquire and Implement;

• Deliver, Service and Support; and

• Monitor, Evaluate, and Assess.

11

The IT examination team concluded that CDPHP’s IT General Controls (“ITGCs”) are

“Effective,” resulting in the conclusion that ITGCs are reliable for the purposes of this financial

examination. The IT review conclusions were based on inquiry, observation, inspection of

documentation, independent research and a review of third-party workpapers.

The IT examination team assessed CDPHP’s compliance with the provision of the

Financial Services Regulation Part 500 (23 NYCRR 500) – “Cybersecurity Requirements for

Financial Services Companies.” CDPHP appears to be in compliance with the sections of the New

York Cybersecurity Regulation that have already taken effect through March 2018, and they

appear to be ready for the remaining sections as they come due. This conclusion was based on a

review of the responses provided by CDPHP to the Department’s Cybersecurity letter, review of

prior third-party control assessments, inspection of documentation, observation, and management

interviews.

Internal Audit Department

CDPHP, the ultimate parent established an Internal Audit Department (“IAD”) function to

serve all subsidiaries and affiliates within its holding company system. The IAD reports to the

Audit Committee (“AC”) of the Board of the Directors.

The IAD assists all levels of management by reviewing and testing financial and

operational controls and processes established by management to ensure compliance with laws,

regulations and policies. It shall be noted that the IAD testing of controls includes a process which

Corporate Team Leaders (“CTL”) from each business unit perform their own internal control

testing of those items deemed “high risk” and “not low risk”. To the extent that IAD reperformed

this testing without confirming the sampling methodology used by the business units, the examiner

12

did not rely upon the work performed by the IAD and, as prescribed by the Handbook, performed

additional testing.

Insurance Regulation No. 118 (11NYCRR 89)

The HMO is a non-publicly traded company and therefore not subject to the Sarbanes-

Oxley Act of 2002. Insurance Regulation 118 No. (11 NYCRR 89) – “Audited Financial

Statements,” is similar to the NAIC’s Model Audit Rule (“MAR”), and therefore applies to certain

New York regulated insurance entities, including CDPHP. Insurance Regulation No. 118 became

effective January 1, 2010. The Audit Committee for CDPHP, which is composed of outside

directors, assumed responsibility for all entities within the holding company structure. With the

independent and internal auditors, the CDPHP Audit Committee reviews the effectiveness of the

accounting and financial controls and elicits recommendations that may improve controls. CDPHP

Audit Committee met each quarter during the examination period, and meeting minutes were

prepared and retained.

B. Territory and Plan of Operation

The HMO is certified to operate business in New York State only. The HMO’s service

area, as authorized in its Certificate of Authority, includes the following twenty-four (24) counties

in the State of New York. Effective February 22, 2016, the Certificate of Authority was reissued

for inclusion of approved counties for the Child Health Plus (“CHP”) and Medicare Advantage

Programs:

Albany

Broome

Chenango

Columbia

Delaware

Dutchess

Essex

Fulton

Greene

Hamilton

Herkimer

Madison

Montgomery

Oneida

Orange

Otsego

Rensselaer

Saratoga

13

Schenectady

Schoharie

Tioga

Ulster

Warren

Washington

The HMO provides a comprehensive prepaid health program by means of a network of

participating physicians. Subscribers to the HMO select a participating physician who acts as their

primary care physician. This physician refers members to other participating HMO physicians

when particular medical specialties are required. Except for services specifically excluded or

limited in the HMO’s contracts or riders, there is no limit to duration, frequency or type of health

care provided, as long as the care is directly provided or pre-authorized by the HMO’s medical

director and/or the primary care physician.

Inpatient hospital services are rendered as directed by the HMO’s participating physicians.

The HMO pays hospital charges through direct hospital billing. Out-of-area emergency care is

provided for in the subscriber contracts.

The charts below illustrate the HMO’s annual year-end enrollments and premium writings

during the examination period.

CDPHP Year-end Annual Enrollment

Line of Business

2015

2016

2017

Direct Pay

4,600

5,033

4,663

Large Group

75,645

68,008

66,159

Small Group

4,725

0

0

Healthy New York

1,645

1,917

1,957

Medicare Advantage Part. D

39,876

37,171

37,144

Medicaid

96,422

85,063

81,460

Child Health Plus

12,820

12,613

12,998

Health & Recovery Plan (HARP)

__0

2,097

2,672

Total

235,733

211,902

207,053

14

During the examination period, the HMO’s overall annual enrollment decreased by

approximately 13.9% from 235,733 total enrollees as of December 31, 2015 to 207,053 enrollees

as of year-end 2017. Declining enrollment was due to premium pricing that is not competitive in

the current market.

The HMO’s direct written premiums for each year under examination were as follows:

CDPHP Year-end Annual Premiums (000 omitted)

Line of Business 2015 2016 2017

Direct Pay

$ 40,225

$ 38,975

$ 35,857

Large Group

467,706

449,125

450,999

Small Group

39,114

4,602

1,128

Healthy New York

7,380

5,289

4,635

Title XVIII - Medicare

430,074

434,487

430,256

Medicaid

492,445

461,142

431,154

Child Health Plus

36,202

34,336

36,696

Health & Recovery Plan (“HARP”)

0

17,372

51,834

Total gross premiums

$1,513,146

$1,445,328

$1,442,559

Percentage Change in net Premiums

(4.5) %

(0.2) %

CDPHP’s reported total gross annual premium of $1,513,146, as of December 31, 2015

and $1,442,559 as of December 31, 2017, representing an overall percentage decrease of 4.7% for

the period under examination. The premiums written have a direct relationship to the decrease in

membership, as noted above.

C. Reinsurance

As of December 31, 2017, CDPHP maintained ceded reinsurance agreements with Carter

Insurance Company Ltd. of Hamilton Bermuda (“Carter”), a wholly owned subsidiary of CDPHP,

15

and also with Atlantic Specialty Insurance Company, a nonaffiliated and New York authorized

insurer. The two agreements comprised the following reinsurance coverage:

Carter Insurance Company Cession:

1

st

Layer (Specific/Excess Retention)

CDPHP’s retention Reinsurer’s obligation

CDPHP retains 100% of the first $750,000 and

Reinsurer pays 90% of CDPHP’s incurred

10% above $750,000 of incurred losses per

losses above $750,000 up to a maximum

covered member, each per covered line of limit of $1,250,000 per

each covered

business, up to a maximum of $1,250,000. member.

Atlantic Specialty Insurance Company Cession:

2

nd

Layer (Excess of Loss Coverage) ________

CDPHP’s retention Reinsurer’s obligation

CDPHP retains 10% of all inpatient

Reinsurer pays 90% of CDPHP’s incurred

losses incurred losses per member above

losses above $1,250,000 up to a maximum

$1,250,000 up to a maximum limit of limit of $1,750,000.

1,750,000.

The HMO’s ceded reinsurance program applied to all CDPHP’s commercial business, and

all government Medicare and New York State products excluding Medicaid business.

As noted above, CDPHP’s first layer reinsurance cession program with Carter called for

Carter to reinsure CDPHP’s inpatient hospital services at 90% of the total hospital payments by

the HMO beginning at the attachment point above $750,000 of paid losses per covered member,

up to Carter’s maximum of $1,250,000. The second layer cession program, with Atlantic Specialty

Insurance Company, calls for the reinsurer to cover 90% of the HMO’s inpatient hospital services

paid commencing at the attachment point excess of $1,250,000 per member, up to Atlantic’s

maximum of $1,750,000.

16

The reinsurance agreements contained all the required standard clauses, including the

insolvency clause required by Section 1308(a)(2)(A) of the New York Insurance Law.

17

D. Holding Company System

Capital District Physicians’ Health Plan of New York, Inc., the ultimate parent in the

Holding Company system, is required to file registration statements pursuant to the requirements

of Part 98-1.16(e) of the Administrative Rules and Regulations of the New York State Health

Department (10 NYCRR 98-1.16). All pertinent filings made regarding the aforementioned

statutes during the examination period were reviewed, and no exceptions were noted.

The following is the organizational chart of CDPHP and its subsidiaries as of December 31, 2017:

Capital District Physicians’ Health Plan, Inc. (CDPHP)

(Parent Corporation), a not-for-profit entity

CDPHP Universal

Benefits, Inc.

(CDPHP its sole member)

Capital District Physicians’

Health Network, Inc.

(CDPHP owns 100%)

Carter Insurance Company,

Ltd.

(CDPHP owns 100%)

CDPHP The Foundation

Inc.

(CDPHP its sole member)

Practice Support Services,

LLC

(100% Direct Ownership)

Acuitas Health, LLC

(65% Ownership)

Strategic Solutions Management

Company, Inc.

(100% Direct Ownership)

18

The following is a summary of CDPHP’s significant entities within the holding company

system including the ultimate parent.

1. Capital District Physicians’ Health Plan, Inc., - the ultimate parent company of the holding

company system, is a not-for-profit corporation organized under Section 402 of the Business

Corporation Law of the State of New York to operate as an Individual Practice Association

(IPA) Health Maintenance Organization (“HMO”), pursuant to Article 44 of the New York

Public Health Law.

2. CDPHP Universal Benefits, Inc. (“UBI”) - incorporated in 1997, as a not-for-profit

membership corporation, with the CDPHP being the sole member. UBI has been granted a

license pursuant to the provisions of Article 43 of the New York State Insurance Law. The

HMO reported its subsidiary, UBI, as “other invested asset”, in the amount of $124,846,345 at

December 31, 2017.

3. Capital District Physicians’ Healthcare Network (“CDPHN”), - incorporated in 1991 and is a

wholly-owned subsidiary of the CDPHP, provides managed care and administrative support

services to the self-insured employer groups under the HMO’s administrative services

organization (“ASO”) contracts. As an investment in CDPHN, CDPHP reported a

book/adjusted carrying value in the amount of $30,713,778 as of December 31, 2017.

4. CDPHP Foundation, Inc. (the “Foundation”) - incorporated in 2014, as a not-for-profit

corporation organized under section 402 of the Not-for-Profit Corporation Law of the State of

New York, with CDPHP being the sole member. The Foundation was organized for the

purpose of improving the health and wellbeing of the community through health awareness,

prevention, wellness, education and other programs focused on health priorities. The

foundation began operations on January 1, 2017.

5. Carter Insurance Company, Ltd, (“Carter”), - was formed in November 2003, is the HMO’s

wholly owned Bermuda based reinsurance affiliate. Carter is a non-New York authorized

insurer. The HMO’s investment in Carter is carried at cost, which is adjusted for undistributed

earnings or losses and changes in the market value of investments. CDPHP’s investment in

19

Carter comprised a book/adjusted carrying value in the amount of $5,248,993 as of December

31, 2017.

6. Practice Support Services, LLC (“PSS”) - formed in 2016 as a Limited Liability Company

organized under Section 203 of the Limited Liability Company Law with CDPHN being the

sole member. PSS was organized for the purpose of providing consulting and other services to

health care providers.

7. Acuitas Health LLC, (“Acuitas”) - formed on September 21, 2016 as a Limited Liability

Company organized under Section 203 of the Limited Liability Company Law as a joint

venture between PSS and participating provider. Acuitas began operations in July 2017 and at

the time of inception PSS was the majority owner at 65% ownership. As of December 1, 2019,

PSS is the sole owner. Acuitas is a health services organization that provides health

management services to health care providers,

8. Strategic Solutions Management Consultants, Inc. (“SSMC”) - purchased by PSS in November

2016 through a stock purchase agreement whereby PSS is 100% owner. The total

consideration for the acquisition was $3,867,500, which was comprised of $2,367,500 in cash

and $1,500,000 in accrued contingent consideration. The acquisition resulted in $3,193,500 in

goodwill which is being amortized over 15 years. SSMC is a medical billing and healthcare

consulting company offering services to private practice physicians and physician and hospital

networks.

The HMO maintained the following inter-company agreements with its affiliates as of

December 31, 2017:

1. Administrative Services Agreement with UBI

The captioned agreement, effective June 15, 2006, subsequent to the Department’s

approval on February 2, 2006, requires CDPHP to provide UBI with

consultative/administrative services and also support services to UBI’s customers,

including but not limited to: financial, legal, internal operations, information technology,

marketing consultation, health care services, including the development, revision and

20

refinement of new health care service products, systems, policies, procedures and software

to support and enhance the business of UBI.

2. Administrative Services Agreement with CDPHN

The captioned agreement, effective January 1, 2004, was approved by the Department of

Financial Services and the Department of Health on May 27, 2004 and June 2, 2004,

respectively. This agreement requires CDPHP to provide CDPHN with consultative,

administrative and support services including, but not limited to: financial, legal, internal

operations, information technology, marketing consultation, healthcare services, including

the development, revision and refinement of new healthcare service products, systems,

policies, procedures and software to support and enhance the business of CDPHN.

3. Reinsurance Agreement with Carter Insurance Company, Ltd.

The HMO and Carter maintained the captioned agreement whereby CDPHP ceded

healthcare business in connection with in-patient hospital services covered under the

HMO’s enrollee contracts. The agreement, which covered the twelve-month period

January 1 through December 31, was renewed annually by the HMO and Carter during the

examination period.

Part 98-1.10(c) of the administrative rules and regulations of the Department of Health

(10 NYCRR 98-1.10(c)) states in part:

“(c) … Thirty days prior notice to the commissioner and, except in the

case of a PHSP, HIV SNP or PCPCP, the superintendent, is required

before entering into the following transactions between a controlled MCO

and any person in its holding company system; a reinsurance agreement

or an agreement for rendering services on a regular or systematic basis,

other than medical or management services that require prior approval

under this Subpart.”

The examiner noted that the HMO did not notify the superintendent of the affiliated

reinsurance agreement with Carter, as required pursuant to Part 98-1.10(c) of the administrative

rules and regulations of the Department of Health.

21

It is recommended that CDPHP comply with Part 98-1.10(c) of the administrative rules

and regulations of the Department of Health by notifying the Department thirty days prior before

entering inter-company reinsurance agreements with an affiliate.

On December 18, 2018, subsequent to the examination period, CDPHP notified the

Department of the reinsurance agreement with Carter. CDPHP ended the reinsurance agreement

with Carter at December 31, 2019, and Carter was subsequently liquidated.

E. Significant Operating Ratios

The underwriting ratios presented below are on an earned-incurred basis and encompass

the three-year period covered by this examination.

Amounts

Ratios

Total hospital and medical expense

$ 3,853,974,544

87.61%

Claims adjustment expenses

211,810,835

4.82%

General administrative expenses

225,524,381

5.13%

Increase in reserves

(16,300,000)

(0.4)%

Net underwriting gain

123,881,970

2.82%

Premiums earned

$ 4,398,891,730

100.00%

3. MEDICAL LOSS RATIO (“MLR”)

A. Market Classification

The HMO’s 2017 Medical Loss Ratio (“MLR”) Annual Reporting Form for the state of

New York was examined to assess compliance with the requirements of Title 45 of the Code of

Federal Regulations (“CFR”), Part 158, which implements section 2718 of the Public Health

Service Act (“PHS Act”). Section 2718 of the PHS Act, as added by the Affordable Care Act,

generally requires health insurance companies to submit to the Secretary of the U.S. Department

22

of Health and Human Services (“HHS”) an annual report on their MLRs. The MLR is the

proportion of premium revenue expended by a company on medical services and activities that

improve health care quality in a given market. Section 2718 of the PHS Act also requires a

company to provide rebates to consumers if it does not meet the MLR standard (82% in the

individual and small group markets and 85% in the large group market for the state of New York).

This examination of the HMO’s 2017 MLR Annual Reporting Form covered the reporting

period January 1, 2015 through December 31, 2017, including 2016 and 2017 experience and

claims run-out through March 31, 2018.

The examination was conducted in accordance with the NAIC’s 24 MLR Agreed Upon

Procedures (“MLR AUPs”). The MLR AUPs set forth the procedures for performing an

examination to evaluate the validity and accuracy of the data elements and calculated amounts

reported on the MLR Annual Reporting Form, and the accuracy and timeliness of any rebate

payments, if applicable. The examination included assessing the principles used and significant

estimates made by the HMO, evaluating the reasonableness of expense allocations, and

determining compliance with relevant statutory accounting standards, MLR regulations and

guidance, and the MLR Annual Reporting Form Filing Instructions.

Title 45 CFR §158.110(b) requires that a report for each MLR reporting year is to be

submitted to the Secretary of HHS by July 31

st

of the year following the end of an MLR reporting

year, on a form and in the manner prescribed by the Secretary of HHS. Based on the examiner’s

review, the 2017 MLR Annual Reporting Form filed by the HMO are fully compliant with the

requirements of Title 45 CFR §158.

23

Title 45 CFR §158.210 (a), (b) and (c) requires that an issuer must provide a rebate to

enrollees if the issuer has an MLR below the required amount (less than 82% in the individual and

small group markets and 85% in the large group market for the state of New York).

The HMO’s MLR and rebate calculations, as reported on its 2017 MLR Annual Reporting

Form and for the year ending December 31, 2017 were as follows:

MLR Components

Individual

Small Group

Large Group

Adjusted Incurred Claims

$ 35,549,186

$ 3,722,623

$ 379,305,355

Plus: Quality Improvement Expenses

$ 502,853

$ 189,856

$ 5,412,256

Less: Cost-sharing reductions

$ 63,572

Less: Federal Transitional Reinsurance Program

payments expected from HHS

$ 0

Less: Federal Risk Adjustment Program net payments

expected from (payable to) HHS

$ 8,782,324

$ (3,278,226)

Less: Federal Risk Corridors Program net payments (charges)

$ 0

$0

MLR Numerator

$27,206,143

$7,190,705

$384,717,611

Premium Earned

$31,481,636

$8,162,555

$450,664,717

Federal & State Taxes and Licensing/Regulatory Fees

$558,239

$147,971

$6,919,552

MLR Denominator

$30,923,397

$8,014,584

$443,745,165

Preliminary MLR

87.5%

94.4%

86.5%

Credibility Adjustment (cumulative)

2.3%

2.5%

0.0%

Credibility–Adjusted MLR (cumulative)

89.8%

96.9%

86.5%

MLR Standard

82%

82%

85%

Rebate Amount

$0

$0

$0

B. MLR Numerator

According to Title 45 CFR §158.221(b), the numerator of the MLR calculation is

comprised of incurred claims, as defined in Title 45 CFR §158.140, expenditures for activities that

improve health care quality as defined in Title 45 CFR §158.150, and Title 45 CFR §158.151, Cost

Sharing Reductions Program as defined in Title 45 CFR §158.140(b)(1)(iii) and Federal

24

Transitional Reinsurance, Federal Risk Adjustment and Federal Risk Corridor Programs as defined

by Title 45 CFR §158.140(b)(4)(ii), as applicable.

Incurred Claims

The examiner reviewed the accuracy and appropriateness of the amounts reported within

incurred claims as defined by Title 45 §CFR 158.140, including the verification of the data used

by the HMO to calculate adjusted incurred claims and the validation of a sample of incurred claims

reported by the HMO.

The 2017 MLR Annual Reporting Form that was filed by the HMO for the state of New

York complied with the MLR Annual Reporting Form Filing Instructions.

Based on the procedures performed, it was determined that the HMO’s incurred claims

were accurately reported on the HMO’s 2017 MLR Annual Reporting Form.

Quality Improvement Activities (“QIA”)

The HMO’s QIA process consists of the personnel and related operational administrative

costs as incurred primarily by CDPHP and then allocated to CDPHP and its subsidiaries. The cost

centers and the purpose of these cost centers are used to determine the total QIA reported on the

HMO’s MLR Annual Reporting Form.

The examiner reviewed the accuracy and reasonableness of health care quality

improvement expenses, including the validation of a sample of the QIA amounts reported, to

ensure they are in conformity with the definition of Healthcare Quality Improvement Expenses as

defined by Title 45 CFR §158.150 and Title 45 CFR §158.151, and to confirm that the allocation

methodology is reasonable and complies with the requirements set forth by Title 45 CFR §158.170.

25

Personnel and related operational and administrative costs QIA

Title 45 CFR Part 158.502 requires issuers to maintain all documents and other evidence

necessary to verify that the data submitted is in compliance with the definitions and criteria set

forth in Title 45 CFR Part 158 and that the MLR and any rebates owed are calculated and provided

in accordance with the Regulation. In addition, such records are required to be maintained under

Part 243.2 (b)(8) of Insurance Regulation No. 152 (11 NYCRR 243.8), cited above. In testing for

compliance with these requirements, it was noted that the HMO maintain adequate documentation

to support the cost reported in the QIA categories.

In testing for compliance with this requirement and Part 243.2 (b)(8) of Insurance

Regulation No. 152 (11 NYCRR 243.8) cited elsewhere in this report, it was noted that the HMO

had sufficient documentation to support the QIA allocation amounts.

To identify costs that are QIA applicable, the HMO requires each cost center to annually

attest to the activities performed. If the purpose and activities of the cost center meets the

qualifications of the QIA categories, the expenses of that cost center are included in the applicable

QIA category. The cost center expenses include CDPHP personnel and fringe as well as vendor

costs such as consulting and outsourced services. These expenses are allocated based upon a

metric that aligns with the cost center’s purpose and is primarily based upon membership.

Cost Sharing Reductions (“CSR”)

In accordance with Title 45 CFR 8158.140(b)(1)(iii), cost-sharing reduction payment

received from HHS must be deducted from incurred claims to the extent not reimbursed to the

provider furnishing the item or services. The HMO correctly reported advanced payments of CSR

26

received from HHS as a deduction from incurred claims on the HMO’s MLR Annual Reporting

Forms.

Federal Premium Stabilization Programs

The examiner reviewed the accuracy of the amounts reported for Federal Transitional

Reinsurance and Federal Risk Adjustment and Federal Risk Corridor Programs as defined by Title

45 CFR §158.140(b)(4)(ii), including the verification of amounts to HHS program summary

reports and the HMO’s transactional records.

Based on the procedures performed, the HMO’s Federal premium stabilization programs

amounts were accurately reported on the HMO’s MLR Annual Reporting Forms.

C. MLR Denominator

According to Title 45 CFR §158.22(c), the denominator of the MLR calculation is

comprised of premium revenue, as defined in Title 45 CFR §158.130, minus Federal and State

Taxes and Licensing / Regulatory fees, described in Title 45 CFR §158.161(a), and Title 45 CFR

§158.162(a)(1) and (b)(1).

Earned Premiums

The examiner reviewed the accuracy and appropriateness of the amounts reported within

earned premiums as defined by Title 45 §CFR 158.130, including the verification of the data used

by the HMO to calculate earned premium and the validation of a sample of policy premium

reported by the HMO.

Based on the procedures performed, the HMO’s earned premiums were accurately and

appropriately reported, for each market segment on the HMO MLR Annual Reporting Forms.

27

Federal and State Taxes and Licensing / Regulatory Fees

The examiner reviewed the accuracy and appropriateness of Federal and State Taxes and

Licensing / Regulatory Fees, including confirmation that the allocation methodology was

reasonable and complied with the requirements set forth by Title 45 CFR §158.170 and that taxes

were reported in accordance with the provisions of Title 45 CFR §158.161 and Title 45 CFR

§158.162.

Based on the procedures performed, it was determined that the HMO’s allocation

methodology is reasonable, and the Federal and State Taxes and Licensing / Regulatory fees were

accurately and appropriately reported for each market segment on the HMO’s MLR Annual

Reporting Forms.

D. Credibility Adjustment

According to Title 45 CFR §158.232, the Credibility–Adjustment is the product of the base

credibility factor multiplied by the deductible factor. The examiners reviewed the underlying data

utilized in the determination of the base credibility and deductible factors, tested the accuracy of

the calculation of the base credibility and deductible factors and the resulting Credibility–

Adjustment for the individual, small group, large group and student health plan markets. The

Company elected to use a deductible factor of 1.0, in lieu of calculating a deductible factor, which

has no impact on the Credibility–Adjusted MLR.

Based on the procedures performed, it was determined that the Company’s base credibility

factor, deductible factor and Credibility–Adjustment were accurately calculated and reported for

each market segment on the HMO’s MLR Annual Reporting Form.

28

E Credibility-Adjusted MLR

According to Title 45 CFR §158.221(a), the calculation of the MLR is the ratio of the

numerator to the denominator, plus the credibility adjustment. The examiner recalculated the

credibility-adjusted in accordance with 45 CFR § 158 and the applicable MLR Annual Reporting

Form Filing Instructions and determined the HMO’s credibility-adjusted MLR amounts were

accurately calculated for each market segment on the HMO’s MLR Annual Reporting Forms.

F. Rebate Disbursement and Notice

According to Title 45 CFR §158.240, a rebate is required to be paid no later than September

30

th

, following the MLR reporting year if an insurer’s credibility-adjusted MLR is less than the

MLR standard (82% in the individual and small group markets and 85% in the large group market

for the state of New York).

Based on the examiner’s review of the credibility-adjusted MLR for each market segment

on the HMO’s MLR Annual Reporting Forms, the HMO exceeded the MLR standard for the

individual, small group, and large group markets for the state of New York and thus was not

required to pay rebates to its enrollees.

According to Title 45 CFR §158.251, a notice of rebate is required when the credibility-

adjusted MLR does not exceed the MLR standard. Since the HMO’s credibility-adjusted MLR

exceeded the MLR standard for the individual, small group, and large group markets for the state

of New York, a notice of rebate was not required to be issued by the HMO.

G. Impact on Risk-Based Capital

29

According to Title 45 CFR §158.270(a), rebate payments having any adverse impact on

the HMO’s Risk-Based Capital (“RBC”) level requires notification by the Department to the

Secretary of the HHS. Based on the examiner’s review, it was determined that the HMO’s

Credibility adjusted MLR exceeded the minimum percentage for individual and small group

market and no rebates were issued, therefore there was no impact on the HMO’s RBC level that

would warrant notification of the Secretary of HHS.

30

4. FINANCIAL STATEMENTS

The following statements show the assets, liabilities, and surplus as of December 31, 2017,

as contained in the HMO’s 2017 filed annual statement, a condensed summary of operations and

a reconciliation of the surplus account for each of the years under review. The examiner’s review

of a sample of transactions did not reveal any differences which materially affected the HMO’s

financial condition as presented in its December 31, 2017 filed annual statement.

Independent Auditors

D&T was retained by the HMO to audit (in accordance with generally accepted accounting

principles “GAAP”) CDPHP’s consolidated combined statements of financial position as of

December 31

st

for each of the years within the examination period, and the related GAAP

statements of operations, surplus, and cash flows for the year then ended.

D&T concluded that the consolidated GAAP financial statements presented fairly, in all

material respects, the financial position of the HMO at the respective audit dates. Balances

reported in these audited financial statements were reconciled to the corresponding years’ annual

statements with no discrepancies noted.

31

A. Balance Sheet

Assets

Bonds

Common stocks

Cash, cash equivalents and short-term investments

Other invested assets

Receivables for assets

Investment income due and accrued

Uncollected premiums and agents’ balances in the course of

collection

Accrued retrospective premiums

Amounts recoverable from reinsurers

Electronic data processing and software

Receivable from parent, subsidiaries and affiliates

Healthcare and other amounts receivable

Total assets

$201,873,843

49,045,538

61,521,862

124,846,345

56

1,154,064

52,084,085

(3,027,677)

1,969,910

2,870,394

884,041

30,536,960

$523,759,421

Liabilities

Claims unpaid

Accrued medical incentive pool and bonus amounts

Unpaid claims adjustment expenses

Aggregate health policy reserves

Premiums received in advance

General expenses due and accrued

Amount due to parent, subsidiaries and affiliates

Total liabilities

$126,551,488

5,309,163

2,824,043

2,508,000

4,078,254

45,905,682

2,296,030

$189,472,660

Capital and Surplus

Aggregate write-ins for special surplus funds

Aggregate write-ins for other than special surplus funds

Unassigned funds

Total capital and surplus

14,933,316

180,299,961

139,053,484

$334,286,761

Total liabilities and capital and surplus

$523,759,421

32

B. Statement of Revenue and Expenses and Capital and Surplus

Capital and surplus increased $85,363,647 during the three-year examination period,

January 1, 2015 through December 31, 2017, detailed as follows:

Revenue

Premium income

$4,398,891,730

Hospital and Medical Expenses

Hospital/medical benefits

$2,644,423,095

Other professional services

252,000,403

Emergency room and out-of-area

97,529,549

Prescription drugs

781,223,179

Aggregate write-ins for other hospital and

medical costs

90,103,274

Incentive pool, withhold adjustments and

bonus amounts

20,065,366

Sub-total $3,885,344,866

Net reinsurance recoveries

31,370,322

Total hospital and medical expenses

$3,853,974,544

Claims adjustment expenses

211,810,835

General administrative expenses

225,524,381

Increase in reserves for accident and health

(16,300,000)

contracts

Total underwriting deductions 4,275,009,760

Net underwriting gain $ 123,881,970

Net investment income earned 14,639,658

Net realized capital gains

491,402

Net investment gains less capital gain taxes

15,131,060

Aggregate write-ins for other income

(72,224)

Net income after capital gain

138,940,806

Federal and foreign income taxes incurred

0

Net income

$ 138,940,806

33

Change in Capital and Surplus

Capital and Surplus, per report on

examination, as of December 31, 2014

$248,923,114

Gains in

Surplus

Losses in

Surplus

Net income

Change in net unrealized capital losses

Change in nonadmitted assets

$138,940,806

1,482,294

$55,059,453

__________

Net increase in capital and surplus

$ 85,363,647

Capital and Surplus, per report on

examination, as of December 31, 2017

$334,286,761

5. CLAIMS UNPAID

The examination liability of $126,551,488 for the above captioned account is the same as

the amount reported by the HMO as of December 31, 2017.

The examination analysis of the claims unpaid reserve was conducted in accordance with

generally accepted actuarial principles and practices and was based on statistical information

contained in the HMO’s internal records and filed annual statements as verified during the

examination. The examination reserve was based upon actual payments made through a point in

time, plus an estimate for claims remaining unpaid at that date. Such estimate was calculated based

on actuarial principles, which utilized the HMO’s past experience in projecting the ultimate cost

of claims incurred on or prior to December 31, 2017.

34

6. SUBSEQUENT EVENT

Pursuant to the Bylaws of CDPHP, the voting members of CDPHP approved the transfer

of all outstanding and issued CDPHN stock from CDPHP to UBI effective January 1, 2020. This

was approved by CDPHP Board of Directors, NYSDFS, and New York State Department of

Health.

35

7. COMPLIANCE WITH PRIOR REPORT ON EXAMINATION

The prior report on examination as of December 31, 2014 contained eight (9) comments

and recommendations pertaining to the financial portion of the examination (page number refers to

the prior report on examination):

ITEM NO

PAGE NO.

Corporate Governance

1.

It is recommended that the HMO amend its current Key

Bank custodial agreement to include the required

protective safeguard provisions detailed in the Handbook.

11

The HMO has complied with recommendation.

2.

It is recommended that the HMO assess its current

organizational and staffing structure with consideration

given to segregating responsibilities for

internal audit,

information security governance, risk management and

internal testing. This assessment should consider all

aspects of ERM, internal audit,

information security

governance and operations, and administrative

responsibilities related to management’s ERM testing of

controls. Such recommendation is also consistent with the

same requirement indicated in CDPHP’s Corporate

Internal Audit Charter.

13

The HMO has complied with recommendation.

3.

It is recommended that as a best practice CDPHP

restructure the organizational reporting structure of its

internal audit department by having its top supervisory

employee in charge of that department report directly to

the Audit Committee and on a dotted line basis to

13

management.

The HMO has complied with recommendation.

4.

It is recommended that the HMO’s Audit Committee be

14

responsible for reviewing and approving the performance

36

ITEM NO

PAGE NO.

evaluation and the salary and variable compensation of the

Director of Audit Information and Assurance.

The HMO has complied with recommendation.

5

It is recommended that CDPHP comply with its Internal

Audit Charter by communicating to senior management

and the Audit Committee, all significant matters of

operational security.

14

The HMO has complied with recommendation

6.

It is recommended that CDPHP comply with the

requirement of its Internal Audit Charter by ensuring that

an external quality assurance review and assessment of

CDPHP’s internal audit activities are conducted at least

every five years by an independent reviewer.

14

The HMO has complied with recommendation.

Holding Company System

7.

It is recommended that CDPHP comply with Part 98-

1.10(c) of the administrative rules and regulations of the

Department of Health by filing with the Department for

approval, its inter-company reinsurance agreement with

its affiliate, Carter Insurance Company of Hamilton,

Bermuda.

22

The HMO has not complied with this recommendation. A

similar recommendation will be made in this report.

Insurance Regulation No. 118

8.

It is recommended that the HMO comply with Parts (a) and

(b) of Section 4 of Insurance Regulation No. 118 when

appointing a new CPA for purposes of the annual audit of

its financial statements by filing with the Superintendent,

within sixty days of the CPA’s appointment by the HMO,

the requisite CPA letter stating that the firm is aware of the

provisions of New York State insurance laws and

regulations relative to accounting and financial matters of

this State.

25

The HMO has complied with recommendation.

37

ITEM NO

PAGE NO.

9.

It is recommended that CDPHP comply with the

requirements of paragraph 3 of Section (b) of Insurance

Regulation No. 118 by filing within the specified fifteen

day timeframe the requisite CPA attestation, stating

whether the firm agrees with the HMO’s representation

that it had no disagreement with the former CPA within the

previous two years on any matter of accounting principles

or practices, or financial statement disclosure, or auditing

scope or procedure that might or could have been

referenced in the CPA opinions rendered in the CPA

Reports of the prior two reporting years.

The HMO has complied with recommendation.

26

38

8. SUMMARY OF COMMENTS AND RECOMMENDATIONS

ITEM

PAGE NO.

A.

Corporate Governance

It is recommended that the HMO comply with its own audit

committee charter by updating the role of the treasurer of the

corporation to the treasurer of the board of director.

Subsequent to the examination date, June 25, 2018, the Audit

Committee updated its Audit Charter from the chair of the

committee being the “Treasurer of the Corporation” to the

“Treasurer of the Board of Directors”.

9

B.

Reinsurance

It is recommended that CDPHP comply with Part 98-1.10(c) of

the administrative rules and regulations of the Department of

Health by notifying the Department thirty days prior before

entering inter-company reinsurance agreements with an

affiliate.

21

Subsequent to the examination date, December 18, 2018,

CDPHP notified the Department of the reinsurance agreement

with Carter.

_______________________

_______________________

Respectfully submitted,

Gail A Ross

Financial Services Examiner 2

STATE OF NEW YORK )

) SS.

)

COUNTY OF NEW YORK )

GAIL A ROSS, being duly sworn, deposes and says that the foregoing report

submitted by him is true to the best of his knowledge and belief.

Gail A Ross

Subscribed and sworn to before me

This ____ day of _________ 2023